Heartbeat Company: How long can the fiery vibes last?

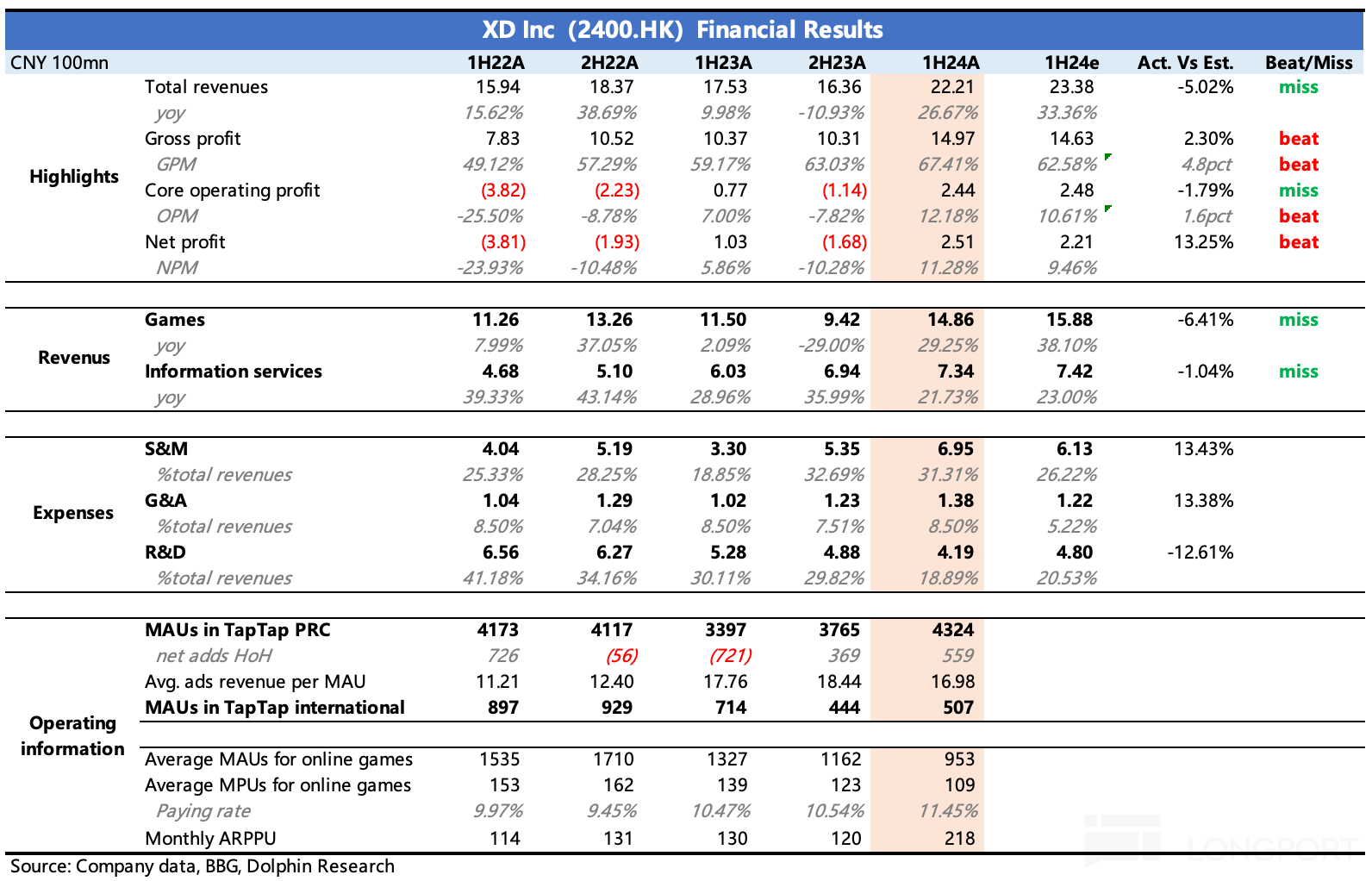

At noon on August 30th Beijing time, $XD INC(02400.HK) released its performance for the first half of 2024. Due to the positive performance forecast issued at the beginning of the month, market expectations were not low.

In reality, it seems that both game and TapTap advertising revenue slightly missed expectations. On the contrary, due to the higher profit margin of self-developed games and more stringent optimization of research and development personnel than expected, the significant increase in sales expenses caused by the pre-marketing of the global release of "Sword of the Bellflower" in August was offset. This ultimately made XD INC's profit performance more impressive.

Specifically:

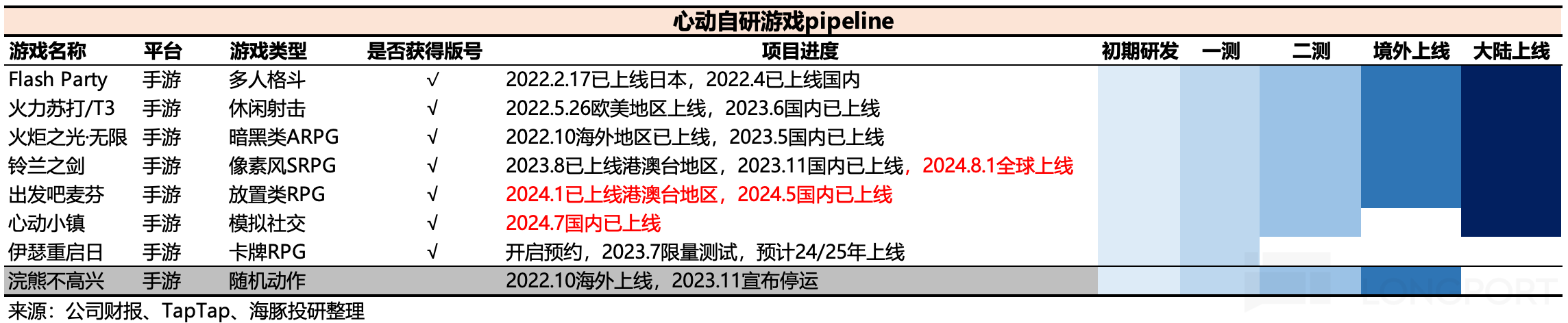

1. "Muffin" Takes Over from "Sausage Party"

