Employment storm "the storm is coming", is the United States really going to decline?

As the most macroscopic variable in the US stock market trading recently, the latest employment data was finally revealed last week. However, it was this number that made the market start to panic: Is the US entering a Hard landing mode? Is the rapid decline in employment due to supply side or demand side factors? Is the signal of employment structure also deteriorating?

However, from Dolphin's perspective, there is no need to be overly alarmed by the overall situation. Specifically:

I. Is US employment collapsing?

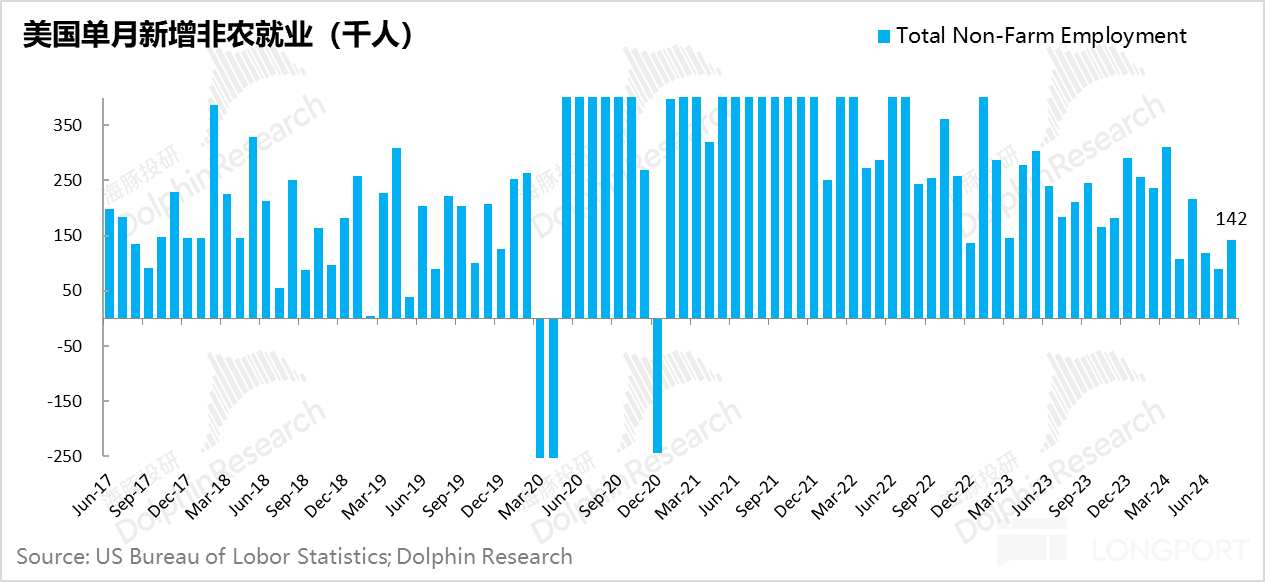

Last week, the US released two important employment data points, one being the job vacancies in July and the other being the addition of non-farm payrolls in August. These two data points together can clearly illustrate the current trend of changes in labor supply and demand.

As Dolphin mentioned before, the addition of around 150,000 non-farm payrolls per month is a reasonable monthly addition level under stable employment conditions. This is based on the average monthly addition of around 180,000 labor force (including labor force and non-labor force) in the US from 2015 to 2019. Such monthly additions mean that almost all new labor supply can find employment each month, without increasing the unemployment rate or depleting the pool of potential employees.

In terms of August alone, with 210,000 new labor force supply and 142,000 new non-farm payrolls, although there were no surprising developments, the situation was relatively balanced; and due to this balance, the unemployment rate even slightly narrowed from 4.25% to 4.22%.

However, the real issue here is that alongside the release of non-farm payrolls for August, there was a significant downward revision of the previously reported additions in June and July: the July data was revised down from the original 114,000 to 89,000, and the June data, after being revised down to 179,000 in July, was further revised to less than 120,000. Especially in July, if the additional unemployment due to abnormal weather resulted in less than 90,000 new jobs, and based on this foundation, August only recovered to slightly over 140,000, then the overall picture of non-farm employment appears much weaker.

