After the slump, is there still hope for Chinese concept stocks?

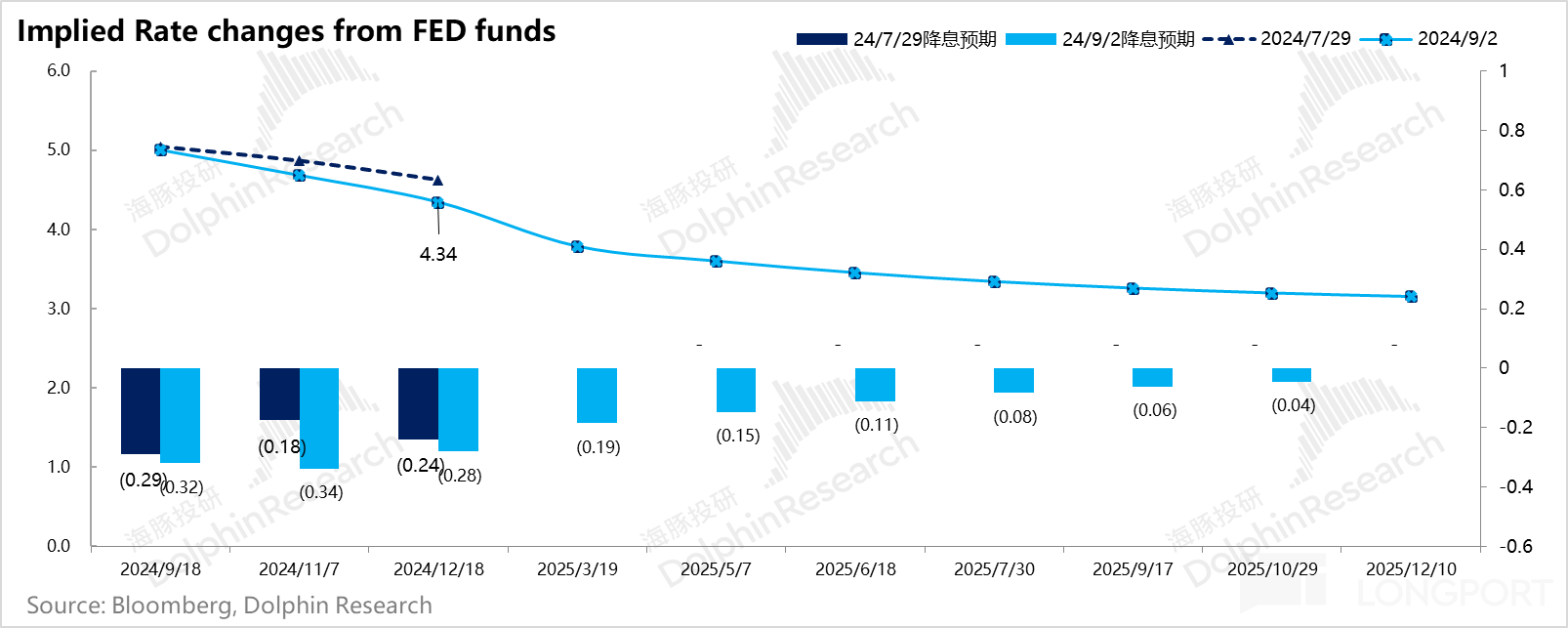

With the official stamp of Federal Reserve Chairman Powell at the global central bank meeting, the market has now fully priced in the expectation of a rate cut. However, the magnitude of each rate cut and the overall rate cut still depend on data for decision-making. Data has become simpler, focusing on three key factors - employment, inflation, and consumer spending.

This week, the most crucial August employment and wage data before the decision on the rate cut in September will be released. Last week, the most critical data was July's consumer spending, which remained relatively strong in July and does not support a significant rate cut.

I. Income Slows Down, Savings Make Up for It, Consumer Spending Remains Strong

Unlike the soft outlook shown by many consumer companies in the second-quarter earnings reports of US stocks, overall consumer spending in the US in July was still strong. Behind this strength, let's first look at the source of the money behind consumption:

