Nio: Rarely not collapsed, happy to support the future?

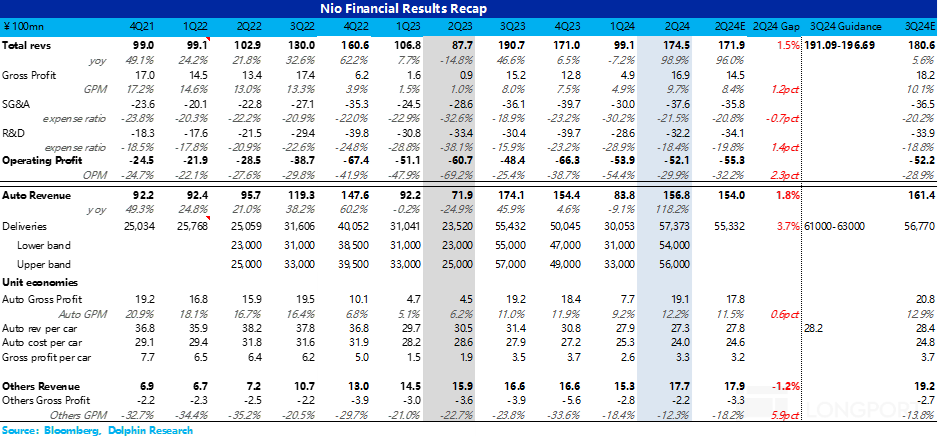

NIO Inc. (NIO.N) released its second-quarter 2024 financial report before the US stock market and after the Hong Kong stock market on September 5th Beijing time. Let's take a detailed look at the actual results for the second quarter:

1. Gross profit margin of vehicles exceeded expectations, mainly due to cost reduction: Despite a mix of old and new models this quarter, as well as a continued decline in unit prices under the BaaS model with a "pay for 4 get 1 free" promotion, the vehicle gross profit margin still exceeded market expectations. This was mainly due to the renegotiation of supplier procurement contracts in this quarter, leading to effective cost reduction on the cost side.

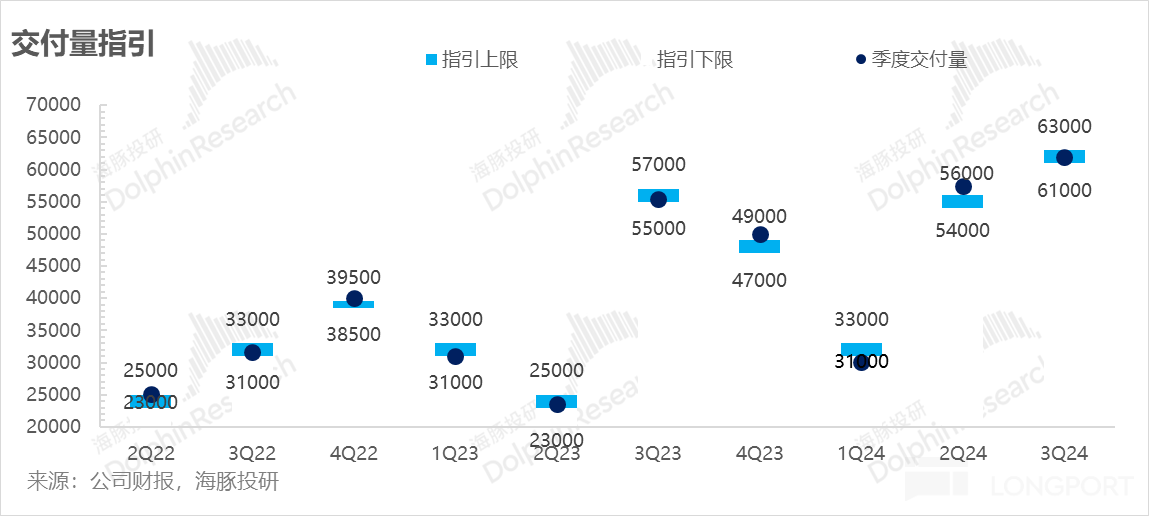

2. Third-quarter sales guidance in line with expectations: With sales in July and August already around 20,000 units each, the delivery volume guidance for the third quarter of 61,000 to 63,000 units implies sales of 21,000 to 23,000 units in September. This basically means that the contribution of the L60 delivered in September is an increase of up to 3,000 units. Since deliveries of this model only began in late September, sales are generally within expectations.

3. Implied selling price in the third quarter finally rebounded after two consecutive quarters of decline: The implied vehicle unit price in the third quarter increased by 11,000 yuan compared to the previous quarter, indicating that all old models were cleared in the third quarter and only 2024 models were sold. The impact of the L60 deliveries in late September on the third quarter is minimal, leading to a rebound in the vehicle unit price.