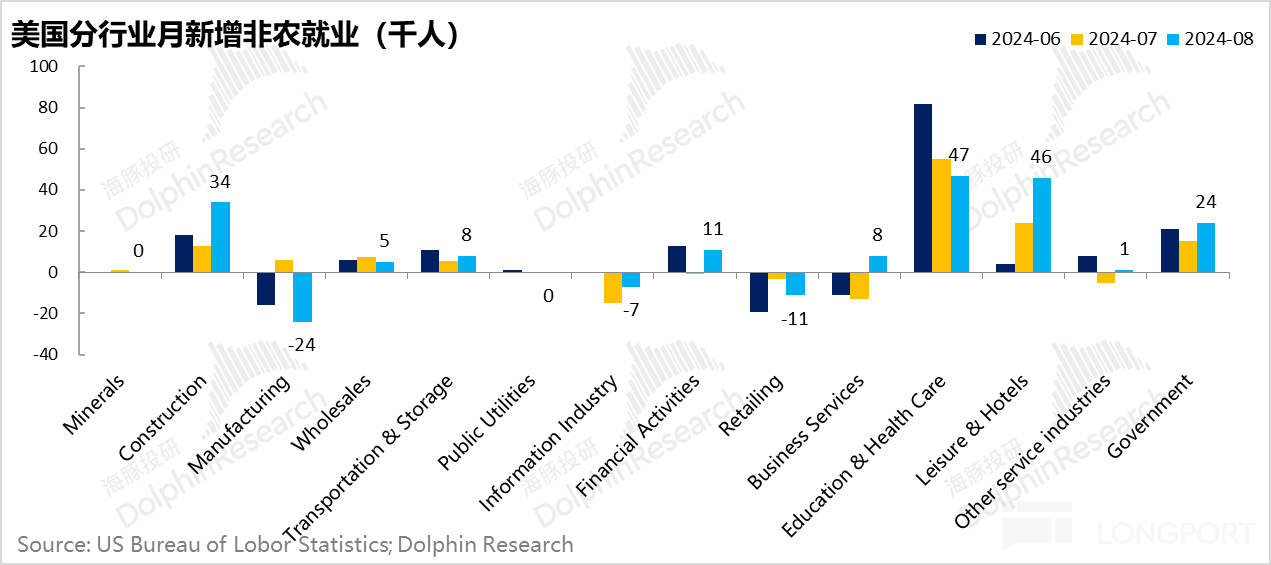

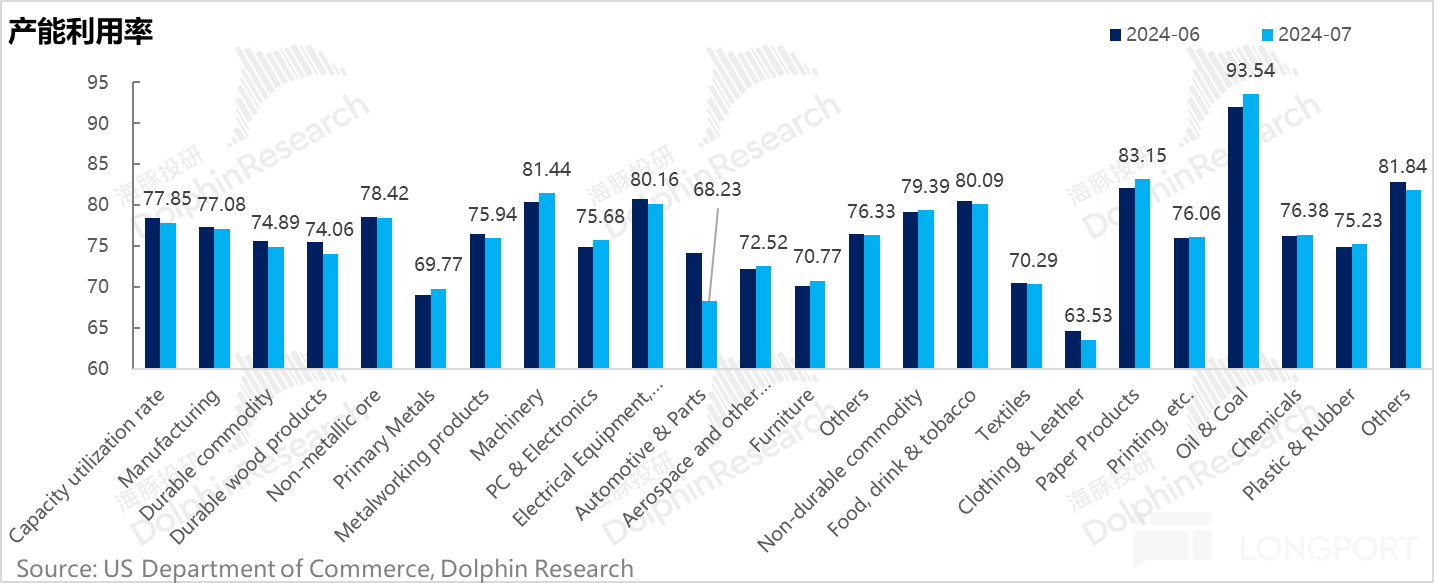

From the perspective of employment structure, the changes in the construction industry in July and August may be more weather-related, and when looked at together, they are still decent. However, the main issue lies in the manufacturing industry, where the decline in August is very apparent. Looking at the source of the decline from a detailed industry perspective, it is mainly in the transportation equipment manufacturing sector, especially in automobile and parts manufacturing. When combined with the gradual decline in automobile production capacity utilization in July (falling below 70% for the first time), the US automobile market seems to have transitioned from post-pandemic supply tightness to oversupply, and the impact of high interest rates on automobile demand has become evident.

In terms of employment in the service industry, a. The continuous net layoffs in the retail industry have to some extent shown the pressure on physical consumption; b. The information industry mainly refers to the media industry, as traditional media such as cable is performing poorly and continues to see net layoffs; c. Within the broad category of professional business services, positions represented by computer technology, scientific research, and finance and accounting are still doing well, but temporary employment services continue to see net layoffs, showing poor performance.

In the originally two industries with strong traditional employment demand: a. Medical services: Although overall employment is relatively strong, there has been some structural differentiation in specific areas, such as the employment shift from medical care to home care; b. Leisure and entertainment industry: A very peculiar situation, despite the sharp decline in the stock prices of many American catering companies, employment in the catering sector accelerated in August. However, recent employment data has been continuously revised downwards, so it is necessary to consider whether the August data will also be revised downwards in advance.

Overall, if we look at the data for the three months after adjustment together, with an average of less than 120,000 new non-farm jobs per month and a recent labor force supply of 200,000 per month, the labor market does seem to be leaning towards oversupply.