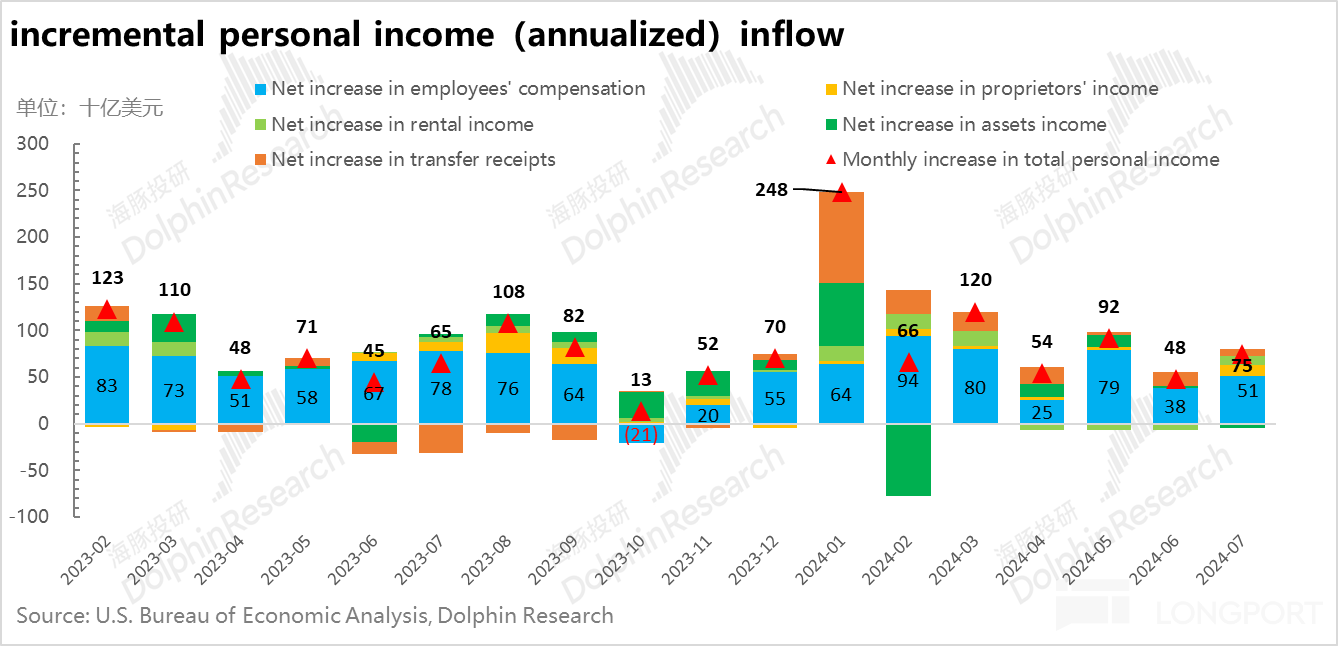

a. In July, the annualized increase in monthly income for the US population was $51 billion, with a month-on-month increase of 0.31%, equivalent to nearly 4% year-on-year growth. Therefore, whether looking at the absolute value of the increase or the year-on-year comparison, the overall income pool for residents is stable.

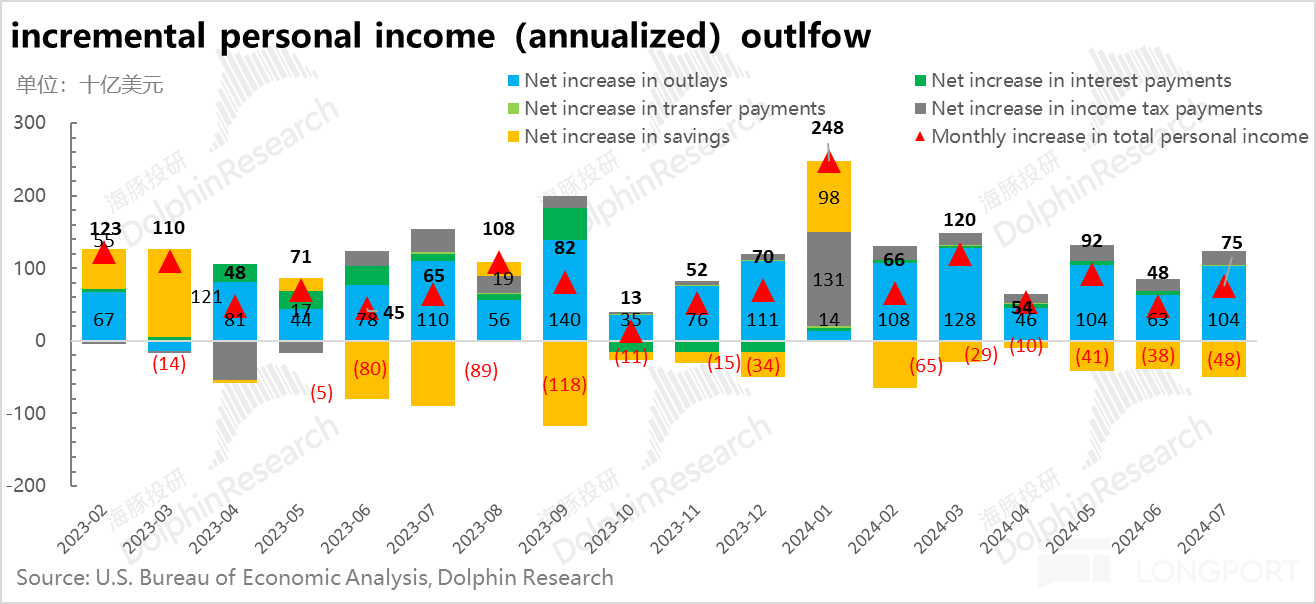

b. On the expenditure side, although the growth on the income side can only be described as stable, consumption was very strong: not only did all additional income convert into consumption, but in July, consumption once again significantly squeezed the proportion of income converted into savings, leading to consumer spending growing more than income, indicating strong domestic demand.