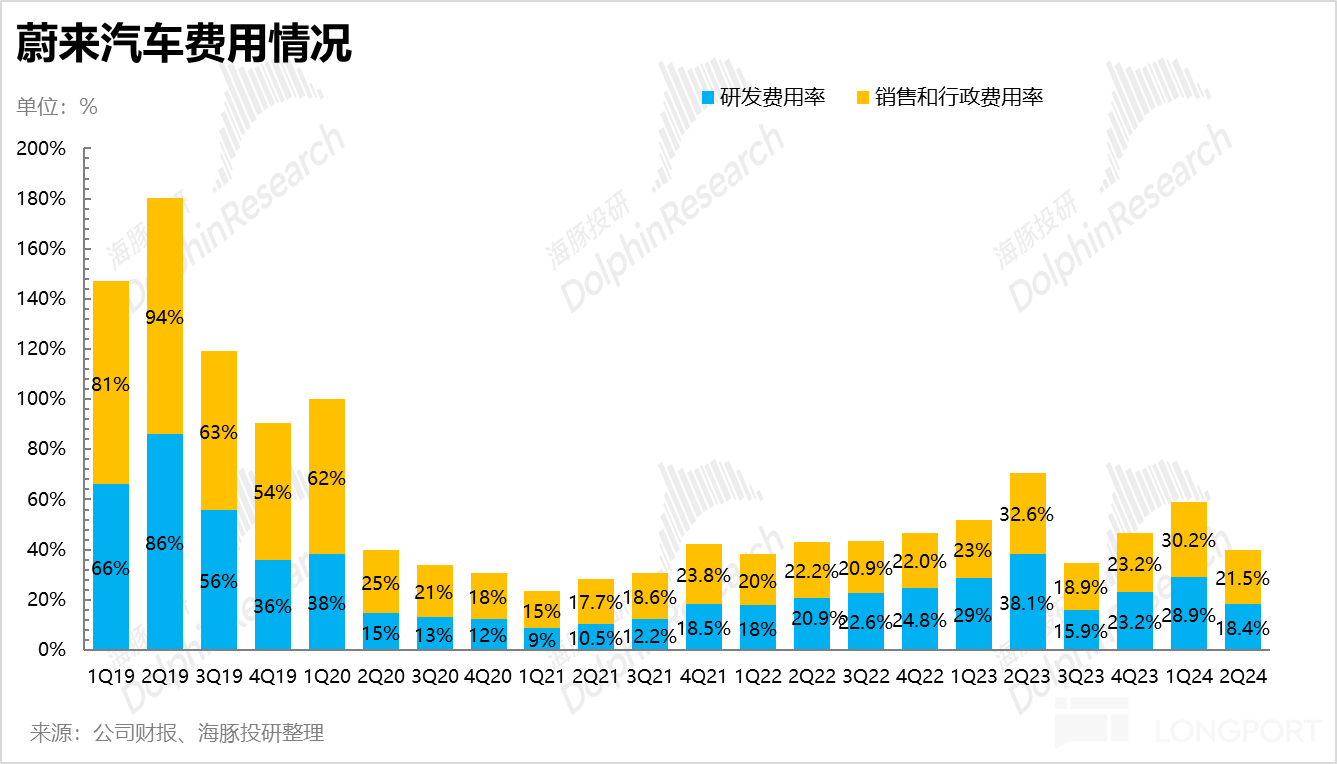

4. However, operating expenses remain high, mainly due to a significant increase in sales expenses: This quarter's Non-GAAP research and development expenses were 2.9 billion, within the company's guidance of under 3 billion. However, sales expenses this quarter saw a significant increase, rising by nearly 800 million compared to the previous quarter. This is mainly expected to be due to 1) the upcoming delivery of the Luhu in September, the expenses of opening new stores (105 stores), and the costs of recruiting sales staff; 2) the introduction of the 2024 models for delivery starting in March, leading to an increase in marketing expenses.

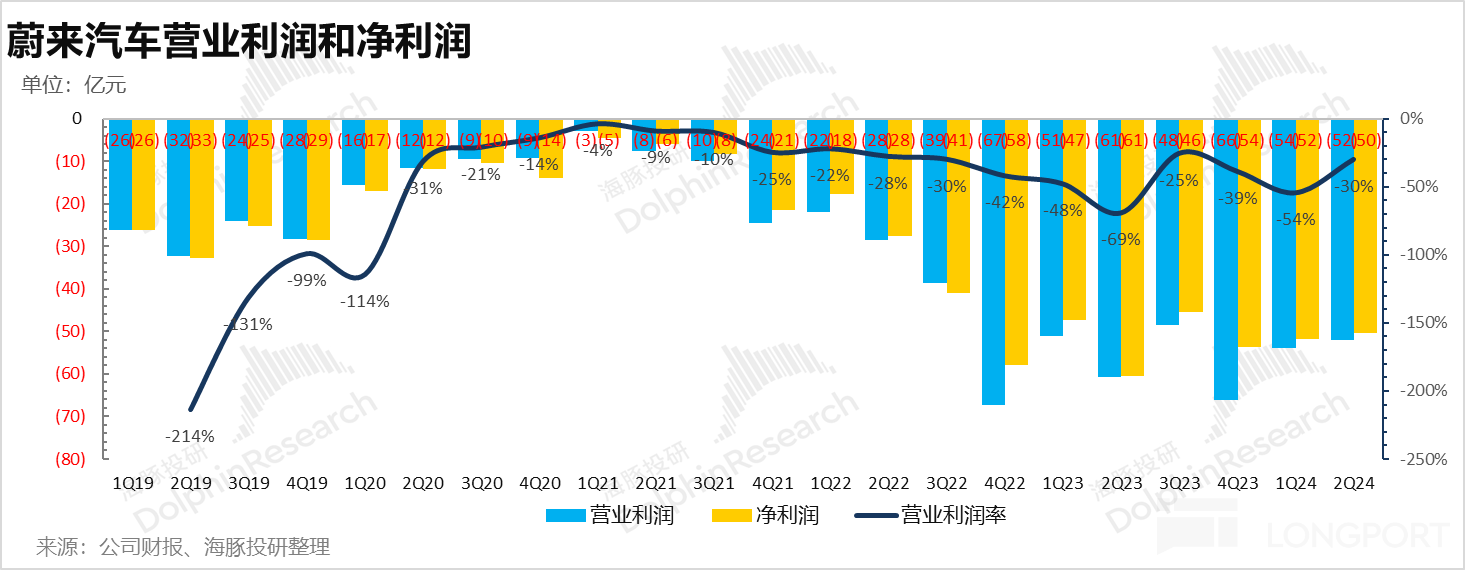

5. Operating loss in this quarter still exceeds 5 billion: Although there was a significant improvement in gross profit this quarter, mainly due to cost reduction in the vehicle side and reduced losses in other businesses, operating losses still exceeded 5 billion, reaching -5.2 billion. This led to a further decline of 3.7 billion in cash and cash equivalents for this quarter.