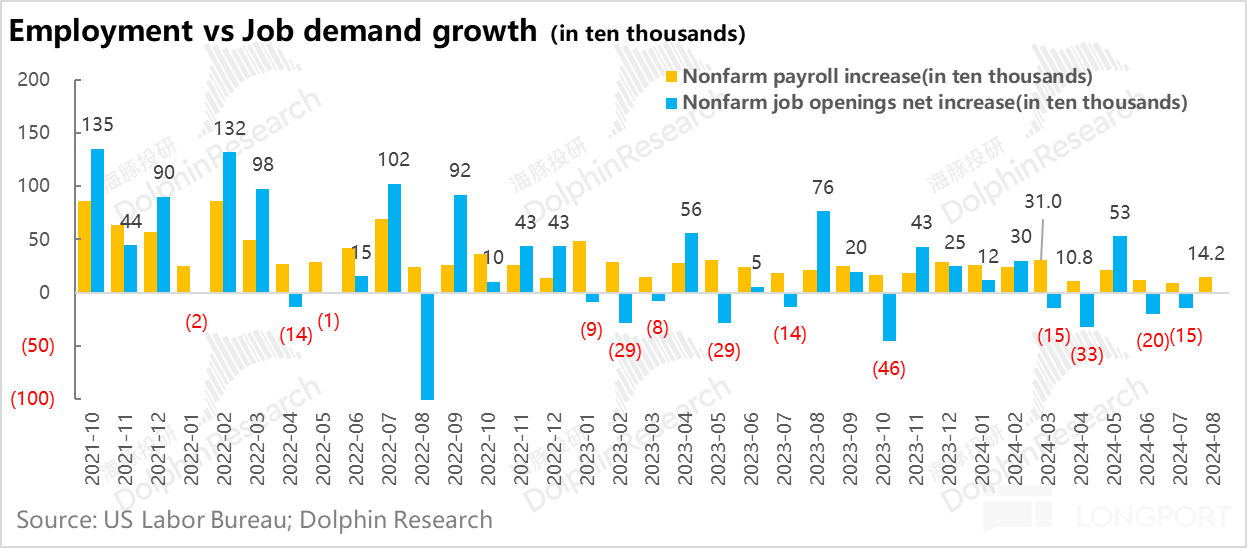

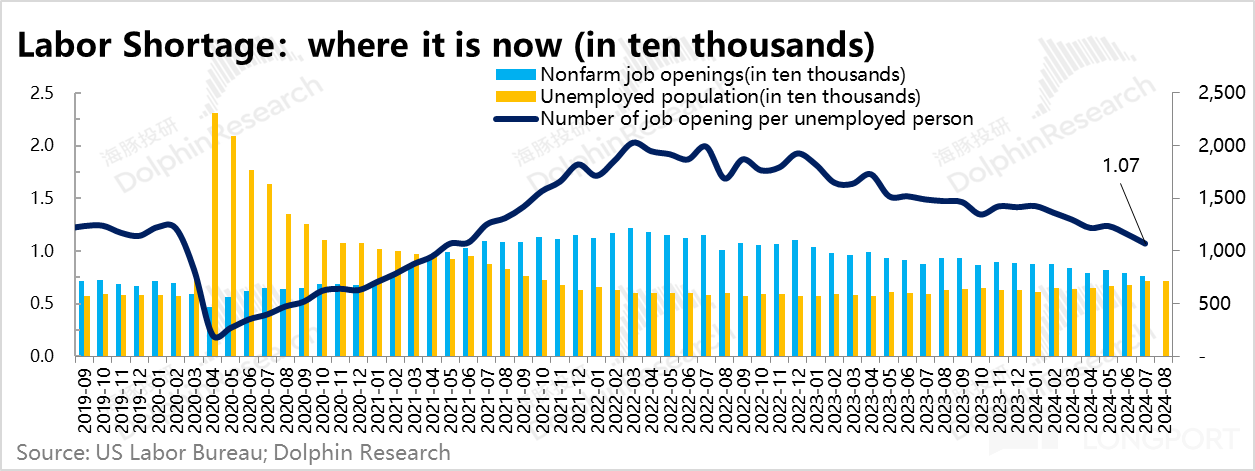

Of course, in addition to the actual increase in employment, another truly important factor is whether the demand for hiring by companies is really shrinking. Unfortunately, the number of job vacancies in July did not provide much comfort to the market. Even from the perspective of the Federal Reserve, this number may be the real cause for concern.

In July, there were 7.67 million job vacancies, and considering the newly added jobs in that month, following a decrease of 200,000 job vacancies in June, companies reduced their demand for positions by 150,000 in July.

When these numbers from the supply and demand sides are put together, on one hand, the labor force supply continues to steadily increase, while on the other hand, companies' recruitment demand is decreasing. If these two trends continue, the labor market will inevitably shift from undersupply to oversupply.