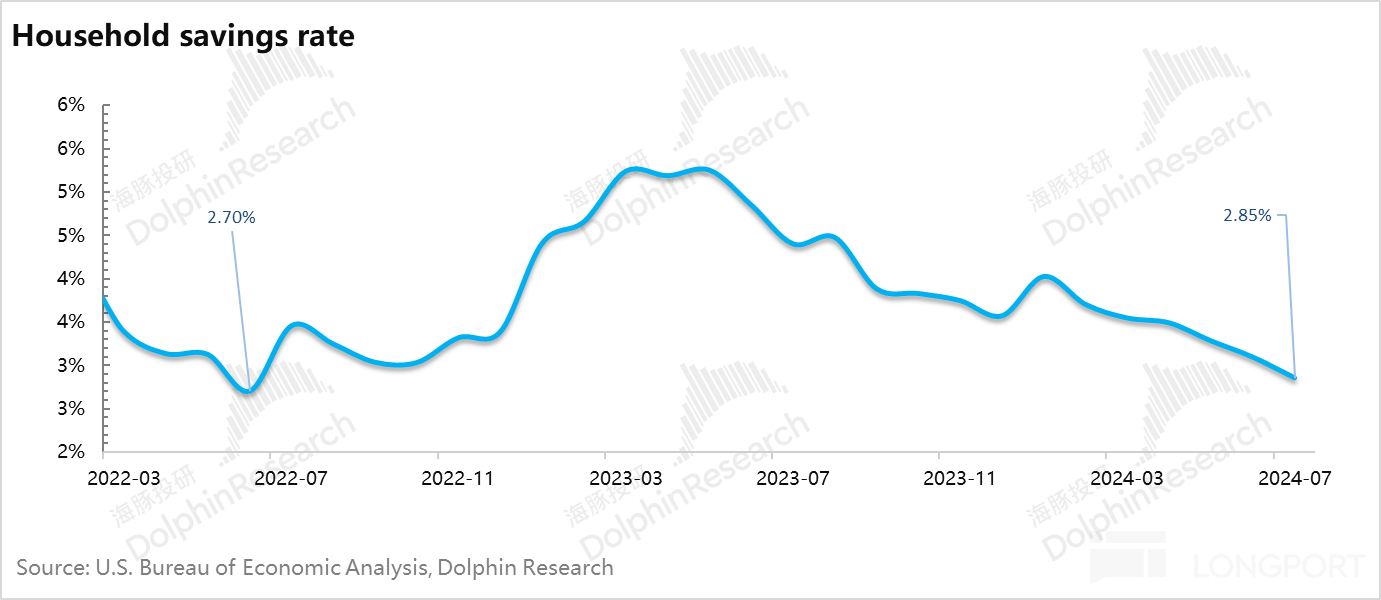

c. Savings Rate Approaching a New Low

With no significant increase in resident income, consumption continues to squeeze the savings rate. As a result, in July, the savings rate almost hit a new low since the helicopter money in 2022, at only 2.85%. This means that for every $100 of disposable income earned by US residents, only $2.85 is saved (whether this saving is in the form of deposits or investments).

As the two main sources of consumer spending, whether it is the growth in resident income (strong employment) or the squeeze on the savings rate (healthy resident balance sheet, confident residents not needing to save extra), it seems to be continuously flowing.