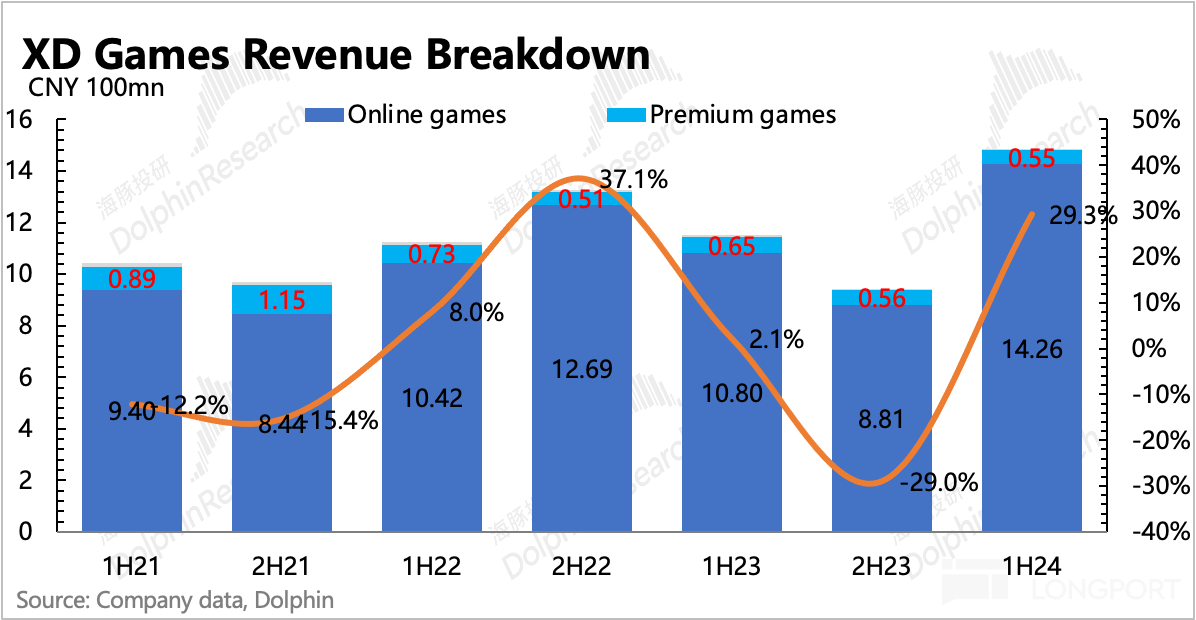

Gaming revenue in the first half of the year increased by 29% year-on-year, reaching 1.49 billion, exceeding the forecast but lower than market expectations. The year-on-year growth was mainly contributed by "Setting Off Muffin" launched at the beginning of the year and "Sword of the Bellflower" launched at the end of last year, while the flagship game "Sausage Party" continued to decline. The top five games are currently "Setting Off Muffin" > "Sausage Party" > "Sword of the Bellflower" > "Torchlight: Infinite" > "Ragnarok M".

"Setting Off Muffin," which was launched in January ahead of Hong Kong, Macau, and Taiwan, unexpectedly became a hit. The scale of its success exceeded expectations. "Muffin," developed by the RO team, had successful experiences in game style and type in the past ("Ragnarok Online," "Immortal Urala"), and as an idle game that integrated some MMO elements, the initial market expectations were not too low.

However, the success of "Muffin" exceeded expectations. It remained in the top 20 of the iOS bestseller list in Hong Kong until July, after dropping out of the top 10. In the mainland market, due to intense game competition this year, the domestic version of "Muffin" dropped out of the top ten during the summer after being online for two months in May. However, the mainland market is large enough, and based on data from Qimai and the assumption of Android/iOS = 2:1, the domestic version's revenue is expected to reach nearly 1 billion after three months online, higher than Dolphin Jun's previous expectations in the last annual report review.

2. TapTap User Growth Surges, Company Actively Controls Commercialization

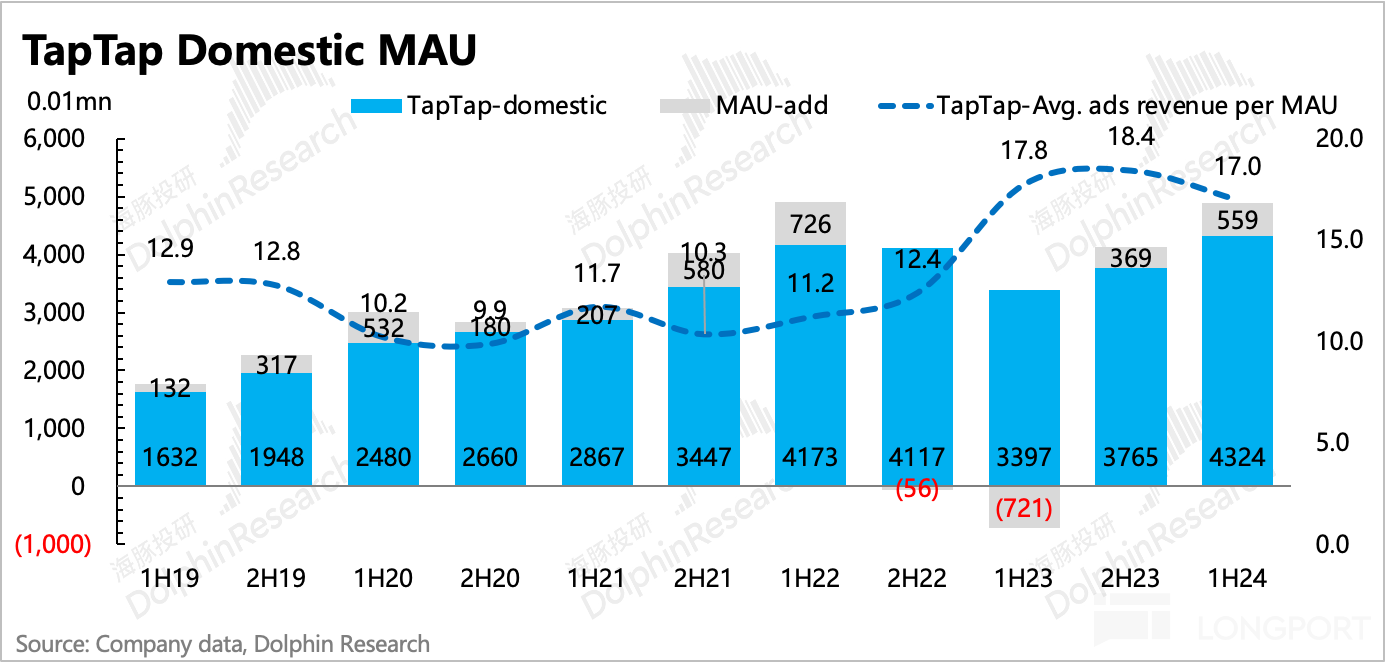

TapTap's domestic MAU increased to 43.24 million in the first half of 2024, a 27% year-on-year growth, with a net increase of 5.59 million compared to the previous period. Driving factors include the overall increase in industry supply and the company's position in the product cycle, with impressive game performance (self-developed/exclusive titles still driving traffic actively).