Dolphin Research's Viewpoint:

As the last Chinese concept stock to release its performance, Dolphin was initially nervous, but the actual results turned out to be safe.

With sales already transparent, the really good news this time is that the per-vehicle gross profit margin did not disappoint. Besides the growth in sales, the company explained that effective cost reduction was achieved due to renegotiations with suppliers, benefiting the gross profit margin in the second quarter.

In terms of the crucial guidance for the next quarter, it appears that the main NIO brand can maintain a monthly sales volume of around 20,000 units. The delivery of the Luhu will begin in late September, providing some incremental volume, but since it is not a full delivery month, the increase is not significant. The company's guidance of 61,000 to 63,000 units for the third quarter is basically within expectations However, the implied unit price of 19.1-19.7 billion RMB is approximately 282,000 RMB, which is basically within expectations. It is expected to be higher than the previous quarter, and the return price probably implies that the previous old cars have been mostly cleared out, and it will be all about selling new cars completely. The gross profit margin of the automobile is expected to continue to increase quarter-on-quarter. Dolphin Jun predicts that based on the return price of the unit, the gross profit margin of the automobile business in the third quarter is expected to continue to increase quarter-on-quarter.

In terms of expenses, the increase in the three expense categories this quarter is mainly due to the rise in sales expenses. However, due to the launch of the 2024 new models + the addition of stores under the LeDao brand and newly recruited sales personnel this quarter, it is relatively understandable. But the guidance that the year-on-year increase in sales expenses should not exceed 20% may indicate that it will be difficult to reduce sales expenses in the second half of the year, and they may continue to increase. Finally, despite the increase in operating losses due to the rising sales expenses, it still stands at -5.2 billion.

Overall, this performance is not particularly impressive, but considering its sales volume expectation of 210,000-220,000 units, the 2024 P/S ratio (only for car sales business) of only 1-1.1 times, it is more than sufficient.

Below is a detailed analysis:

I. Making money by selling cars? This quarter mainly relies on cost reduction!

As the most crucial indicator every time the results are released, let's first look at NIO's profitability from selling cars.

Since NIO provided guidance on the gross profit margin of the automobile business before, with reduced promotions, it is expected that the gross profit margin of the automobile business in the second quarter will return to double digits. Therefore, the market expects NIO's gross profit margin from the automobile business in the second quarter to increase to around 11%-11.5% quarter-on-quarter, while NIO's actual gross profit margin from selling cars is 12.2%, exceeding market expectations.

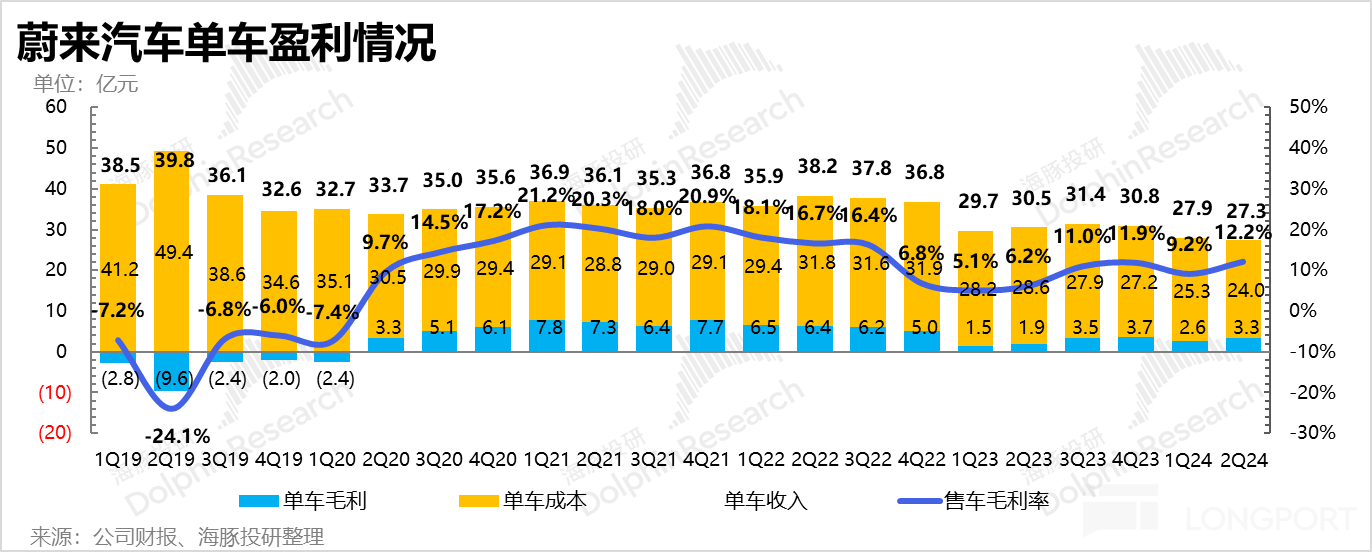

If we break down NIO's performance in automobile gross profit margin this quarter from the perspective of unit economics, the better-than-expected automobile gross profit margin is mainly due to the cost reduction of the unit:

1) NIO's average unit price in the second quarter was 273,000 RMB, lower than the market's expected 278,000 RMB

In the second quarter, the average unit price of the car was only 273,000 RMB, a decrease of 6,000 RMB from the previous quarter, lower than the market's expected 278,000 RMB, mainly affected by the following factors:

① NIO's 2024 models have been delivered successively since March 2024. In the second quarter, they were still in the period of mixed sales of old and 2024 models. Due to significant discounts on the old models, the unit price did not increase effectively this quarter (ET5, ET5T, ES6, EC6 received discounts of 24,000-32,000 RMB; ES8, EC7, ES7, ET7 received discounts of 32,000 RMB).