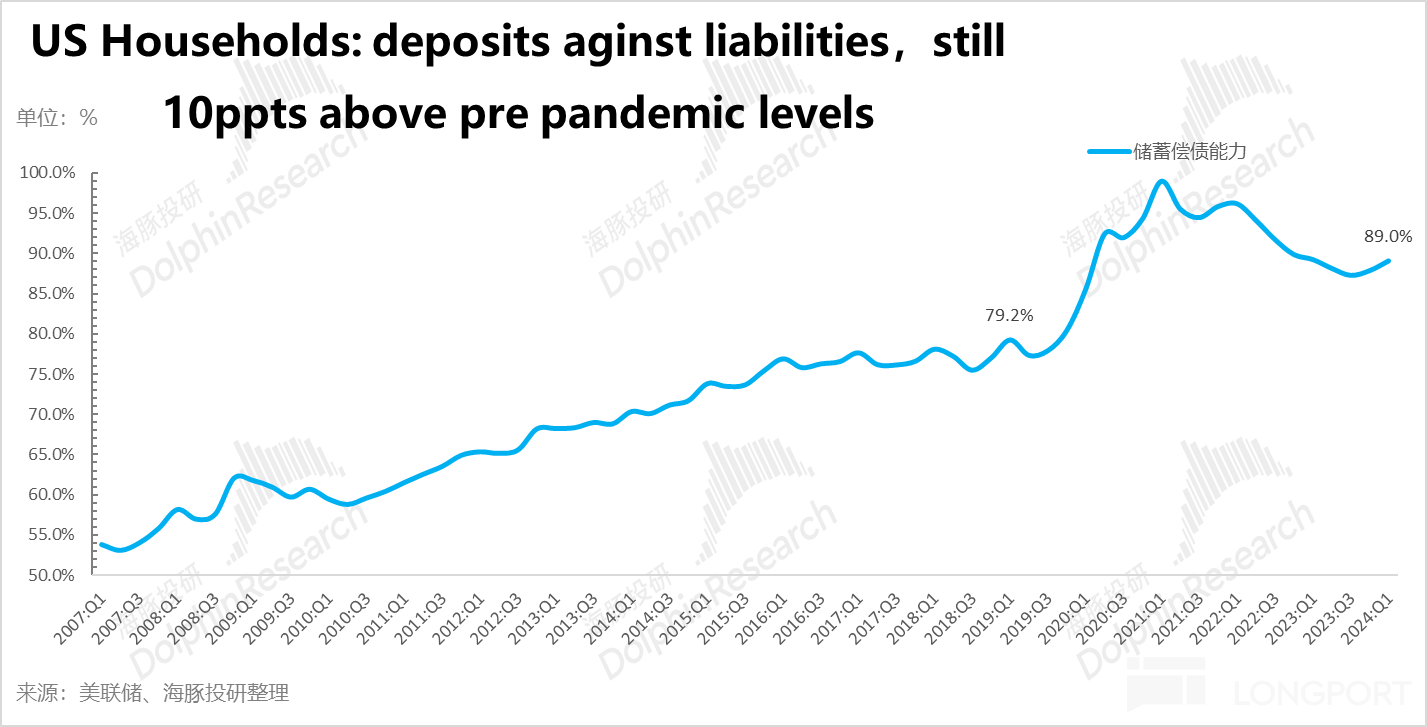

Especially with the ongoing squeeze on the savings rate, even though half of 2024 has passed, consumption can still effectively squeeze savings. This is mainly due to the deleveraging of the resident balance sheet since 2008, coupled with the helicopter money during the pandemic, further improving the resident balance sheet situation In this way, the current household balance sheet shows that savings have particularly strong ability to pay off debts, so there is absolutely no need to save money, and savings can also be continuously squeezed. As a result, household income + savings consumption continue to drive household consumption as a key pillar of GDP to move forward at a high speed.

With the continuous stability of domestic demand, although current prices are steadily declining, there is indeed a need to lower interest rates, but Dolphin Jun is skeptical about whether the magnitude is the expected 100 basis points in the market. With the market fully pricing in the rate cut, Dolphin Jun believes that the rate cut trade has basically run its course.