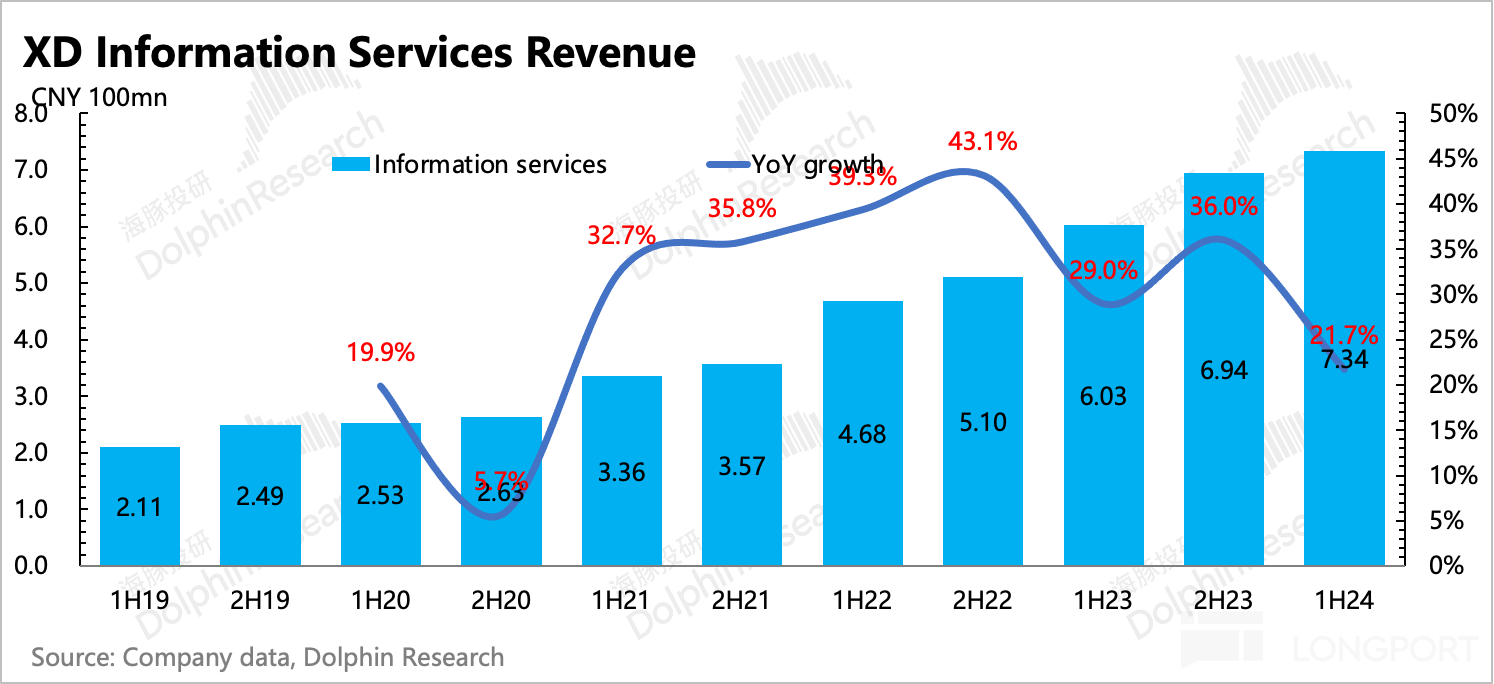

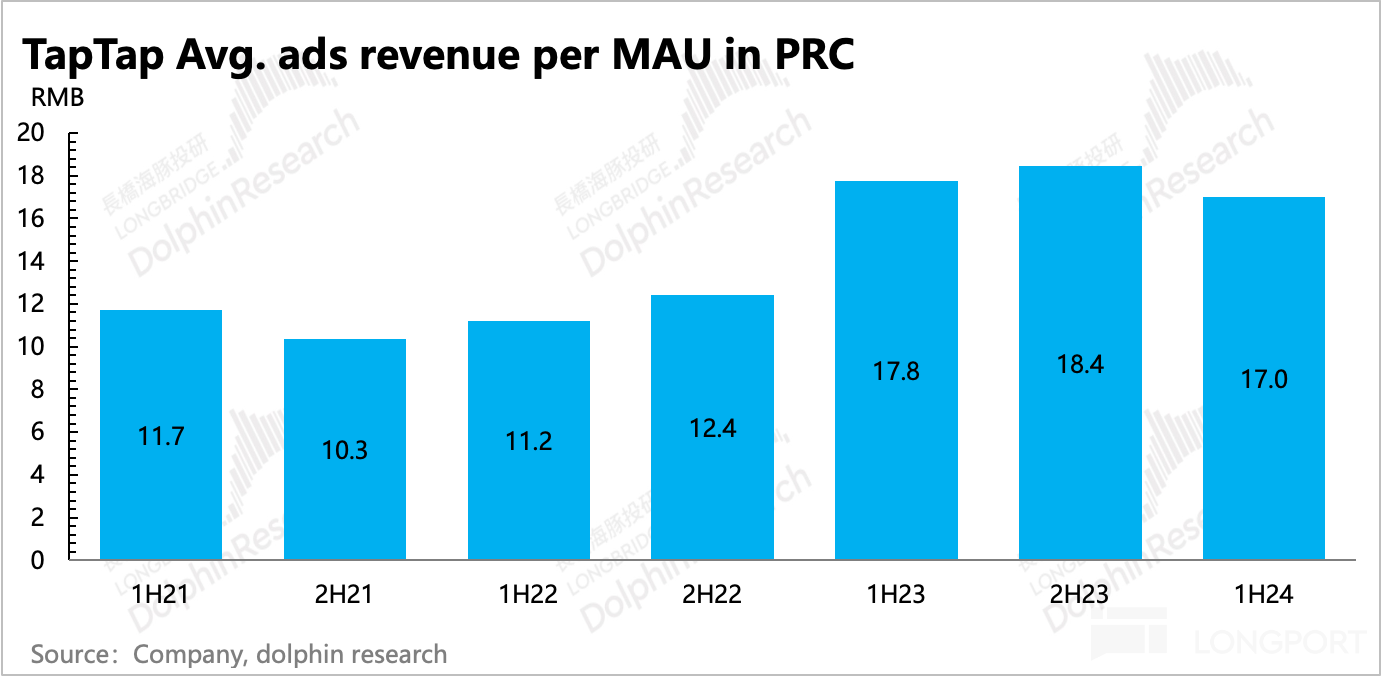

However, the company stated that in the first half of the year, in order to ensure user experience, advertising placement was relatively restrained. Therefore, looking at TapTap's information service revenue, it reached 734 million in the first half of the year, a 22% year-on-year growth, but the monetization value per user actually declined year-on-year.

However, the greater the influence of TapTap users, the more they can attract more advertising placements and even exclusive/mainstream game releases in the long run (such as "Happy Fishing Master", "Ming Chao", "JX3" in the first half of the year), after all, TapTap still follows a zero revenue-sharing policy. Previously, Tencent publicly challenged the Android channel, indicating that developers have long been dissatisfied with the channels.

In the first half of the year, the company controlled the advertising loading rate, which also reflects TapTap's position in the industry chain. Therefore, Dolphin Jun expects TapTap to still perform well in the chaotic summer game battle in the second half of the year.

3. Self-developed high-margin + stricter staff simplification = profits exceeding expectations

On the revenue side, there is third-party high-frequency data disclosed in advance, but expense outlays and profit performance are mainly reflected in the interim report, providing incremental information on "enterprise operational efficiency".