Delivery time for 2024 new models

② Negative impact of model structure: The proportion of NIO's lowest-priced models ET5+ES6 in the model structure increased by 4% quarter-on-quarter;

③ NIO announced a new BaaS policy on March 15, which involved two discount policies:

a. NIO lowered the rent under the BaaS model, with a reduction of 26%-33%. However, NIO explained that the adjustment of rental prices did not have a significant impact on revenue and gross profit margin, mainly based on assumptions about battery life and battery operation optimization b. "Pay 4 Get 1 Free" Promotion - For example, leasing 4 months of batteries and enjoying 1 month free promotion (up to 5 years), with an impact on the single bike price of approximately less than 6000 yuan, but this promotion started to decline in June.

In the end, Nio's second-quarter single bike revenue was 273,000 yuan, lower than the market's expected 278,000 yuan.

2) Second-quarter single bike cost 240,000 yuan, lower than the market's expected 246,000 yuan

The second-quarter single bike cost was 240,000 yuan, a decrease of 13,000 yuan compared to the previous quarter, lower than the market's expected 246,000 yuan, which was also the main reason for the increase in the car's gross profit margin this quarter.

The continued decline in single bike cost this quarter was mainly influenced by two factors:

① Release of economies of scale: Nio sold 57,000 cars in the second quarter, hitting a historical high, with a 91% increase in sales volume compared to the previous quarter, leading to the release of economies of scale and a decrease in the per bike amortized cost.

② Savings in supplier procurement costs: Nio renegotiated supplier contracts in the second quarter, effectively reducing procurement costs for the quarter.

3) Single bike gross profit increased to 33,000 yuan

The single bike price decreased by 6,000 yuan, but the single bike cost saved 13,000 yuan compared to the previous quarter. In the end, for every car sold in the second quarter, Nio earned a gross profit of 33,000 yuan, an increase of 7,000 yuan compared to the previous quarter.

II. Sales volume guidance and unit price guidance for the second and third quarters are generally in line with expectations

1) Third-quarter sales volume guidance of 61,000-63,000, basically in line with expectations

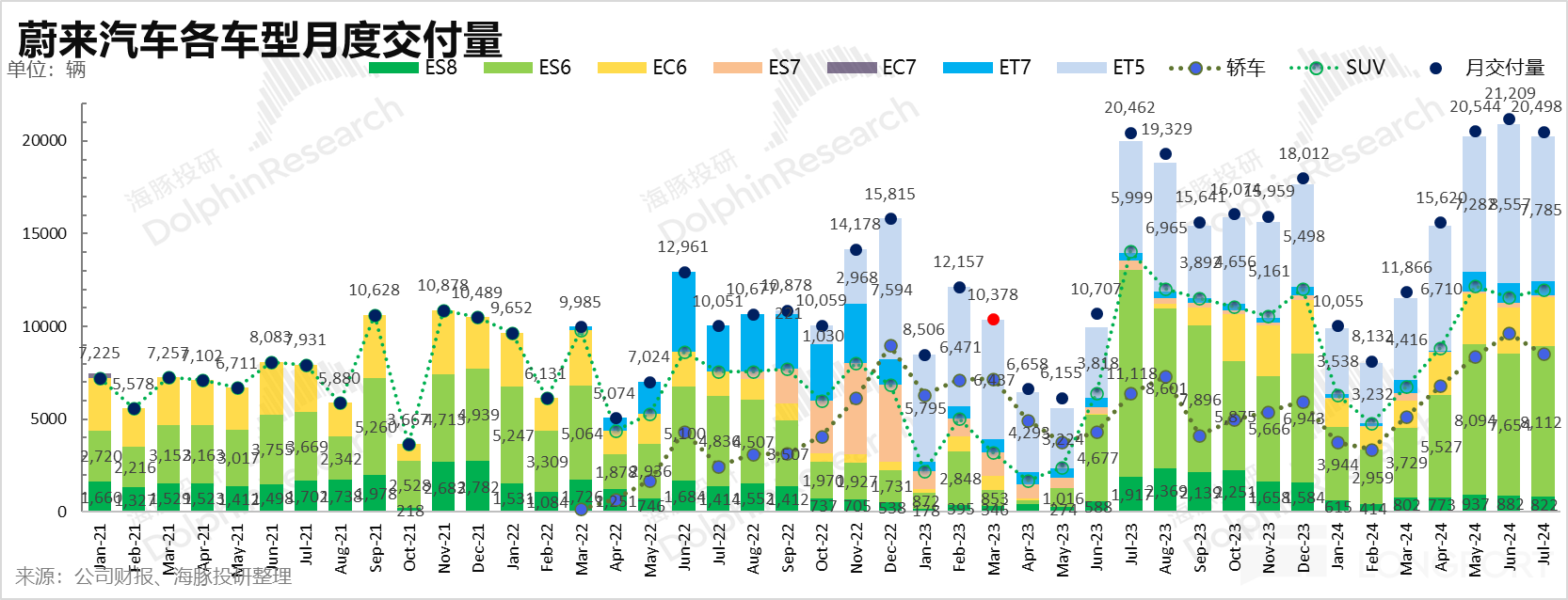

Nio expects third-quarter sales volume guidance of 61,000-63,000 units. As July/August sales have been strong, both around 20,000 units, the sales volume guidance implies sales in September will be between 20,000-23,000 units.