II. Chinese Assets: Can the US rate cut open up domestic monetary policy space?

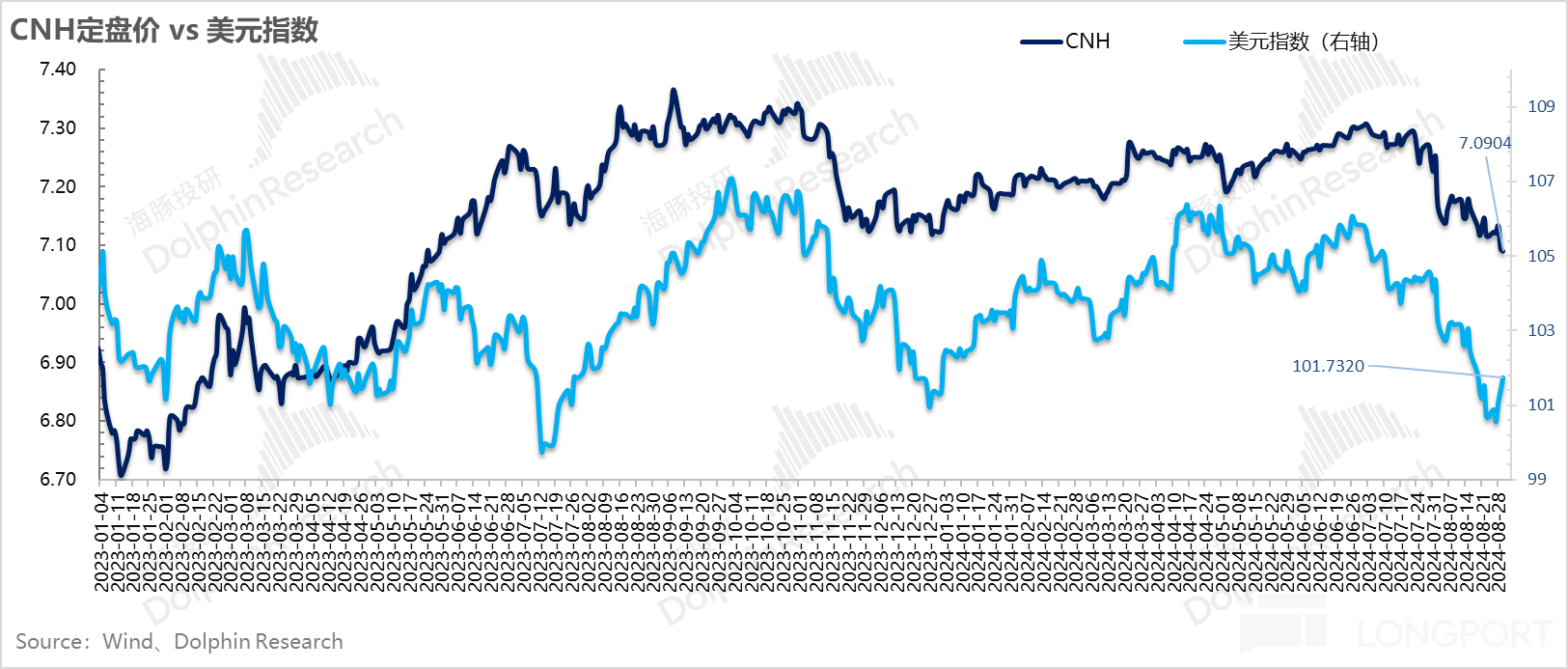

If the Federal Reserve cuts interest rates by 75 basis points this year and continues to decline next year, reaching around 3.5%. Then, can the RMB exchange rate improve? With the confirmation of the US rate cut expectations recently, the offshore RMB has risen to around 7.1.

In this scenario, can domestic assets open up some room for interest rate cuts or debt monetization under high domestic debt? Last week, news about reducing existing loan interest rates for residents and switching to mortgages to some extent, served as a small trial.

As for the current overseas-priced Chinese equity assets, after the baptism of the financial report season, whether it is the general weakness in internet advertising companies, fierce competition in e-commerce companies, conservative guidance from recruitment companies like Boss, or the widespread underperformance of consumer goods companies (such as beer companies and 9-9 restaurant chains that Dolphin Jun has seen), the market has fully realized the severity of performance realization. In the absence of effective policy stimulus, there is only one way left, which is to start cost reduction and efficiency improvement in a unified direction.

In terms of individual stock valuations, among the companies Dolphin Jun has seen, only pan-consumer companies in the domestic market, whether in advertising, e-commerce, general entertainment, or consumer goods, have mostly valuations ranging from single-digit PEs to around 20x PEs. To some extent, valuations have been slashed. The real question is, how many companies will follow the path of China International Travel Service, slashing PEs, falling in performance, and whether there is a true bottom in performance?

This question is to some extent a macro issue, and currently from a macro perspective, Dolphin Jun believes that as the US dollar enters a rate-cutting cycle, it can to some extent open up space for domestic policy execution, thereby at least playing a role in short-term improvement and helping achieve short-term valuation repair