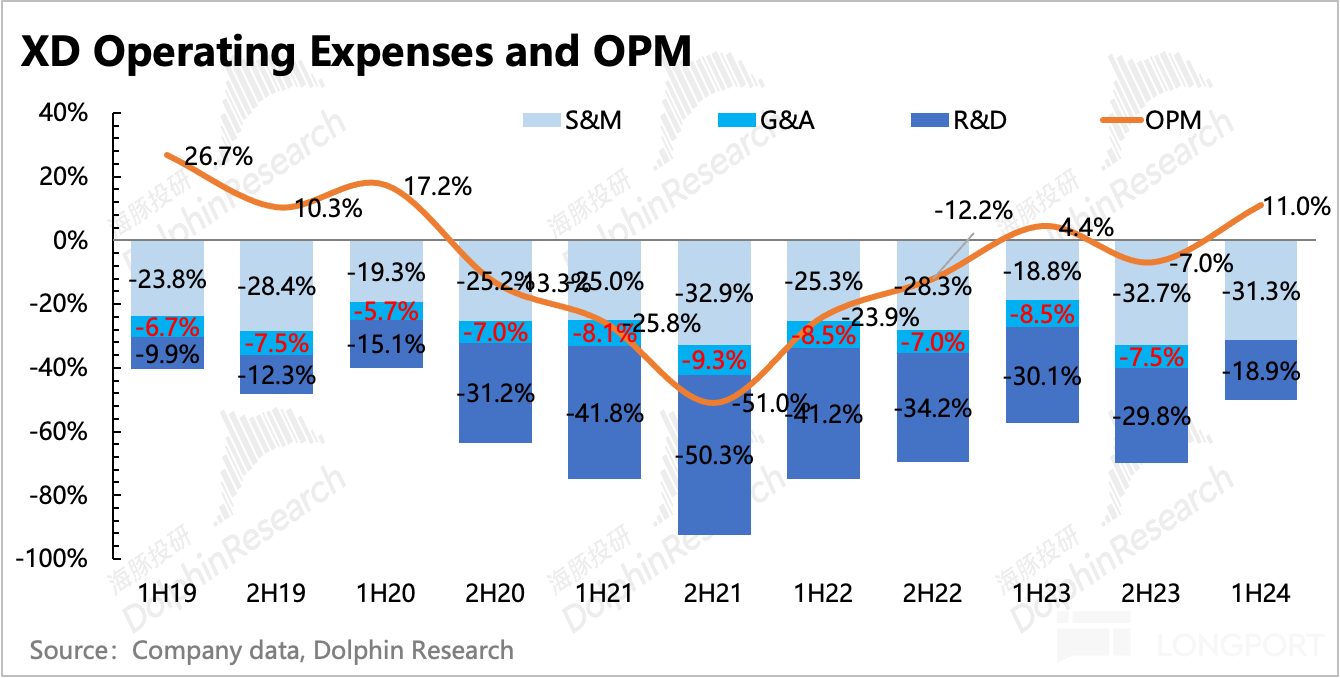

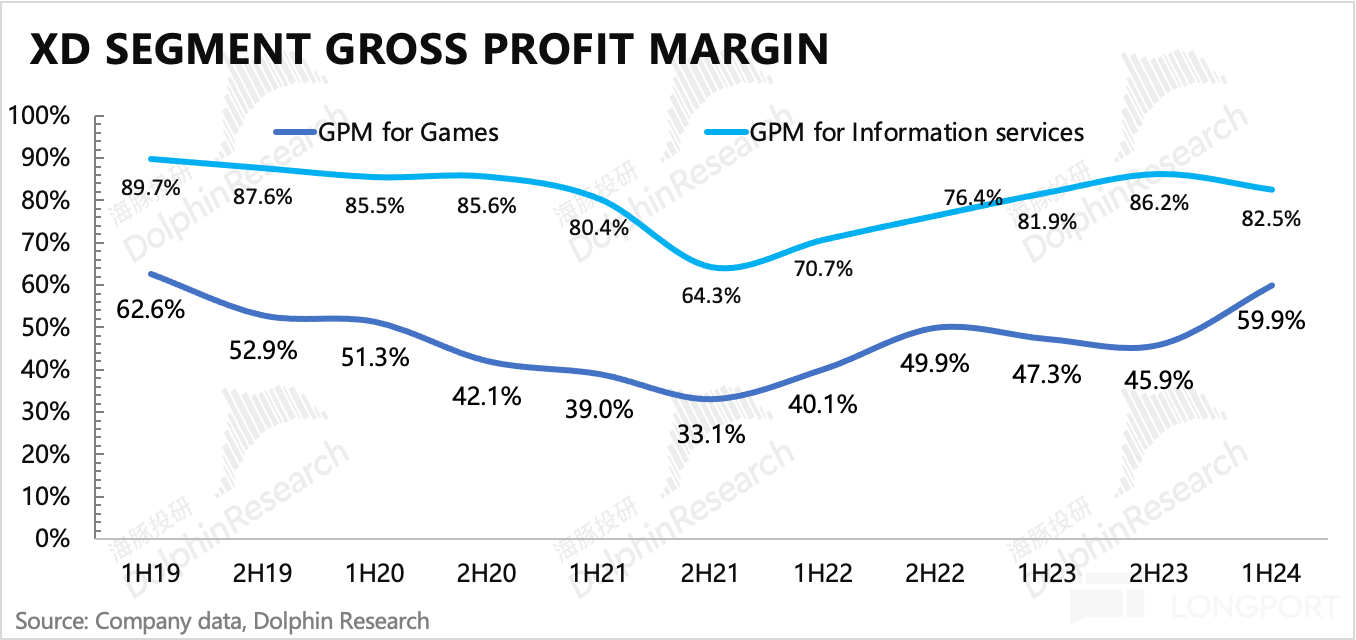

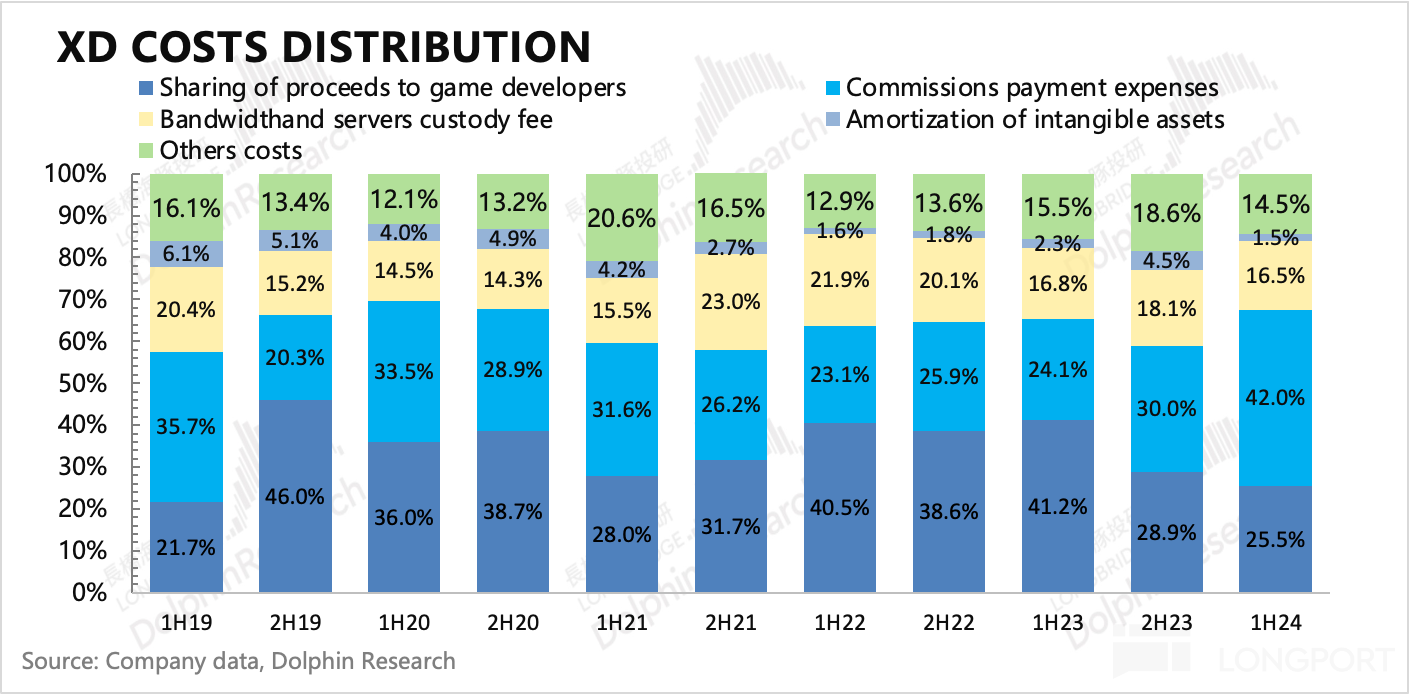

More self-developed games mean fewer external revenue sharing. Higher advertising conversion efficiency means that unit server costs can generate more revenue. These two factors are the core drivers of the company's overall gross margin increasing to 67% in the second half of the year, once again reaching a historical high.

