NVIDIA: Is the AI faith collapsing, turning honey into poison?

NVIDIA (NVDA.O) released its financial report for the second quarter of the 2025 fiscal year (ending in July 2024) after the US stock market on the early morning of August 29th:

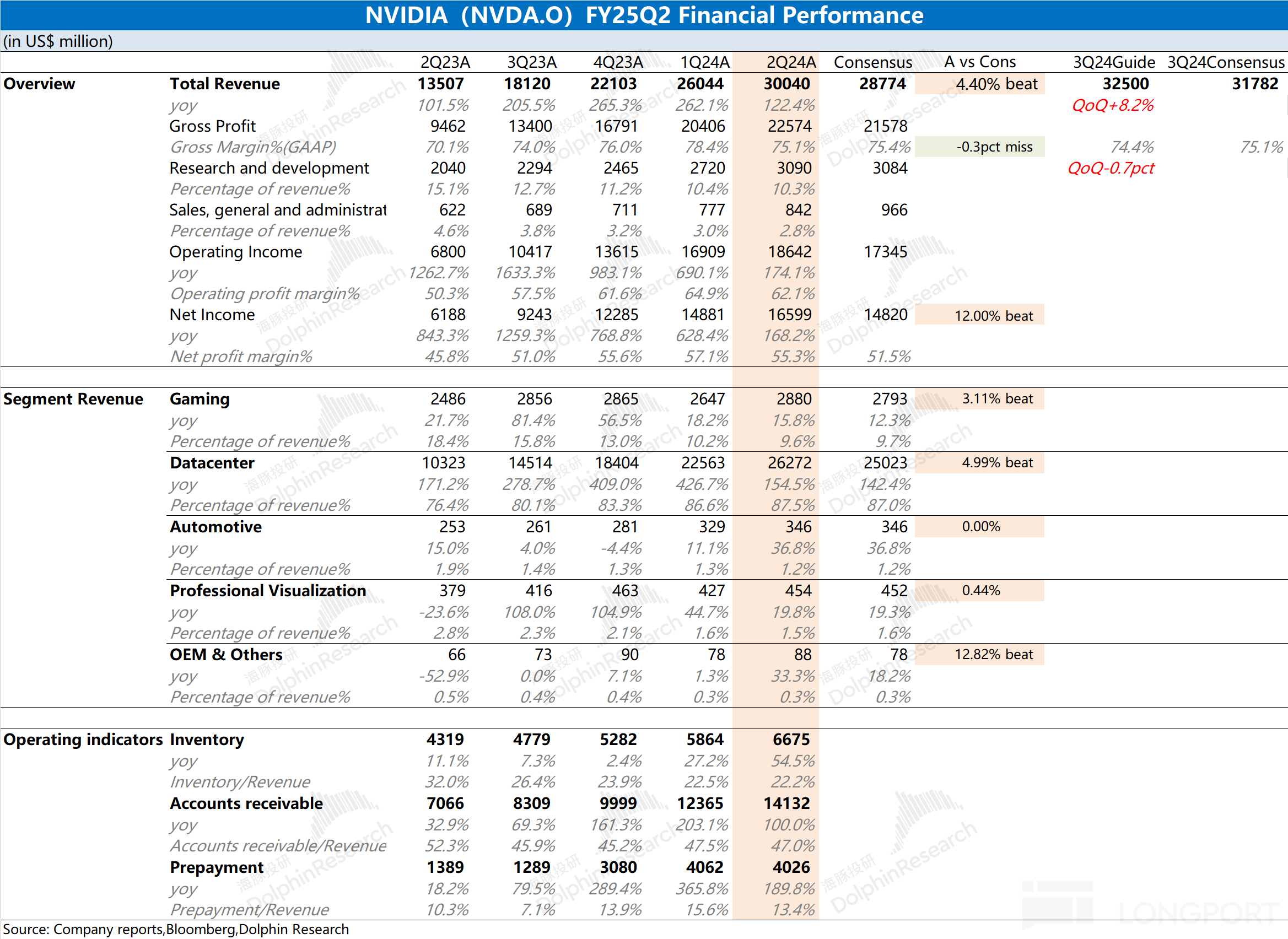

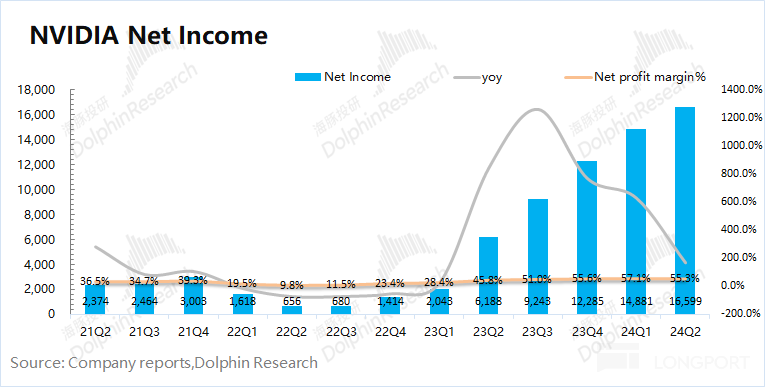

1. Overall Performance: Revenue growth slows down, gross margin declines slightly. In this quarter, NVIDIA achieved a revenue of $30.04 billion, a year-on-year increase of 122.4%, slightly better than market expectations ($28.8 billion). NVIDIA's gross margin (GAAP) for