Of course, in the past, there have been instances where companies' job demands decreased for several months and then saw a significant increase. The Federal Reserve was not concerned at that time. However, the basic premise for not being concerned was: at that time, there were still significantly more job vacancies in the labor market waiting to be filled than there were people actively seeking employment. But by July, with 7.67 million job vacancies vs. 7.16 million people seeking employment, the ratio was already 1:1.

If the demand for job positions from companies in the market further declines, it is likely that there will be more people seeking employment than there are job vacancies to be filled, leading to a reversal in supply and demand. This could weaken residents' employment expectations, drive down consumption expectations, and make residents reluctant to further reduce savings and consumption, which could then lead to a relatively rapid economic downturn.

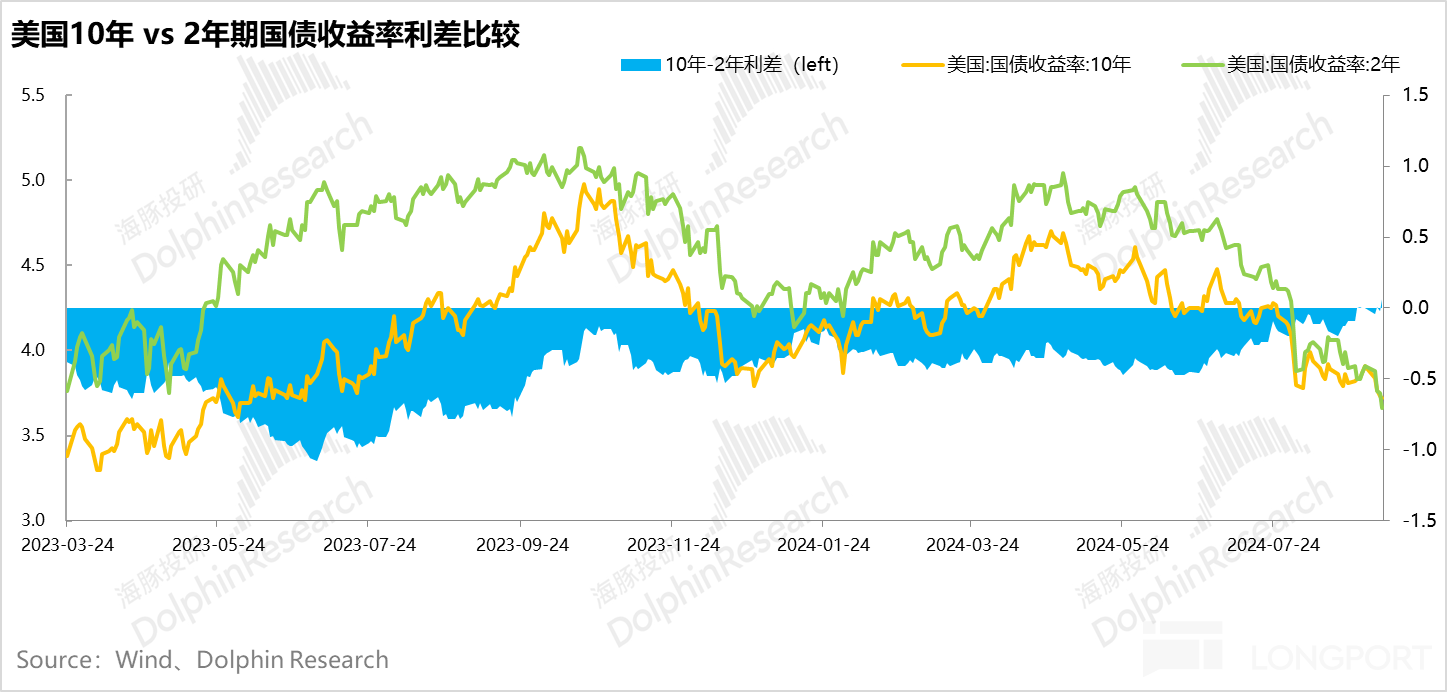

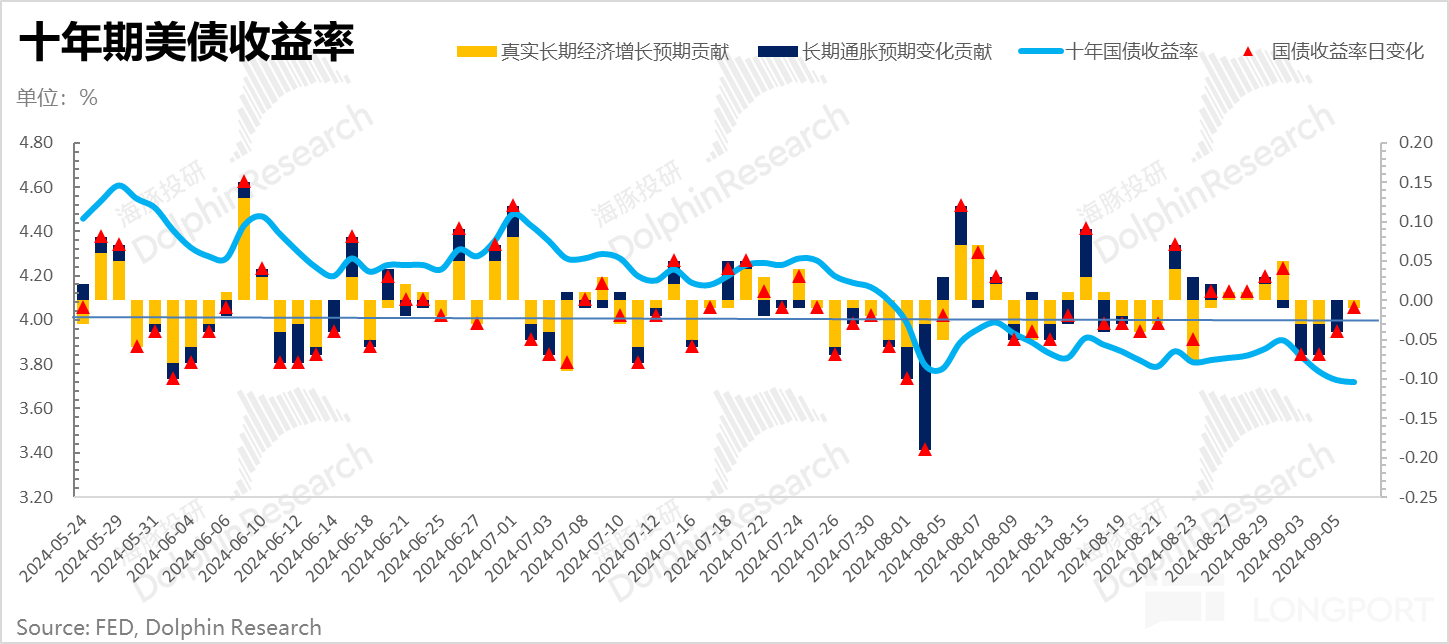

And this is also the reason why the market is beginning to worry about the possibility of a US economic recession. At present, the yield on the 10-year US Treasury bond has fallen to below 3.7%, with the 2-year Treasury bond yield, which is more sensitive to short-term interest rate expectations, experiencing a greater decline. It seems that the market has already started to price in a recession.

In the context of the shift in labor supply and demand, it is estimated that the Federal Reserve will quickly and significantly shift the balance between employment and inflation towards stabilizing employment. Especially from the perspective of the policy choices of various countries at present, deflation is a more terrifying prospect than inflation.

At the same time, considering that in this cycle, household balance sheets are very healthy, although current consumption is weakening, it is not as slow as imagined, and the government is also leveraging up. Taken together, the likelihood of a larger interest rate cut this year has indeed significantly increased, but it may not necessarily be an immediate 50 basis point cut in September. Moreover, as long as the three major employment sectors are overall secure, there is no need to panic over short-term changes in high-frequency data.