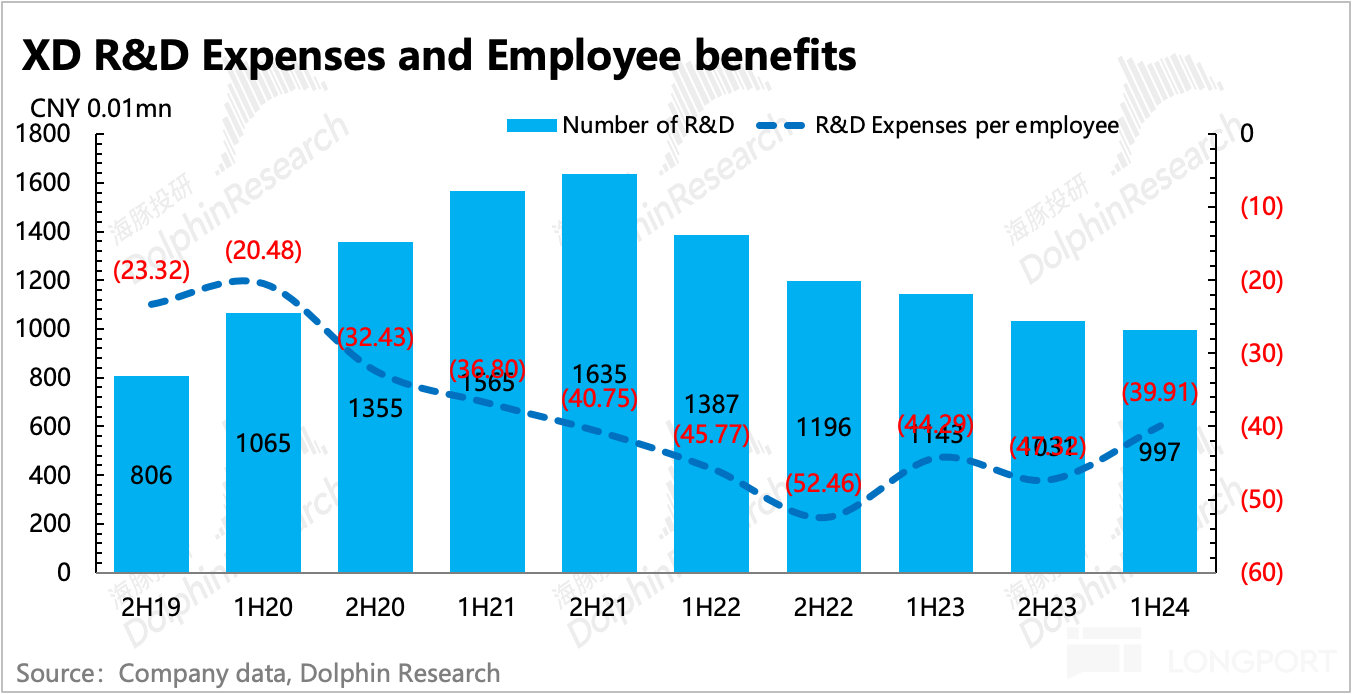

Of course, the company has also been actively reducing costs and increasing efficiency in the past year. Looking at the breakdown of expenses, the main factors leading to the decrease in R&D expenses are optimization of costs related to R&D staff reduction, server/usage rights/intangible assets, and property plants.

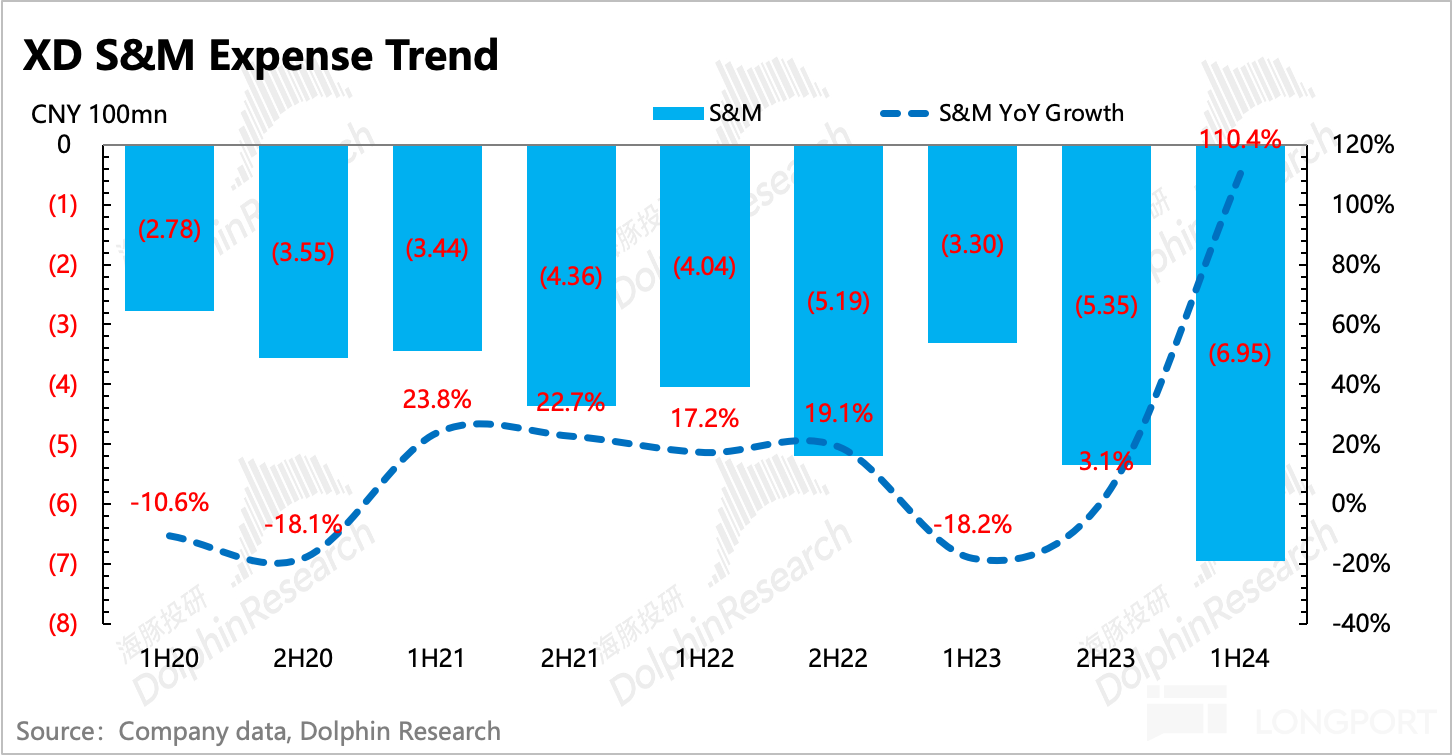

It is worth mentioning that marketing expenses doubled in the first half of the year, with growth exceeding revenue, indicating that monetization efficiency may not be high. However, the high marketing expenses brought about by the pre-marketing of the global overseas release of "Sword of the Bellflower" in August will gradually return to normal levels as revenue is confirmed in the second half of the year.