this quarter was 75.1%, lower than market expectations (75.4%). Affected by negative factors such as material inventory reserves, the gross margin declined slightly. The net profit for this financial report was $16.6 billion, a year-on-year increase of 168%. The profit reached a new high, but the growth rate has slowed down.

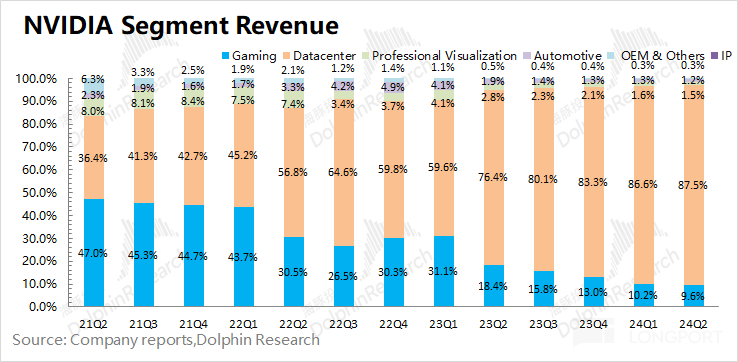

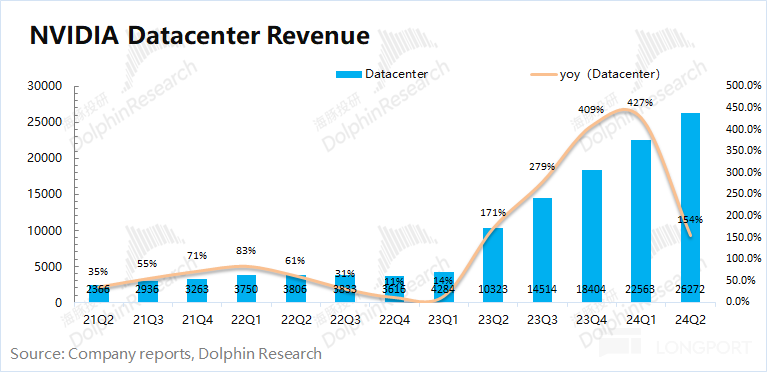

2. Core Business Situation: Data center is the main driving force. The data center business accounts for 87.5% of the company's revenue, making it the most core business of the company.