With the launch and delivery of the L60 in late September, assuming the main brand maintains a monthly sales trend of 20,000 units, it means the delivery volume of the L60 in its first month of launch will be around 3,000 units (not a complete delivery month), which will not have a significant impact on the second quarter.

2) Third-quarter revenue implies a unit price of 282,000 yuan, finally starting to rise after two consecutive quarters of decline!

Nio's third-quarter revenue guidance is 19.1-19.7 billion, with an estimated 1.9 billion from other businesses, corresponding to a unit price of 282,000 yuan, basically within the market's expected range of 284,000 yuan The single-car price in the third quarter finally started to rise after two consecutive quarters of decline, mainly due to:

All cars sold in the third quarter are the new 2024 models, without the drag of discounted old models.

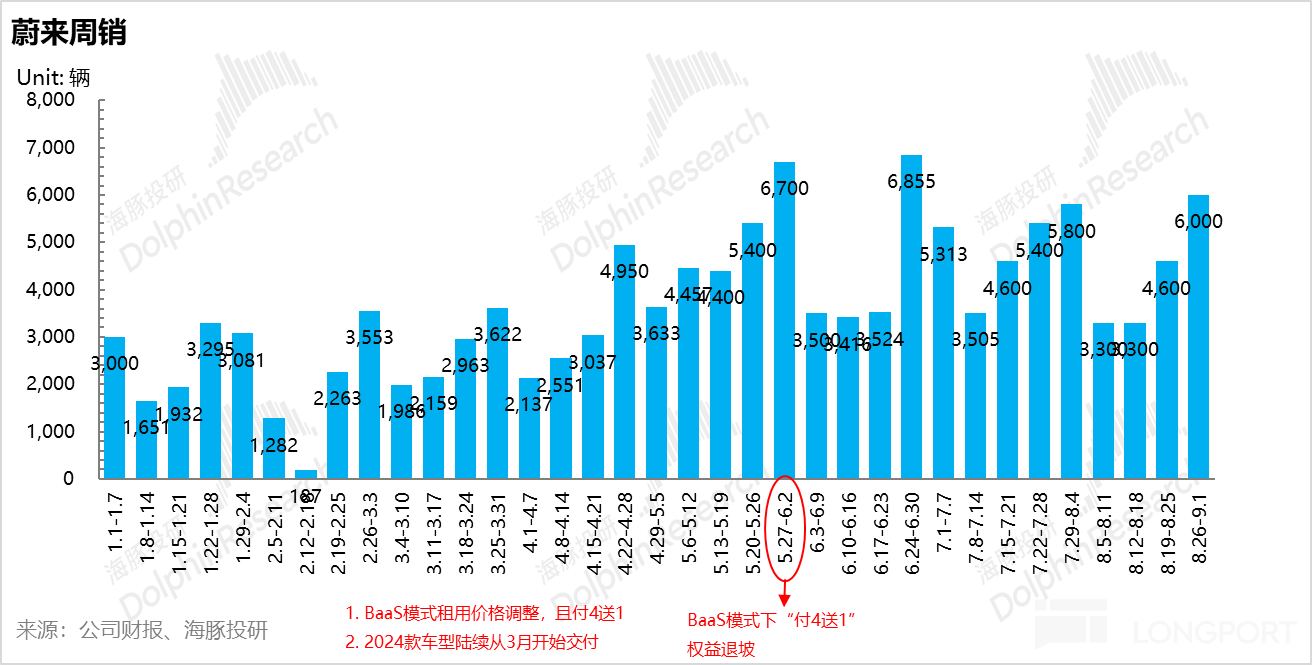

The BaaS model's "pay for 4, get 1 free" policy tapered off in June. Although it temporarily returned from September 2nd to 8th, the impact on unit price was much weaker compared to the drag of around 6,000 yuan per unit in the second quarter due to the short duration.

The Leador L60, with a starting price of only 219,900 yuan, had a small increase in deliveries starting in late September, resulting in a low proportion of overall sales in the second quarter.

Dolphin Jun predicts that based on the rebounding single-car prices, the gross profit margin of the automotive business in the third quarter is expected to continue to increase compared to the previous quarter.

III. Second Quarter Deliveries Back on Track

NIO delivered 57,000 vehicles in the second quarter, a 91% increase compared to the first quarter, exceeding NIO's previous guidance of 54,000 to 56,000 vehicles for the second quarter.

The rebound in NIO's second-quarter sales was mainly influenced by several factors:

The 2024 models started deliveries in March, enhancing product competitiveness.

The release of sales capacity from the previously increased sales force.

NIO adjusted its battery leasing policy, reducing BaaS rents by about 26%-33%, while also introducing the "pay for 4, get 1 free" offer (equivalent to an 20% discount, up to 5 years, but tapered off in June). After the rent reduction, the adoption rate of BaaS increased from the previous 20%-30% to 60%-70%, significantly boosting NIO's sales and order volume.

The market was initially concerned that the BaaS model (especially the "pay for 4, get 1 free" offer) would only provide short-term stimulus to sales and lack sustainability, especially given the pessimistic second-quarter sales guidance. However, after the BaaS model's "pay for 4, get 1 free" benefits tapered off, NIO still maintained monthly sales of over 20,000 vehicles, dispelling market concerns and doubts.