III. Portfolio Rebalancing and Returns

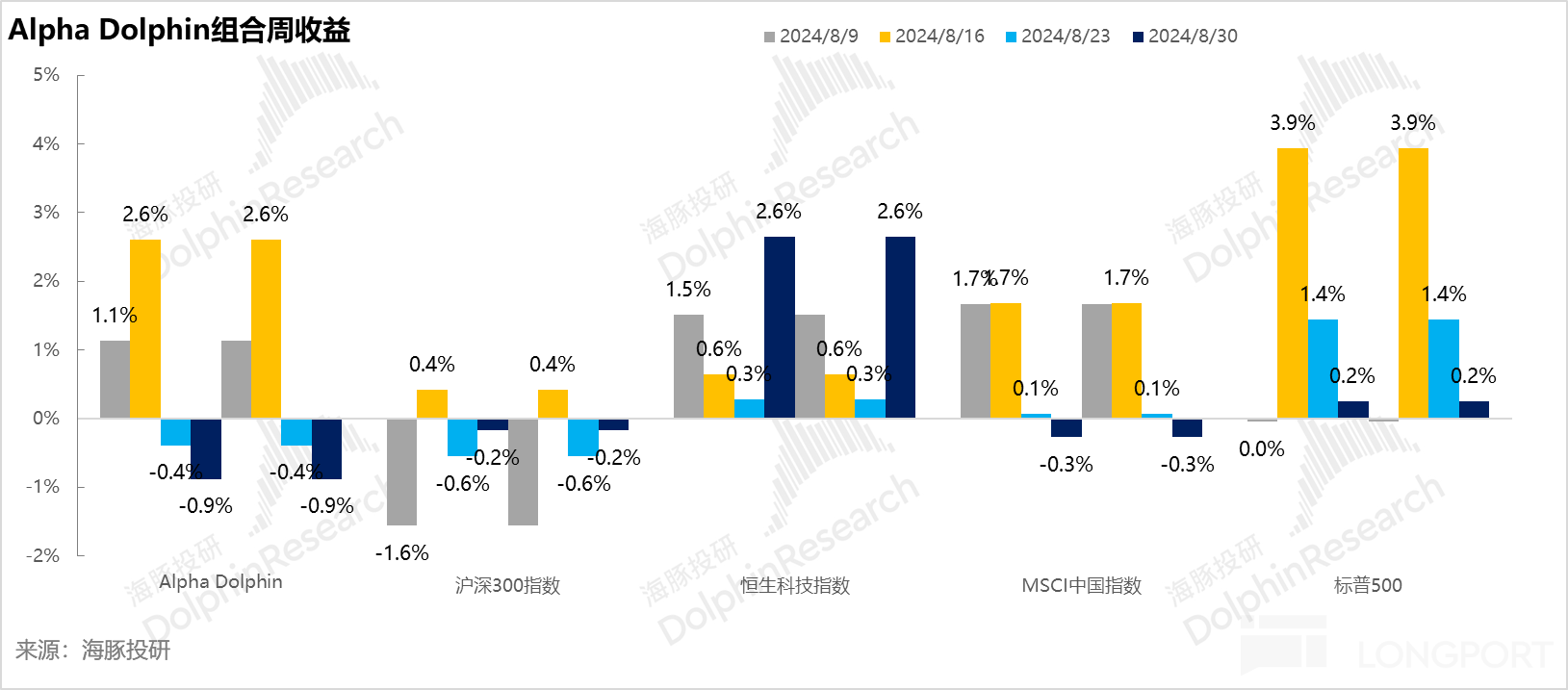

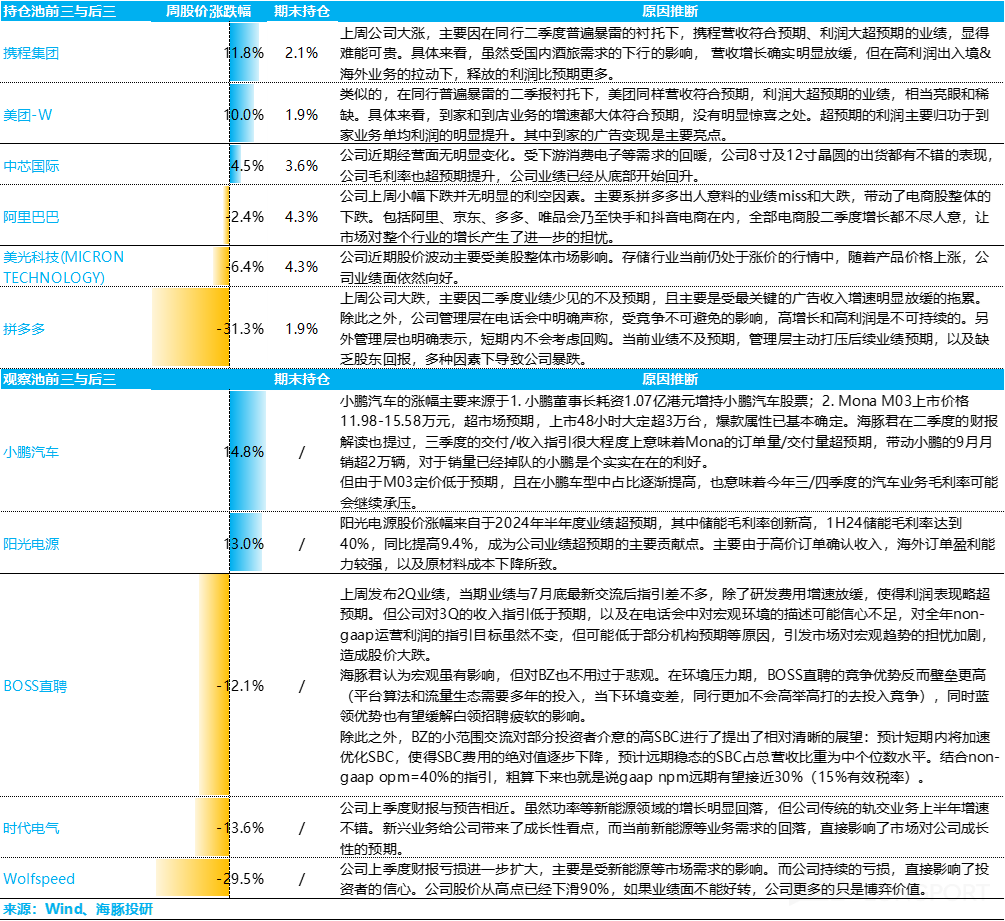

Last week, the portfolio did not rebalance, and the portfolio return decreased by 0.9%, underperforming the Chinese asset index - MSCI China (-0.3%), Hang Seng Tech Index (+2.6%), S&P 500 (+0.2%), and Shanghai-Shenzhen 300 Index (-0.2%). This was mainly due to the reckless performance of Pinduoduo during the conference call, which dragged down stocks of Alibaba and other peers. In the Hang Seng Tech Index, despite the good performance of Meituan last week, after Dolphin Jun reduced its position, it did not add back, unable to withstand the self-inflicted blow from Pinduoduo.