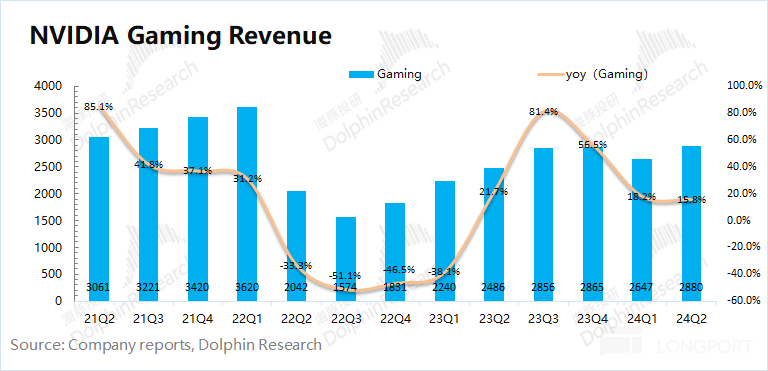

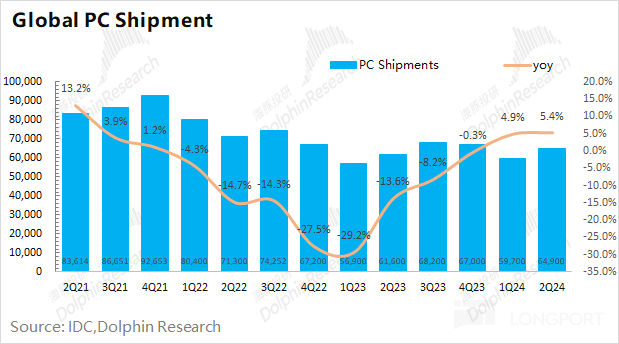

1) Gaming business grew by 15.8% year-on-year this quarter, continuing to recover. The growth of the company's gaming business this quarter is mainly driven by the recovery of the PC industry and the increase in gaming graphics card market share. Combined with the global PC market, the shipment volume this quarter has returned to 64.9 million units, showing some recovery from the bottom.

2) Data center business grew by 155% year-on-year this quarter, mainly driven by the demand for large models, recommendation engines, and generative AI. The growth of the business benefited from the increase in capital expenditures from cloud service providers, but the growth rate of the company's business revenue began to slow down this quarter.

3. Key Financial Indicators: Expense ratio remains low. NVIDIA's operating expense ratio this quarter continued to decline to 13.1%, with the revenue growth offsetting the increase in expenses. The current inventory ratio is still at a historical low, indicating that the demand for NVIDIA's current products is still good.

4. Guidance for the next quarter: NVIDIA expects revenue of $32.5 billion (±2%) for the third quarter of the 2025 fiscal year, a year-on-year increase of 79.4%, slightly better than the market expectation of $31.8 billion; Gross margin for the second quarter is expected to be 74.4% (±0.5%), lower than the market expectation of 75.1%.

Dolphin's overall view:

From NVIDIA's performance this quarter, both the revenue and profit sides have shown better-than-expected results. However, the guidance for the next quarter provided by the company does not significantly exceed market expectations. While revenue is slightly better than market expectations, the gross margin has continued to decline, significantly lower than market expectations With the negative impact of inventory reserves on certain product materials, the company's gross profit margin will continue to be under pressure in the second half of the year.