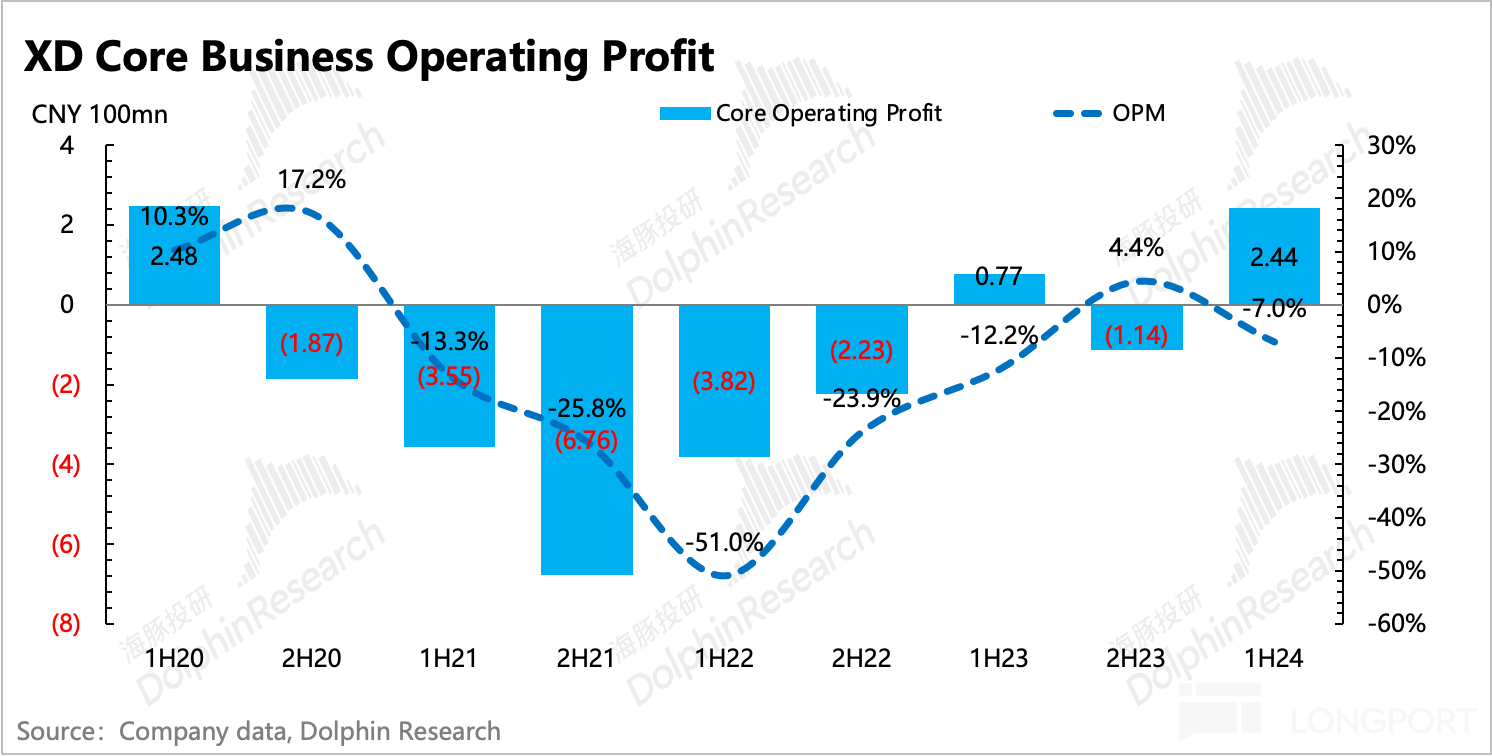

In the end, the operating profit of the core main business in the first half of the year was 244 million, with a profit margin of 12.2%, an increase of 5pct/20pct year-on-year/quarter-on-quarter.

4. Performance indicators vs. market expectations

Dolphin Jun's Viewpoint

This year is a rare year for exciting products, but for game companies, due to the relatively transparent revenue data, market expectations have already been factored into the stock price. Although TapTap follows an advertising monetization logic, the current traffic drive still largely depends on its own product cycle and performance. Perhaps when user penetration reaches a certain scale, the dependence on internal games will gradually decrease.

Therefore, from this perspective, the main factor causing changes in valuation is still based on the performance of the future pipeline (the following calculation is a rough estimate by Dolphin Jun, for cautious reference only):

1) In the short term, the game revenue in the second half of the year will not be bad, but market expectations are not low either. Currently, there are 3 factors that can bring incremental revenue: "Heartbeat Town" (public beta in July), domestic version of "Let's Muffin" (public beta in May), and overseas version of "Sword of the Bellflower" (launched in August). The main contribution of the new game increment comes from the first two mentioned above, but in the long run, "Heartbeat Town" takes the lead. As a game with a large DAU, it not only contributes to the incremental game revenue but also has a greater impact on driving TapTap user activity.

By the way, in the first half of the year, TapTap's monthly active users reached a historical high of 43.24 million, and it is expected to continue breaking records in the second half of the year. At the same time, in the first half of the year, TapTap intentionally slowed down its commercialization, and in the second half of the year during the summer game frenzy, it is expected to perform well.

2) From a medium-term perspective, after this product cycle, the pipeline for next year may be relatively weak. The current online plans mostly involve the overseas release of games from this year, such as the release of "Setting Off Muffin" in Japan and South Korea, and the global release of "Heartbeat Town."

In the financial report, the company mentioned that there are three games in development, including the previously reserved "Isa Restart Day." However, unlike "Heartbeat Town," Dolphin Jun finds it difficult to have relatively clear expectations for the performance of this game and remains cautious for now. It may be worthwhile to listen to the management's description during the afternoon earnings call.

Due to the unclear view of the 25-year performance trend, and considering the pullback of "Heartbeat" after a month, the current market value of 9.5 billion Hong Kong dollars implies a valuation of 14x P/E based on the expected performance in 24 years. Dolphin Jun still maintains a cautious neutral stance and needs to see if the company provides more concrete information on the three games in development during the conference call.

Below is a detailed financial report review:

1. TapTap: Great user growth, but the company restrains commercialization

In the first half of the year, TapTap's domestic monthly active users reached 43.24 million, a year-on-year increase of 27%, with a net increase of 5.59 million month-on-month. The driving factors include the overall industry supply increase and the company's position in the product cycle, with the performance of launched games being impressive (self-developed/exclusive titles are still the main logic driving traffic).

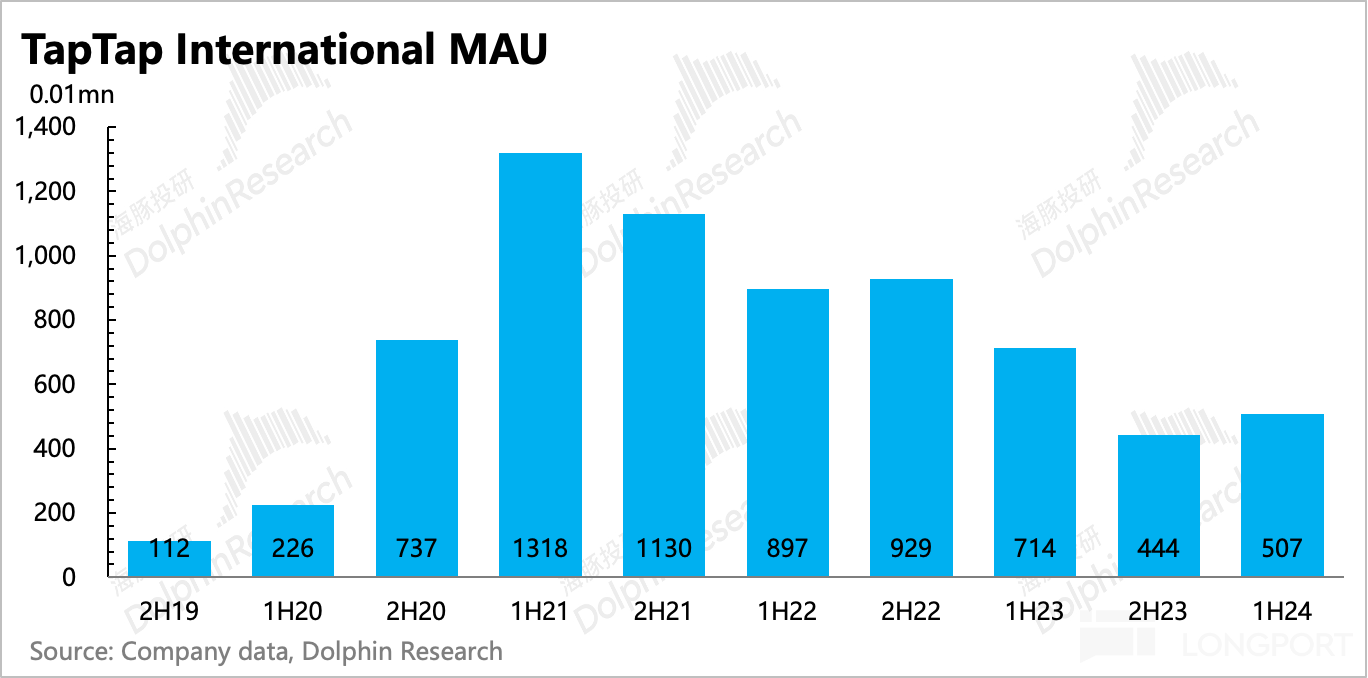

Although "Setting Off Muffin" performed well in the Hong Kong, Macao, and Taiwan regions, it may not rely solely on TapTap for distribution, so the international TapTap monthly active users still decreased by 29% year-on-year with the weakening of "Sausage Party," but compared to the second half of last year without "Setting Off Muffin," there is still an increase in user activity.