Let's take a look at NIO's overall situation:

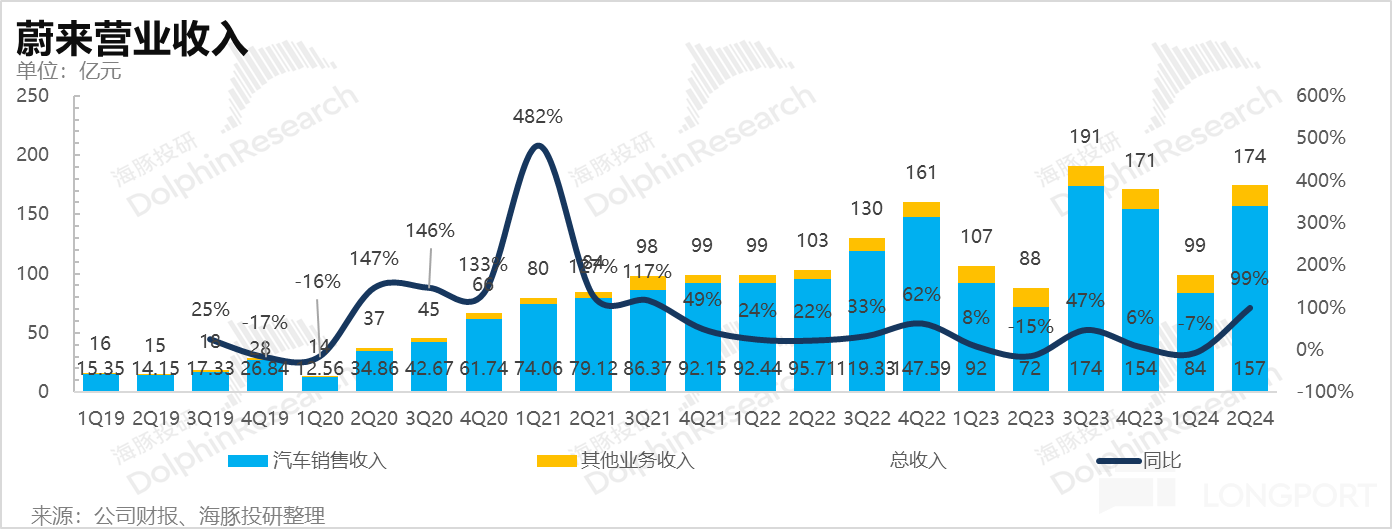

IV. NIO's Revenue Exceeds Market Expectations

NIO's overall revenue in the third quarter was 17.5 billion yuan, a 76% increase compared to the previous quarter, exceeding the market's expected 17.2 billion yuan. The main reason for the revenue exceeding expectations was the higher-than-expected car sales.

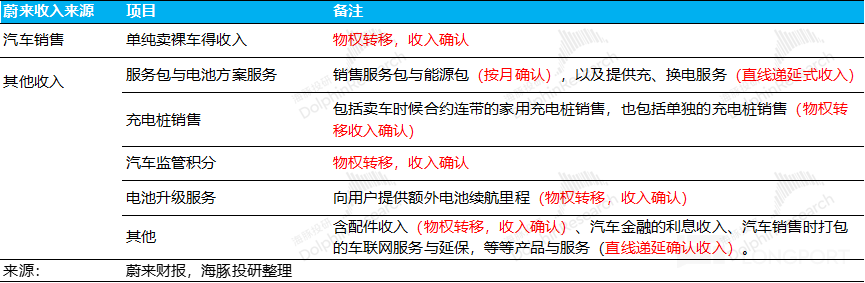

Other business revenue this quarter was 1.77 billion yuan, basically in line with the market's expected 1.79 billion yuan, an increase of 240 million yuan compared to the previous quarter mainly due to the increase in parts, accessories sales, vehicle after-sales service income, and battery swap income brought by the continuous increase in the car ownership. This increase was partially offset by the decrease in revenue from used car sales.

The overall gross profit margin this quarter was 9.7%, exceeding the market's expected 8.4%. Both the car gross profit margin and other business gross profit margin were higher than market expectations. The other business gross profit margin this quarter was -12.3%, a 6.4% increase compared to the previous quarter. The loss in other businesses continued to narrow, mainly due to higher utilization of battery swap stations (the cooperation of the "Battery Swap Alliance") and the enhanced profitability of after-sales services. Management expects that the gross profit margin of other businesses will continue to increase to nearly -10% in the next few quarters, continuing to reduce losses