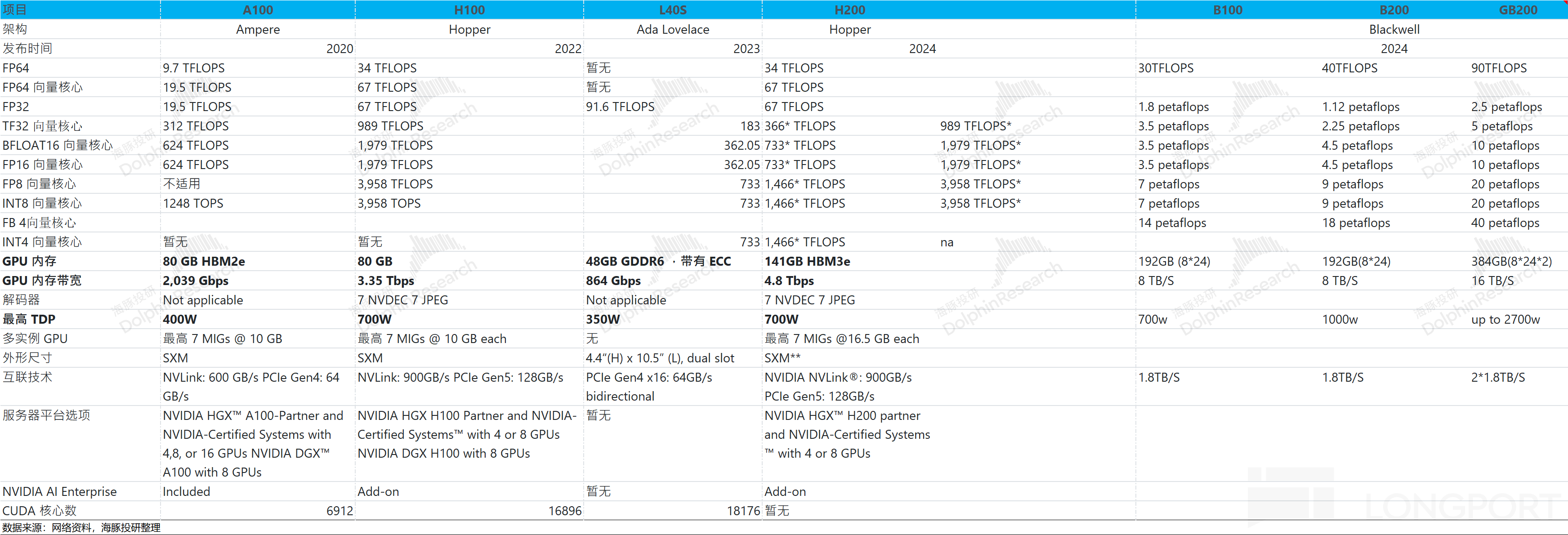

As for Blackwell, the company has been designing and producing it since the second quarter, but they intend to replace some masks. By redesigning to further enhance the stability of Blackwell, bulk production is expected to be achieved in the fourth quarter.

Considering the capital expenditures of major cloud service providers, the overall expectations are still being raised. Benefiting from increased investments, the company's data centers and AI business are expected to continue to rise. The strong performance of games like Black Myth: Wukong is also expected to bring incremental growth to the gaming business. The company is expected to continue growing on the revenue side, while there is still a risk of a further decline in gross profit margin.

In terms of investment itself, although the company's performance is still growing, the growth rate has started to decline. Due to the excessive market expectations already priced into the company's stock, the slowdown in performance and the "redesign" of Blackwell will to some extent affect market confidence. Considering NVIDIA and the market situation, Dolphin expects the company's PE ratio for this year to be around 45 times. If there are further adjustment risks in operations, the company's stock price will continue to be under pressure.

For a detailed analysis of NVIDIA's financial report, please see below:

I. Core Performance Indicators: Slowing Revenue Growth, Slight Decline in Gross Profit Margin

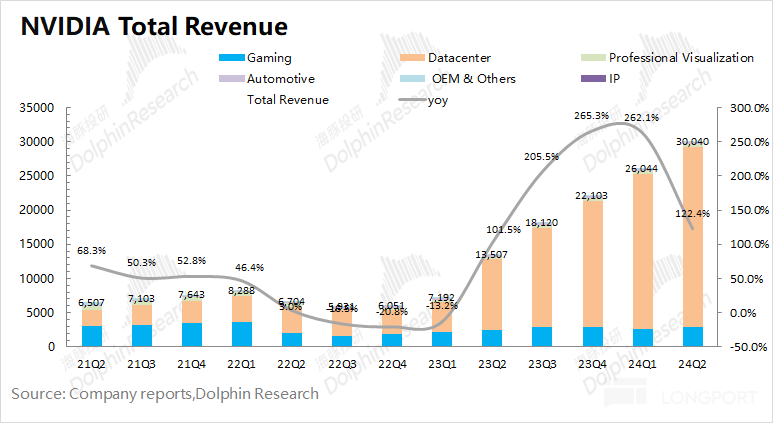

1.1 Revenue: In the second quarter of fiscal year 2025, NVIDIA achieved revenue of $30.04 billion, a year-on-year increase of 122.4%, exceeding market expectations ($28.8 billion). The company's revenue continued to rise this quarter, mainly driven by growth in downstream data center and gaming businesses.

Looking ahead to the third quarter of fiscal year 2025, the company's revenue is expected to continue growing. NVIDIA expects third-quarter revenue to be $32.5 billion (plus or minus 2%), a year-on-year increase of 79.4%, slightly better than the market expectation of $31.8 billion, with revenue growth still mainly coming from the data center business. In addition, with the mass production of Blackwell in the fourth quarter, the company is expected to bring in new increments.

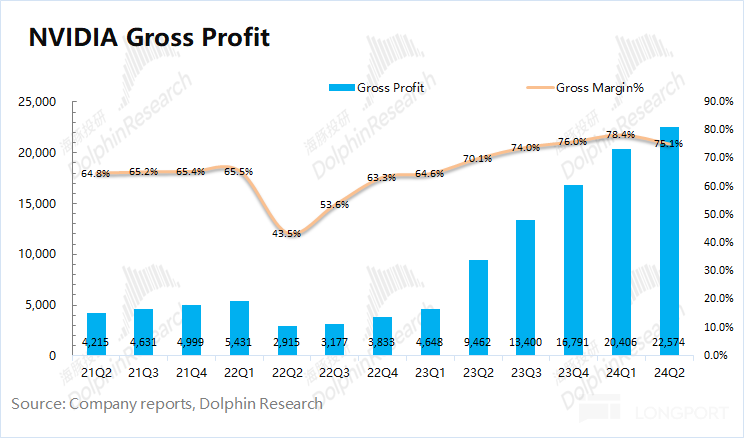

1.2 Gross Margin (GAAP): In the second quarter of fiscal year 2025, NVIDIA achieved a gross margin (GAAP) of 75.1%, lower than market expectations (75.4%). The gross margin in the second quarter was also affected to some extent by the negative impact of low Blackwell material inventory reserves.

With the strong growth of the data center business, the company's gross margin level is gradually being raised. Part of the reason is that the AI products themselves have relatively high gross margins, and another part reflects the current situation in the market where demand outstrips supply, leading to an overall increase in product prices. However, whether it can sustainably remain at a relatively high level still needs to be tested by the market.

NVIDIA's expected gross margin for the third quarter of fiscal year 2025 is 74.4% (plus or minus 0.5%), lower than market expectations (75.1%). **Driven by the demand for AI and other technologies, the company's gross profit margin has increased from 65% to over 70%. However, due to factors such as certain product materials, the company's gross profit margin will still face some pressure.

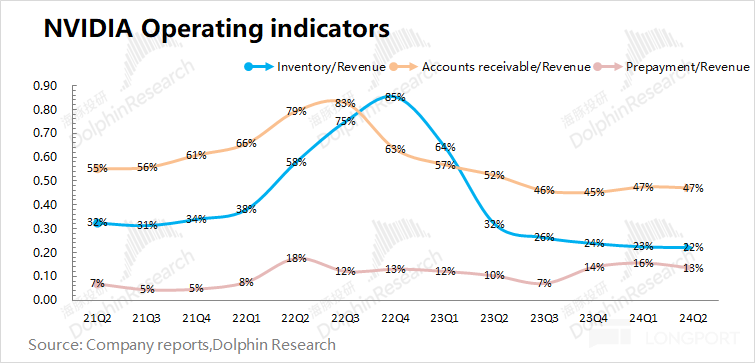

1.3 Operating Indicators

1) Inventory/Revenue: The ratio for this quarter is 22%, a decrease of 1 percentage point from the previous quarter. Although the company's inventory has risen to $6.7 billion this quarter, compared to the company's high revenue growth, the proportion of inventory is still at a historical low. The company is still facing a situation of supply shortage, with the gross profit margin also at a relatively high level;