Additionally, the company mentioned in the financial report that user churn mainly comes from the Indian region, and the company's proactive contraction (significant reduction in marketing and customer acquisition expenses) has affected the overseas TapTap monthly active users.

The next big DAU game, "Sausage Party," may have some hope for "Heartbeat Town," otherwise TapTap's overseas expansion may have to temporarily come to a halt.

However, the expansion of TapTap's traffic has not fully reflected in monetization. The company stated that in the first half of the year, in order to ensure user experience, they were relatively restrained in advertising. Therefore, looking at TapTap's information service revenue, it reached 734 million in the first half of the year, a year-on-year increase of 22%, but the monetization value per user actually decreased year-on-year.

However, the greater the influence of TapTap users, the more they can attract more advertising placements and even exclusive/mainstream game releases in the long run (such as "Joy Fishing Master," "Ming Chao," "Sword of Legends 3" in the first half of the year), after all, TapTap still follows a zero revenue-sharing policy. Tencent previously challenged the Android channel publicly, indicating the long-standing challenges faced by developers in the channel.

In the first half of the year, the company controlled the advertising loading rate, which also reflects TapTap's position in the industry chain. Therefore, in the second half of the year, amidst the chaotic summer game battle, Dolphin Jun expects TapTap to still perform well.

II. Games: Enjoying the new product cycle, "Muffin" takes over from "Sausage Party"

Game revenue in the first half of the year increased by 29% year-on-year, reaching 1.49 billion, exceeding expectations but below market expectations. The year-on-year growth was mainly contributed by "Setting Off Muffin" launched at the beginning of the year and "Sword of Rind" launched at the end of last year, while the flagship game "Sausage Party" continued to decline. As of now, the top five games are "Setting Off Muffin" > "Sausage Party" > "Sword of Rind" > "Torchlight: Infinite" > "Ragnarok M".

"Setting Off Muffin," which was launched in January ahead of Hong Kong, Macau, and Taiwan, unexpectedly became a hit. The "unexpected" does not mean that this game did not perform well. "Muffin" was developed by the RO team, with successful experience in game style and type in the past ("Ragnarok Online," "Immortal Urala"), combined with some MMO elements as a placement game. Therefore, the initial market revenue expectations were not too low.

However, the scale of "Muffin's" popularity exceeded expectations, and it was not until July that "Muffin" dropped out of the top 10 in the Hong Kong iOS bestseller list, currently maintaining in the top 20. In the mainland market, due to intense game competition this year, the domestic version of "Muffin" dropped out of the top ten during the summer after being online for two months in May. However, the mainland market is large enough, according to Qimai data and the assumption of Android/iOS = 2:1, the domestic version's revenue is expected to reach nearly 1 billion after three months online, higher than Dolphin Jun's previous expectations in the last annual report review.

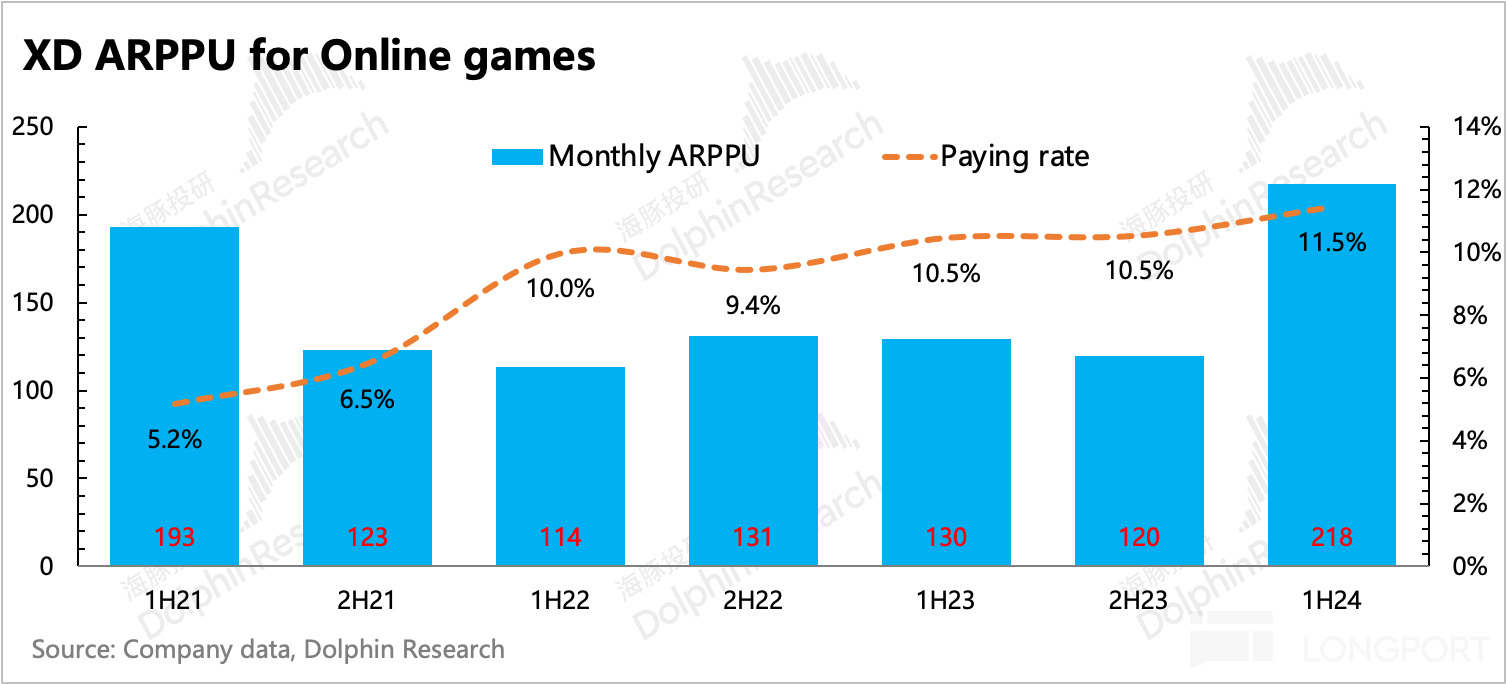

Breaking down to user and individual user payment situations, the main reflection is the "Muffin Adventure" pay-to-win nature - the average per capita payment ARPPU for the overall game business in the first half of the year increased by 68% year-on-year.