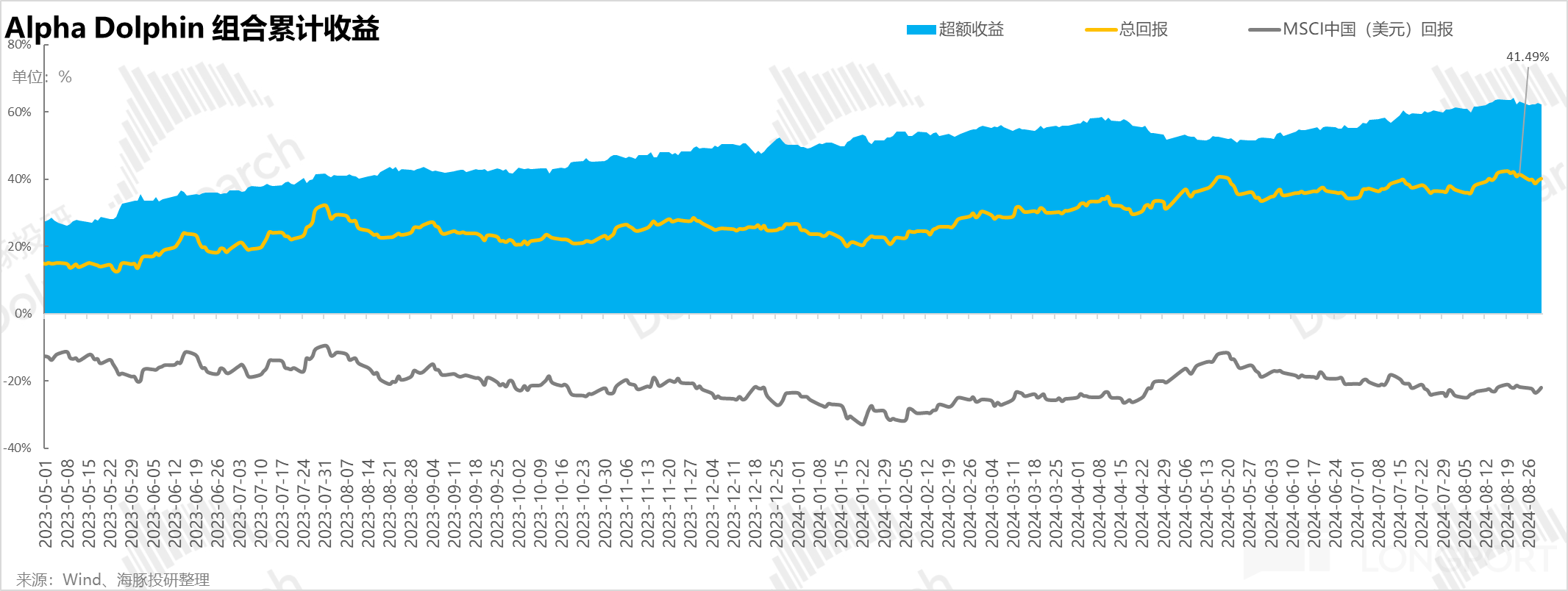

From the beginning of the portfolio testing to the end of last week, the absolute return of the portfolio was 40%, with an excess return compared to MSCI China of 62%. From the perspective of asset net value, Dolphin Jun's initial virtual assets were $100 million, which has now fallen to $142 million.

IV. Individual Stock Profit and Loss Contribution

Last week, due to the decline of AI stocks like Micron, and the crash of Chinese concept stocks in the US stock market including Pinduoduo, dragging down Alibaba as well, the portfolio performance was significantly weaker than the market. Meanwhile, Ctrip and Meituan, which performed relatively well, had reduced positions by Dolphin Jun, resulting in less exposure to hedge against the decline of Pinduoduo. Dolphin Jun explained the stocks with large fluctuations in the stock pool of interest last week as follows:

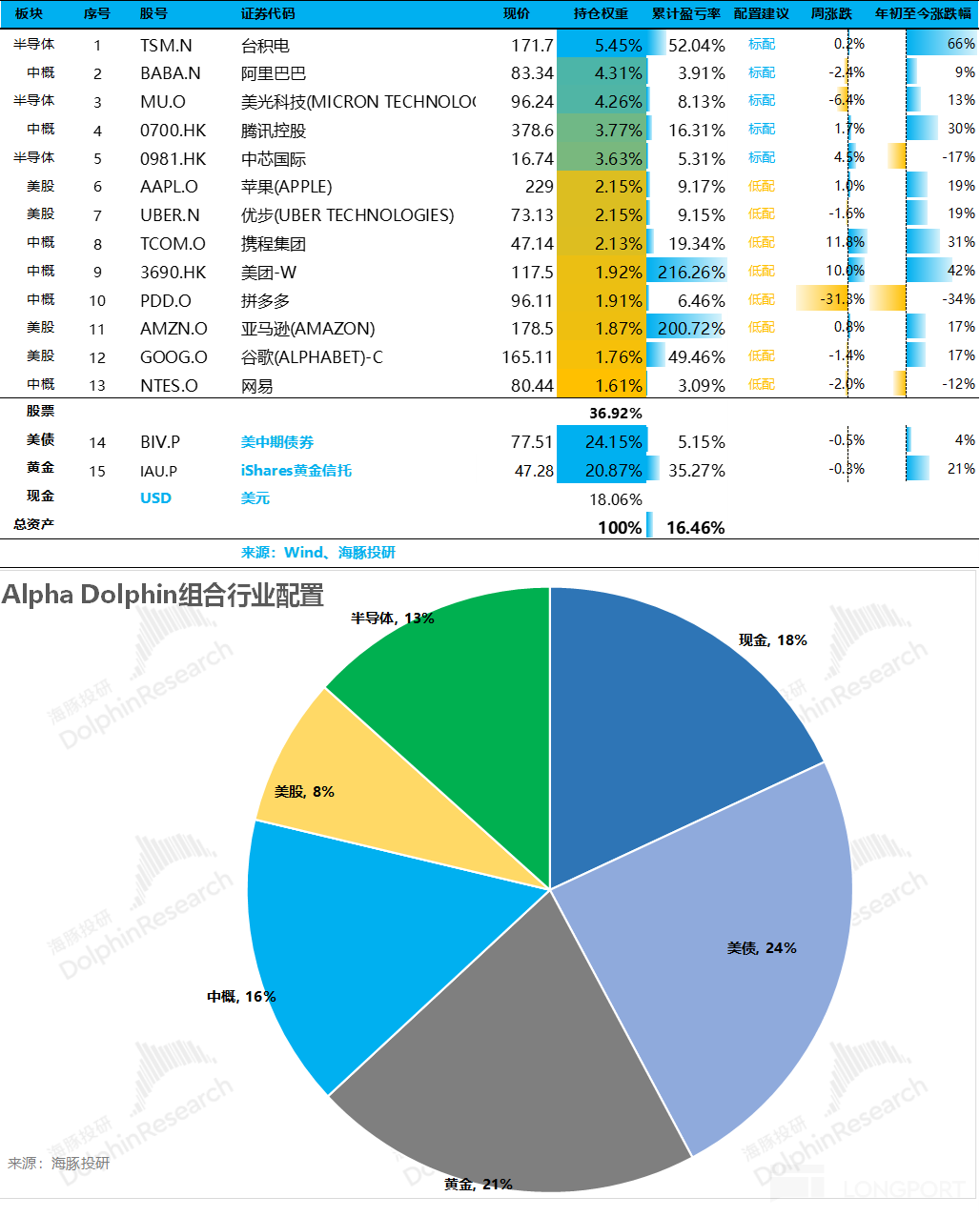

V. Portfolio Asset Allocation

The Alpha Dolphin virtual portfolio holds a total of 13 individual stocks and equity ETFs, with 5 core holdings and 8 equity assets underweighted. The rest is distributed in gold, US bonds, and US dollars cash. Currently, there is still a significant amount of cash and cash-like assets, which will gradually increase based on performance after the end of the earnings season. As of the end of last week, the asset allocation and equity asset weight of Alpha Dolphin are as follows:

VI. Key Events This Week:

With the sharp decline of Pinduoduo, Nongfu Spring, Li Auto, Boss Zhipin, China International Travel Service, and others, the earnings season for Chinese concept stocks has basically come to an end. Among the companies Dolphin Jun is focusing on, the only Chinese assets that performed relatively well in the second quarter are Pinduoduo, Ctrip, and Meituan. It is clear that the companies that can withstand this wave either have made waves overseas or have stabilized domestic supply-side while focusing more on their business (stabilizing market share in food delivery, no more reckless investments, improving governance) This week, among the companies that Dolphin Jun is focusing on in the US and China stock markets, only Nio and Broadcom are left. The key focus is as follows:

At that time, Dolphin Jun will first publish performance quick reads, in-depth analysis, breakdown of key data updates on LongPort, as well as meeting minutes. Please prepare the app, set up reminders, and be the first to receive Dolphin Jun's performance season analysis. For Dolphin Research webpage link, please click here.

Risk disclosure and statement of this article: Dolphin Research Disclaimer and General Disclosure

For recent Dolphin Research portfolio weekly reports, please refer to:

"US Stocks: Scared, then playing music?"

"US Stocks keep exploding with 'ghost stories', is there no bottom?"

"Economy, consumption are doing well, will the Fed really cut rates in September and cut three times in a row?" 《Are the economic fundamentals of American "brilliant" small-cap stocks nourishing?》

《The head of the US consumer train leaked, can we still trade the soft landing?》

《Deflated social zero, soft landing economy, will it drag down Chinese assets?》

《The US stock market's rate cut expectations kill "backstabbing", is it reliable this time?》 《Hong Kong stocks suddenly change face, to escape or to accept?》

《Chinese concept stocks in the U.S. stock market simultaneously pull back, who is the opportunity?》

《The United States in 2024, not a soft landing or no landing》

《Can earn more and spend more, why do American residents consume so fiercely》 《Don't Count on a Big Dip in US Stocks to Get On Board? Not Likely》

《Low-grade Inflation in the US, Can Chinese Concepts Still Rise?》

《Afraid to Chase the Seven Tech Sisters? Chinese Concepts Unexpectedly Benefited》

《Companies Relay on Residents to Support the Economy, US Rate Cuts Won't Happen Quickly》

《Giants Stagnate, Chinese Concepts Rise, Twilight or Style Change》

《2024, US Economy Won't Land?》 《Another critical moment! Will Powell bail out the spendthrift Yellen?》

《More mud and sand, how much faith can withstand the test?》

《Unstoppable deficits, supporting the dignity of the US stock market》

《2024 United States: Good economy, quick rate cuts? Too optimistic, will suffer losses》

《2023 United States: Rebirth through suicide》

《High interest cannot extinguish consumption, is America really thriving or just a bubble?》

《Second half of Fed tightening, neither stocks nor bonds can escape!》 《This is the most down-to-earth, Dolphin Investment Portfolio is launched》