2) Accounts Receivable/Revenue: The ratio for this quarter is 47%, remaining stable. The proportion of accounts receivable is also relatively low, indicating a good collection situation for the company.

II. Core Business Situation: Data Center is the Main Driver

Driven by the demand for AI and other technologies, in the second quarter of the 2025 fiscal year, NVIDIA's data center business accounted for 87.5% of the company's revenue. The gaming business share has been squeezed to less than 10%, making the data center business the most important factor affecting the company's performance.

2.1 Data Center Business: In the second quarter of the 2025 fiscal year, NVIDIA's data center business achieved revenue of $26.3 billion, a year-on-year increase of 154%. This quarter, NVIDIA's data center business reached a new high, mainly driven by the demand for the Hopper GPU computing platform, which is used for training and inference in large language models, recommendation engines, and generative AI applications.

Breaking it down: The company's data center business had computing revenue of $22.6 billion, a year-on-year increase of 162%; networking revenue was $3.7 billion, a year-on-year increase of 114%, benefiting from AI revenue from InfiniBand and Ethernet.

As cloud service providers currently account for about 45% of the company's data center revenue, the capital expenditures of cloud service providers directly impact the company's data center business. Looking at the capital expenditures of the four giants Meta, Google, Microsoft, and Amazon, the total capital expenditures of the four companies reached $58.3 billion this quarter, a year-on-year increase of 70%, with Microsoft's capital expenditures increasing by over 30% compared to the previous quarter. The increase in capital expenditures by these tech giants provides assurance for the growth of the company's data center business.

Combining the company's revenue guidance of $32.5 billion for the next quarter, Dolphin believes that the growth will still mainly come from the data center business, with cloud service providers' annual capital expenditure plans also being raised this quarter. Blackwell's shipments in the fourth quarter are also expected to bring new increments to the business.

Blackwell Progress: In the second quarter, the company delivered samples of the Blackwell architecture to customers. Blackwell is scheduled to start mass production in the fourth quarter and continue to increase production in the 2026 fiscal year, with the company expecting Blackwell revenue to reach billions of dollars in the fourth quarter.

2.2 Gaming Business: In the second quarter of the 2025 fiscal year, NVIDIA's gaming business achieved revenue of $2.88 billion, a year-on-year increase of 15.8%. This growth is mainly attributed to the increase in sales of GeForce RTX 40 series GPUs and gaming console SOCs.

Considering the performance of Intel and AMD, Dolphin believes that the recovery of gaming graphics cards is better than the overall PC market, and NVIDIA's discrete graphics card market share has also rebounded.

The overall PC market shipments have improved, which is also one of the factors contributing to the growth of the company's gaming business. According to the latest data from IDC, global PC market shipments in the second quarter of 2024 were 64.9 million units, a year-on-year increase of 5.4%. With the overall market recovery, the PC market has shown some repair, and Intel and AMD's PC businesses have also rebounded. Since gaming graphics cards are mainly installed on PCs, NVIDIA's gaming business has also benefited to some extent.