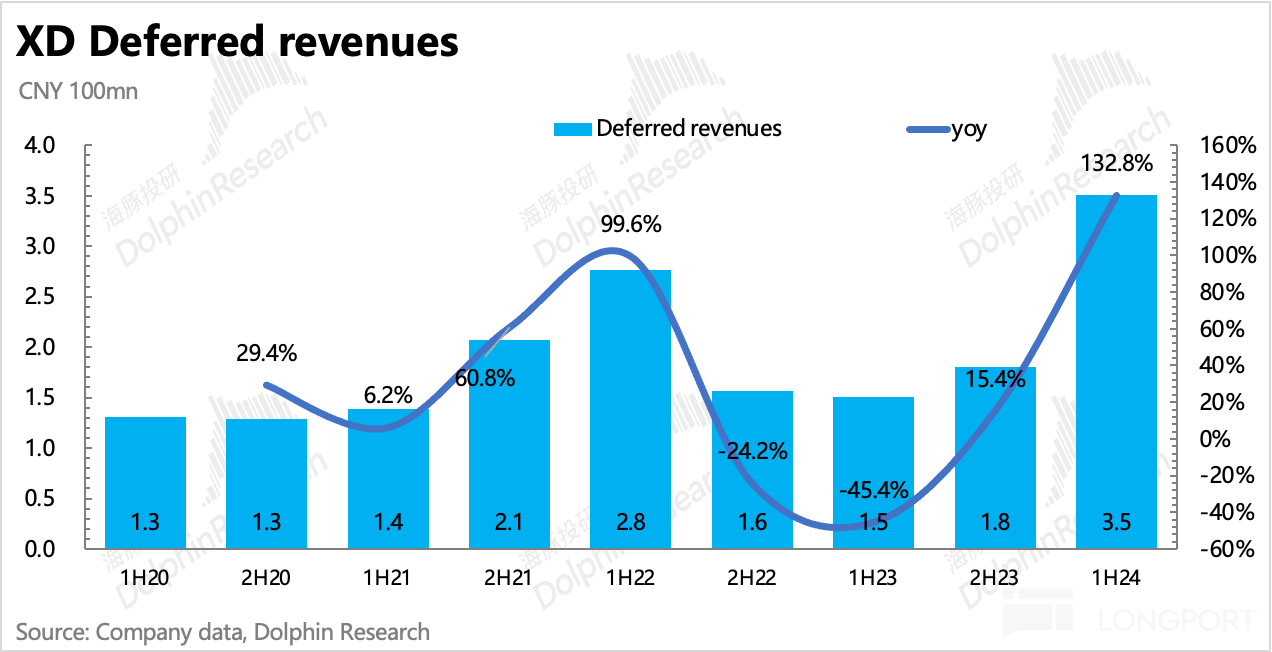

Looking ahead to the second half of the year, game revenue will truly peak. In addition to the new games released in the first half of the year (reflected as doubled deferred revenue), there are 3 incremental contributors: "Heartbeat Town" (public beta in July), domestic version of "Muffin Adventure" (public beta in May), and overseas version of "Sword of Ringeran" (launched in August).

a. The incremental contribution of new games mainly comes from the first two mentioned above, but in the long run, "Heartbeat Town" is more promising. Based on the current revenue situation according to Qimai data, Dolphin Jun predicts a full-year revenue of 500 million for "Heartbeat Town" this year, 1.2 billion for "Muffin Adventure", and 300 million for the overseas version of "Sword of Ringeran", totaling 2 billion in revenue. Based on Heartbeat's historical performance, 90% of the current revenue is confirmed, which is 1.8 billion in revenue.

b. For old games, still according to Qimai data, "Sausage Party" saw a 20% year-on-year decline in the first half of the year, with recent promotional activities slowing down (a combined 5% decline in revenue in July and August). However, considering the intense competition during the summer, assuming that the total revenue of old games led by "Sausage Party" will still decline by 10% year-on-year in the second half of the year. At the same time, "Muffin Adventure" saw a 10% month-on-month decline in Hong Kong, Macao, and Taiwan, meaning a total revenue of 1.3 billion from non-new games in the second half of the year.

c. Ultimately, the total revenue for new and old games in the second half of the year is 31 billion, nearly a 90% year-on-year growth, making this year undoubtedly a "highlight year in performance".

However, looking beyond this year to next year, based on the current "known" pipeline, there will be pressure on revenue growth. In the financial report, the company disclosed that there are three projects in development, besides the previously known "Isa Restart Day", other projects may need to wait for information disclosure during conference calls.

Overall, research and development speed and efficiency are still somewhat uncontrollable factors for Heartbeat, which is why Dolphin Jun believes that small and medium-sized game companies can only closely follow the product cycle to find short-term investment opportunities.

III. Self-developed high-gross-margin + stricter streamlined personnel = profits exceeding expectations

In the first half of the year, Heartbeat easily achieved a net profit of 251 million under the explosion of monetization, within the performance forecast range. Excluding gains and losses from financial assets value changes and financial management, the core operating profit reached 244 million, with a profit margin of 12%

More self-developed games mean less external revenue sharing. Higher advertising conversion efficiency means that unit server costs can generate more revenue. These two factors are the core drivers of the company's overall gross margin increasing to 67% in the second half of the year, once again reaching a historical high.

Looking into details, the game gross margin has reached 60%, comparable to leading game companies; while the TapTap advertising gross margin has declined month-on-month, mainly due to the company actively restraining advertising placements, compressing ad load rates to ensure a relatively good user experience for new users on the platform.

Of course, the company has also been actively reducing costs and increasing efficiency over the past year. Looking at the breakdown of expenses, the main factors leading to the decrease in R&D expenses are optimization of costs related to R&D layoffs, servers/usage rights/intangible assets, and property plants.

It is worth mentioning that marketing expenses doubled in the first half of the year, with growth exceeding revenue, indicating that monetization efficiency may not be high. However, the significant increase was due to the global overseas release of "Sword of the Bellflower" in August of the second half of the year, resulting in inflated marketing expenses. As revenue is confirmed in the second half of the year, the marketing expense ratio will gradually return to normal levels seen in previous years.

Dolphin Investment Research "Heartbeat" Historical Articles:

Financial Report Season

March 29, 2024 Conference Call " Heartbeat: Maintaining the Pace of Releasing 1-2 Self-developed New Games Every Year (2H23 Conference Call Summary)" Financial report review on March 28, 2024: "Doubler Stock" Excitement: Was 2023 too bad? The savior has arrived

Telephone conference on August 31, 2023: "Industry recovery, but investment in Doubler remains cautious (Doubler 1H23 performance conference call)

Financial report review on August 31, 2023: TapTap returns to pre-liberation, Doubler lacks a second explosive product

Telephone conference on March 30, 2023: Lessons from the past three years: no empty promises, talk about implementation (Doubler 2H22 conference call summary)

Financial report review on March 30, 2023: Doubler Company: TapTap falters, it's not easy to say "Doubler"

Telephone conference on September 1, 2022: Doubler: Accelerating the launch process of core games, seeking high-quality work (1H22 conference call summary)

Financial report review on August 31, 2022: Unexpected surprise, Doubler can be excited again

Telephone conference on March 30, 2022: Doubler Company: Hoping to achieve profit and loss balance through overseas expansion without a domestic license (conference call summary)

Financial report review on March 30, 2022: Doubler: Abyss after abyss, can overseas expansion be a "last-minute solution"? August 27, 2021 Conference Call "Summary of Exciting Call: Management's Plans for the Short and Long Term Future are Clear"

August 26, 2021 Financial Report Review "Exciting Financial Report: Market 'Urgent', Exciting 'Calm'"

March 26, 2021 Conference Call "Summary of Exciting Company's 2020 Performance Conference Call: The Transformation of the Gaming Industry is Not Immediate, Nor is Exciting's Growth"

March 26, 2021 Financial Report Review "Key Points of Exciting Investment: Patience, Patience, and More Patience"

March 1, 2021 Performance Warning Interpretation "Dolphin Research | After a Sharp Drop in Profits, Is Exciting 'Squatting Deep'? Perhaps Just a 'Fake Fall'"

In-depth

September 27, 2022 Overview "Can the 'Disappeared' Kuaishou, Exciting, iQIYI, Tencent Music, etc., Reverse Their Dilemma?"

February 1, 2021 "Dolphin Research | The 'Exciting Phenomenon' Behind: If Excited, Can You Take Action?"

December 29, 2021 "Dolphin Research | Heavy Survey: How Far is TapTap from the Chinese Version of Steam?"

December 16, 2021 "Dolphin Research | The 'Exciting Phenomenon' Behind: Why is the Market Excited?"

December 15, 2021 "Dolphin Research | The 'Exciting Phenomenon' Behind: Major Changes in the Gaming Industry!"

Risk Disclosure and Statement of this Article: Dolphin Research Disclaimer and General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.