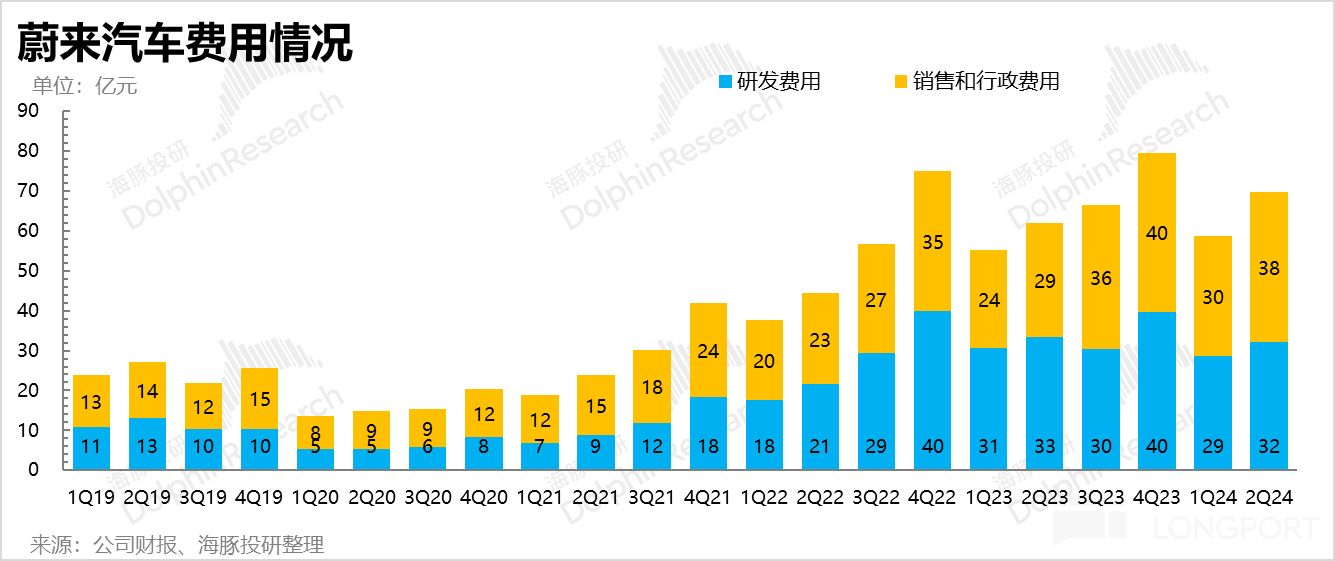

V. Continued High Investment in Operating Expenses

This quarter, operating expenses reached nearly 7 billion, an increase of 1.1 billion from the previous quarter. Even excluding the impact of SBC, operating expenses increased by nearly 900 million compared to the previous quarter, with the highest increase this quarter being in sales expenses. Specifically:

1) R&D expenses this quarter were 3.22 billion, slightly lower than the market's expectation of 3.4 billion

Nio's focus on R&D this year remains on intelligent driving and the development of new models. In terms of personnel structure, about 70% of R&D personnel are dedicated to intelligent technology-related fields. Nio's latest progress in intelligent driving includes the release of the self-developed NX9031 intelligent driving chip based on the 5nm process, with a single chip achieving the performance of four NVIDIA Orin X chips.

Regarding this year's R&D spending guidance, Nio has indicated that Non-GAAP R&D expenses per quarter are around 3 billion, which is still within the guidance for this quarter.

2) Sales and administrative expenses this quarter were 3.76 billion, exceeding the market's expectation of 3.58 billion

The higher-than-expected sales and administrative expenses may be mainly due to:

Nio continues to increase sales personnel and expand its store network. By the end of 2023, sales and market service personnel at Nio accounted for 52% of total employees, making it the company with the most sales personnel among new forces. This quarter may see further expansion of the sales team, especially the need to add stores (about 105) and sales personnel before the delivery of the LeDao in September, making it difficult to reduce sales expenses.

This quarter saw a concentration of new models for 2024 being launched, with sales expenses invested in the marketing of Nio's new models.

As for this year's sales expense guidance, Nio expects sales expenses to increase by no more than 20% year-on-year (not exceeding 15.5 billion for the whole of 2024), averaging no more than 4.4 billion per quarter for the next two quarters. This seems to indicate that it will be difficult to reduce sales expenses, and they may continue to rise.

Although the gross profit margin increased significantly this quarter, the continued high investment in operating expenses (mainly sales expenses) led to an operating loss of -5.2 billion this quarter, still in a deep loss state. The increase in operating expense ratio to -30% this quarter is mainly due to the improvement in gross profit margin and the decrease in the operating expense ratio brought about by the release of sales volume.

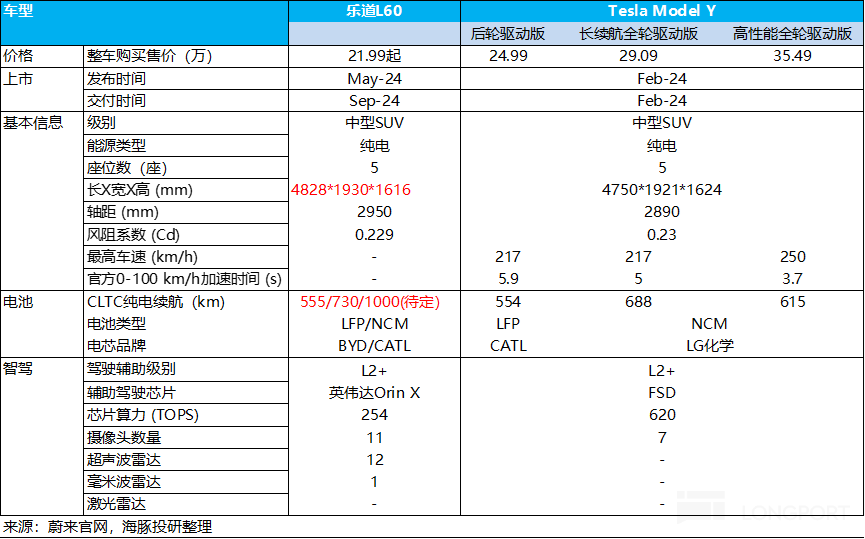

VI. Can the "L60" from Leador drive Nio's sales in 2024 beyond expectations?

This quarter, the company's cash and cash-like assets on the books amount to 42.6 billion, a decrease of 3.7 billion compared to the first quarter's 45.3 billion. The decline is mainly due to a cash consumption of 4.5 billion brought about by adjusting SBC losses this quarter.

The market's sales expectations for Nio in 2024 are around 210,000 to 220,000 vehicles. This is mainly because the sales of Nio's main brand have rebounded, stabilizing at around 20,000 vehicles. However, the market's expectations for the upcoming Leador L60 are not high, with sales expected to be only around 15,000 to 20,000 vehicles in 2024 (deliveries starting in September). This is primarily because the L60 will enter the most fiercely competitive price range of 200,000 to 300,000 pure electric vehicles, facing greater competition than Nio's main brand in the 300,000+ price range. The key to whether sales in 2024 can exceed expectations also lies in the performance of the Leador L60.