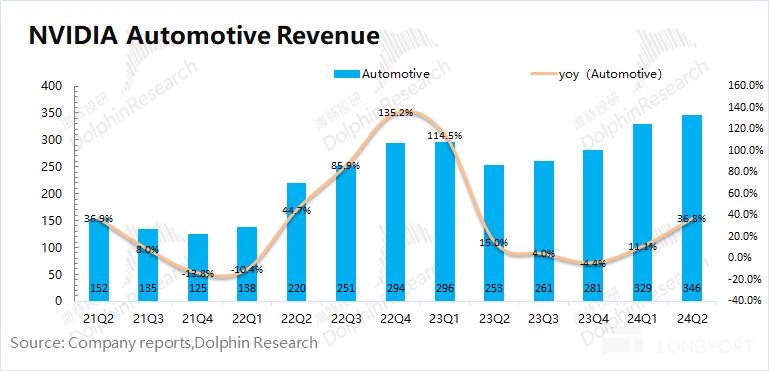

2.3 Automotive Business: In the second quarter of the 2025 fiscal year, NVIDIA's automotive business achieved revenue of $346 million, a year-on-year increase of 36.8%, driven by NVIDIA's AI Cockpit solutions and autonomous driving platform.

Although the company's automotive business has also shown a significant recovery, it currently accounts for a very small proportion of revenue (less than 2%). Currently, NVIDIA's performance is still mainly focused on the performance of the data center and gaming businesses.

III. Key Financial Indicators: Continued Decrease in Expense Ratio

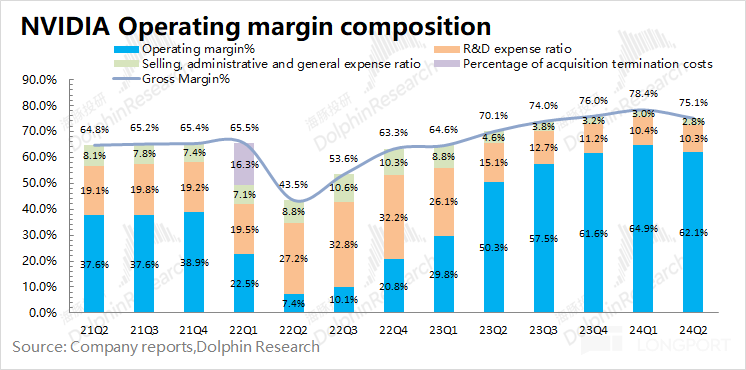

3.1 Operating Profit Margin

In the second quarter of the 2025 fiscal year, NVIDIA's operating profit margin was 62.1%, showing a slight decline. The decline in operating profit margin this quarter was mainly due to the decrease in gross profit margin.

Analyzing the composition of the operating profit margin, the specific changes are as follows:

"Operating Profit Margin = Gross Profit Margin - Research and Development Expense Ratio - Sales, Administrative Expense Ratio"

1) Gross Profit Margin: This quarter was 75.1%, a decrease of 3.3 percentage points compared to the previous quarter. Due to factors such as inventory reserves for certain product materials, the company's gross profit margin was under pressure.

2) Research and Development Expense Ratio: This quarter was 10.3%, a decrease of 0.1 percentage point compared to the previous quarter. While the absolute value of the company's research and development expenses increased, the expense ratio decreased again due to the rapid increase in revenue.

3) Sales, Administrative Expense Ratio: This quarter was 2.8%, a decrease of 0.2 percentage points compared to the previous quarter. Although the absolute value increased, the company's sales expense ratio remained at a relatively low level.

The company's guidance for operating expenses in the third quarter of the 2025 fiscal year continues to increase to $4.3 billion, but compared to the growth in revenue, the operating expense ratio is expected to continue to decrease to around 13.2% in the next quarter. The rapid growth in revenue will lower the expense ratio.

3.2 Net Profit (GAAP) Margin

In the second quarter of the 2025 fiscal year, NVIDIA's net profit was $16.6 billion, a significant year-on-year increase. The net profit margin for this quarter was 55.3%, showing a slight decline compared to the previous quarter. Although the company's revenue continued to grow this quarter and the operating expense ratio continued to decline, the larger decrease in gross profit margin led to the sequential decline in net profit margin.

Dolphin Research on NVIDIA's historical articles:

In-depth:

June 6, 2022: "Stock Market Tremors, Were Apple, Tesla, and NVIDIA Wrongly Killed?"

February 28, 2022: "NVIDIA: High Growth is Real, But Value for Money is Still Lacking"

December 6, 2021: "NVIDIA: Valuation Cannot Rely Solely on Imagination"

September 16, 2021: "NVIDIA (Part 1): How Did the Chip Bull with Twentyfold Growth in Five Years Come About?" 2021 September 28th, "NVIDIA (Part 2): No longer driven by dual wheels, will Davis double kill?"

Earnings Season

2024 May 23rd Earnings Call, "NVIDIA: Sovereign AI will bring billions in revenue (FY25Q1 Earnings Call)"

2024 May 23rd Earnings Review, "NVIDIA: 'Universe' strongest stock, gift package keeps exploding"

2024 February 22nd Earnings Call, "Accelerating computing, global data centers to double (NVIDIA 4QFY24 Summary)"

2024 February 22nd Earnings Review, "NVIDIA: AI shines alone, the true king of chips"

2023 November 22nd Earnings Call, "The first wave of artificial intelligence (NVIDIA 3QFY24 Earnings Call)"

2023 November 22nd Earnings Review, "NVIDIA: Computing power czar in full force? 'Virtual fire' looming"

2023 August 24th Earnings Call, "The computing revolution named 'AI' (NVIDIA FY2Q24 Earnings Call)"

2023 August 24th Earnings Review, "NVIDIA: Exploding again, the 'solo performance' of the AI king"

2023 May 25th Earnings Call, "Emerging from the trough, embracing the AI era (NVIDIA FY24Q1 Earnings Call)"

2023 May 25th Earnings Review, "Exploding NVIDIA: AI new era, the future is already here" 2023 年 2 月 23 日电话会"Performance hits bottom and will rebound, AI is the new focus (NVIDIA FY23Q4 conference call)" link

2023 年 2 月 23 日财报点评"Surviving the cyclical robbery, encountering ChatGPT again, NVIDIA's faith returns" link

2022 年 11 月 18 日电话会"Will the continuously rising inventory be digested in the next quarter? (NVIDIA FY2023Q3 conference call)" link

2022 年 11 月 18 日财报点评"NVIDIA: Profits halved, when will the turning point come?" link

2022 年 8 月 25 日电话会"How does the management explain the 'flash crash' in gross margin? (NVIDIA FY2023Q2 conference call)" link

2022 年 8 月 25 日财报点评"Is NVIDIA stuck in the mud, going back to 2018?" link

2022 年 8 月 8 日业绩预告点评"Thunder rolling, NVIDIA's performance in free fall" link

2022 年 5 月 26 日电话会"Combination of epidemic and lockdown, gaming decline drags down second-quarter performance (NVIDIA conference call)" link

2022 年 5 月 26 日财报点评"The 'epidemic fat' is gone, NVIDIA's performance looks bleak" link

2022 年 2 月 17 日电话会"NVIDIA: Advancing with multiple chips, data center becomes the focus of the company (conference call summary)" link

2022 年 2 月 17 日财报点评"NVIDIA: Concerns behind the better-than-expected performance | Reading financial reports" link

2021 年 11 月 18 日电话会"How does NVIDIA build the metaverse? Management: Focus on Omniverse (NVIDIA conference call)" link 2021 年 11 月 18 日财报点评《 算力爆赚、元宇宙加持,英伟达要一直牛下去?》

直播

2022 年 5 月 26 日《 NVIDIA Corporation (NVDA.US) 2023 财年第一季度业绩电话会》

2022 年 2 月 17 日《 NVIDIA Corporation (NVDA.US) 2021 年第四季度业绩电话会》

2021 年 11 月 18 日《 NVIDIA Corporation (NVDA.US) 2022 年第三季度业绩电话会》

本文的风险披露与声明: Dolphin Investment Research 免责声明及一般披露