The Leador L60 will enter the mainstream household user market. The first SUV Leador L60 has a pre-sale price of 219,900 yuan and will start deliveries in September. Currently, there are about 105 stores and 1,000 swap stations ready. The main advantages of Leador in the most competitive price range are:

Spaciousness: Compared to Tesla Model Y, Leador has size advantages, with larger interior space and longer wheelbase than the Tesla Model Y.

Price advantage: The starting price of Leador L60 is 219,900 yuan, 3,000 yuan lower than the entry-level Model Y. At the same time, under the BaaS model, Leador's price is expected to drop to 150,000-160,000 yuan, forming core competitiveness. Although Nio has not yet announced the pricing of the BaaS scheme, Dolphin Jun predicts that the pricing of the BaaS scheme will have a significant impact on sales.

Energy replenishment advantage: Leador L60 supports both 900V high-voltage fast charging and battery swapping, and can use over 1,000 swap stations nationwide and over 25,000 Nio-owned charging piles. The energy replenishment experience of 900V high-voltage fast charging and battery swapping is a differentiating highlight for Leador L60 at 200,000 yuan.

Nio is relatively optimistic about the sales expectations for this vehicle, expecting monthly sales to exceed 10,000 units, and Leador's long-term gross profit margin may exceed 15%. However, for the profit and loss balance of the Leador brand, the management has indicated that monthly sales will need to reach at least 20,000 to 30,000 units, indicating that there is still a long way to go.

For more in-depth research and tracking comments on Nio by Dolphin Jun, click:

Financial Report:

On June 7, 2024, financial report interpretation "Sales return, stock price collapses, how will Nio be saved?" Read more

On June 7, 2024, minutes of the conference call "Expected return of double-digit gross profit margin in the second quarter" link

On March 15, 2024, financial report interpretation "Another burst of losses! Can Nio only rely on Middle Eastern backers to survive?" link

On March 6, 2024, minutes of the conference call "Maintaining a gross profit margin of 15%-18% for the whole year, hoping for monthly deliveries to quickly return to 20,000 vehicles" link

On December 5, 2023, financial report interpretation "Repeatedly teetering on the brink, what is Nio relying on to restore its reputation?" link

On December 6, 2023, minutes of the conference call "Continuing to increase sales network and personnel investment (Nio 3Q conference call minutes)" link

On August 29, 2023, financial report interpretation "Nio: a single quarter loss of 6 billion? Don't lose hope, the future is not too far away" link

On August 29, 2023, the minutes of the conference call "Achieving low double-digit gross margin in the third quarter, with gross margin increasing to 15% in the second quarter (Nio minutes)"

On June 9, 2023, financial report interpretation "Nio: Reflection is more important than selling cars"

On June 9, 2023, minutes of the conference call "Nio minutes: ES6 to exceed tens of thousands in July, gross margin to return to double digits in the second half of the year"

On March 2, 2023, financial report interpretation "Many ideas, poor execution, how much trust can Nio still erode?"

On March 2, 2023, minutes of the conference call "Nio: Gross margin expected to reach 18-20% by year-end, lithium prices may drop to 200,000"

On November 11, 2022, financial report interpretation "Nio: When pricing is pessimistic enough, how much impact can a collapse in answering have?"

On November 11, 2022, minutes of the conference call "Nio: Break-even in the second quarter of next year, no problem with long-term stable gross margin of 20-25%"

On September 7, 2022, financial report interpretation "Don't be scared by explosive losses, Nio is approaching better days"

On September 7, 2022, minutes of the conference call "Production capacity is the bottleneck, record-breaking sales month by month"

On June 29, 2022, hot review "This report shorting Nio could be more heartfelt"

On June 16, 2022, minutes of the new car launch "Swift release, swift delivery, Nio has hope in the second half of the year"

On June 9, 2022, interpretation of the second quarter financial report "Nio remains soft in the second quarter, can only rely on new cars for confidence?"

On June 9, 2022, second quarter financial report conference call "Gross margin in the second quarter will be worse, Nio's turnaround depends on the second half of the year"

On March 25, 2022, review of the 2021 annual report "Nio: Under pressure, is the future continuing in the dark or welcoming the dawn?"

On March 35, 2021, minutes of the 2021 annual report meeting "2022 is a year of comprehensive acceleration for Nio"

On November 10, 2021, review of the 2021 third quarter report "Nio: After the 'ankle cut', will there be a deep squat jump in the first half of next year?"

On November 10, 2021, minutes of the 2021 third quarter report meeting "Nio: No need to overly worry about temporary delivery slowdown and pressure on gross margin (meeting minutes)"

On August 12, 2021, Review of the Second Quarter of 2021 " Saying goodbye to the outbreak, what is Nio's future relying on?"

On August 15, 2021, Update on the Second Quarter of 2021 " Nio: High Valuation vs Low Deliveries, Be Careful of the "Future" in Front of You"

Research

On June 13, 2023, Hot Topic on Nio " Nio: Finally Doing Subtraction"

On December 21, 2021, Research on Nio NIO DAY " "Hot-selling model" ET5 debuts, Nio aims to reignite the "future""

In-depth

On June 9, 2021, Three Idiots Comparative Study - Part 1 " New Forces in Car Making (Part 1): Investing in the Right People, Doing the Right Things, Analyzing the People and Events of the New Forces"

On June 23, 2021, Three Idiots Comparative Study - Part 2 " New Forces in Car Making (Part 2): Market Enthusiasm Wanes, What Does Three Idiots Rely on to Consolidate Their Position?"

On June 30, 2021, Three Idiots Comparative Study - Part 3 " New Forces in Car Making (Part 3): Doubling in Fifty Days, Can Three Idiots Continue to Sprint?"

Risk Disclosure and Statement for this Article: Dolphin Research Disclaimer and General Disclosure