II. Chinese Assets: Balancing Expectations of Interest Rate Cuts and External Recession

Currently, in terms of the underlying drivers of the domestic economy, one is the leveraged growth of domestic demand (government, enterprises, residents), which is essentially debt-driven, and the other is relying on external demand for export earnings. With domestic demand continuously deleveraging and no positive changes in the domestic fundamentals, we can only look at the marginal changes in external factors. In other words, without strong government leverage, China's ability to self-rescue its assets is weak. Although valuations are currently cheap, being cheap alone is not enough; there needs to be marginal improvement. This marginal change lies in the expected changes in the external market. If it is a soft landing, external demand can remain stable, and a rate cut can boost valuations, which is a good thing. However, if the external market also experiences a recession and external demand falters.

Correspondingly, if the path of the external market is a soft landing, it means that external demand can basically remain stable, and a rate cut can also alleviate valuation pressures, which is a relatively positive situation. But if there is an expectation of an external market recession, then the EPS of Chinese assets on the numerator side may face further pressure, with expectations of further deterioration in EPS. Trying to improve valuations through a rate cut when EPS is hopeless based on Beta alone, one can only look for companies with super-powered Alpha.

III. Portfolio Rebalancing and Returns

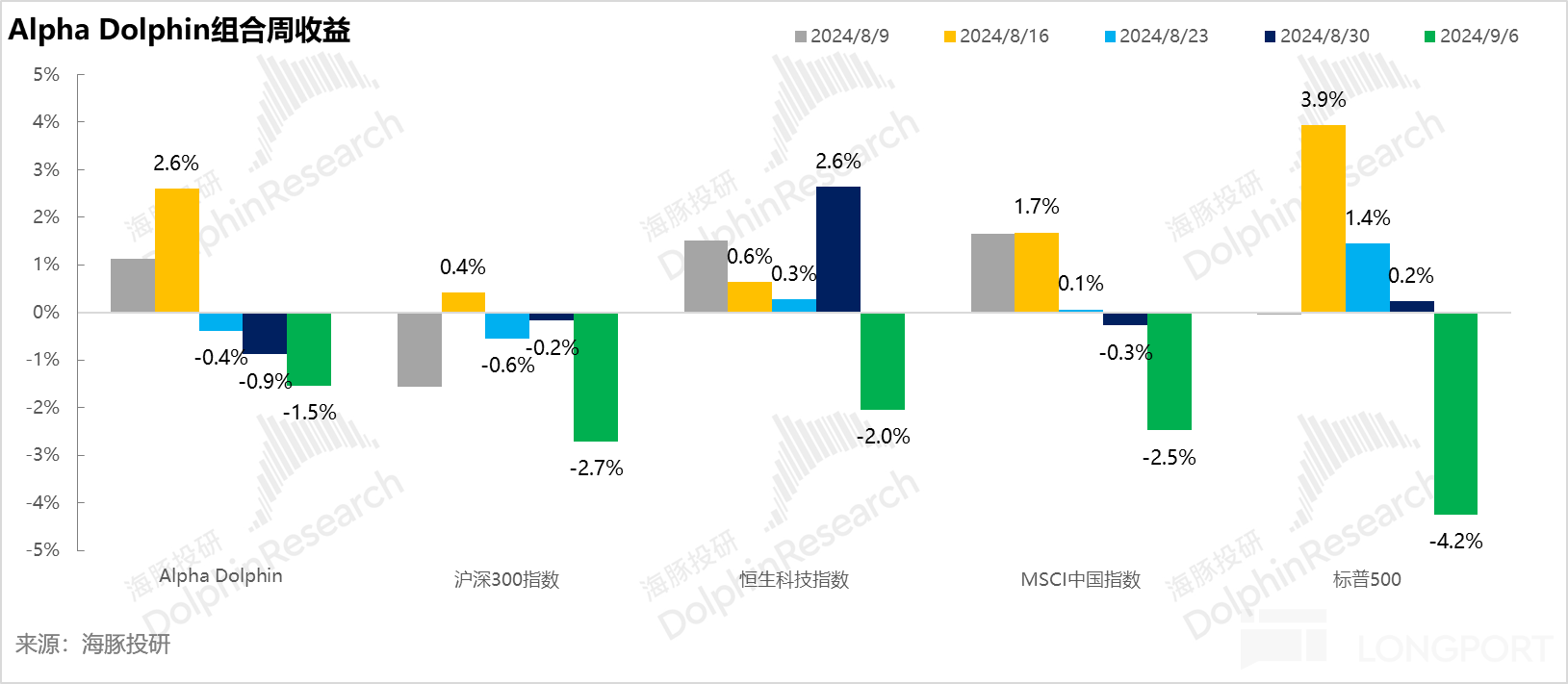

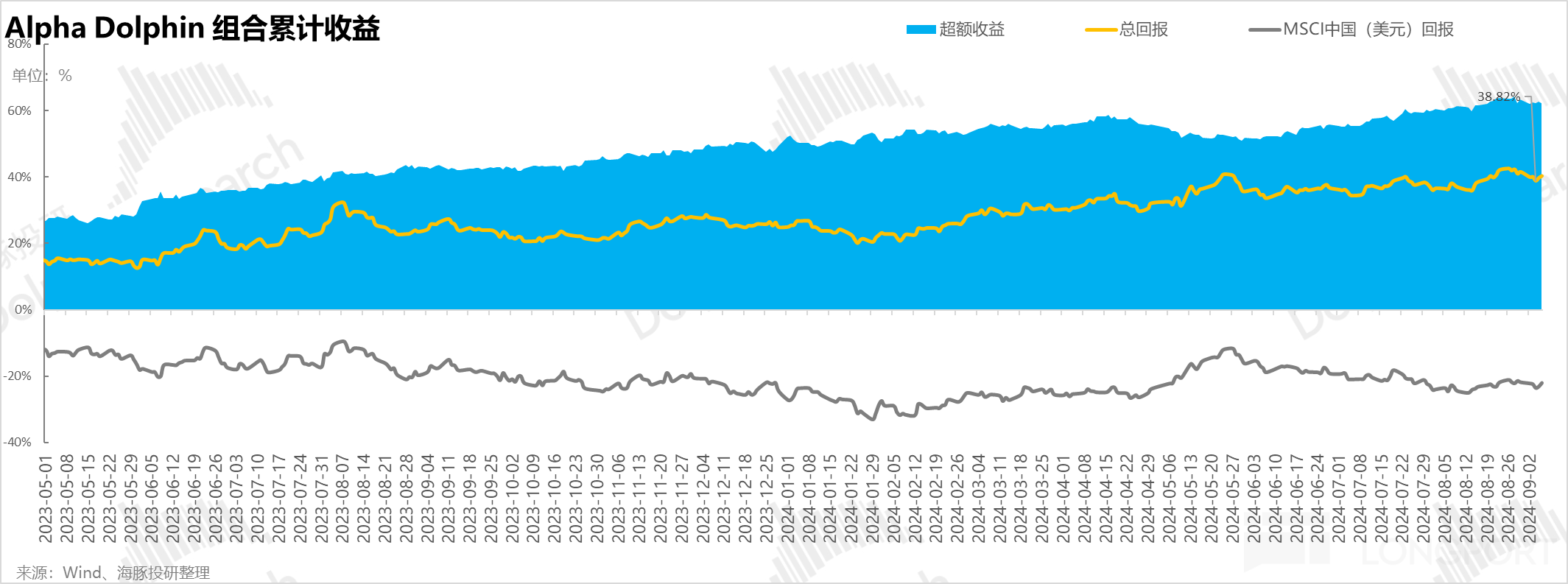

There was no rebalancing in the portfolio last week, and the portfolio return decreased by 1.5%, outperforming Chinese asset indices - MSCI China (-2.5%), Hang Seng Tech Index (-2%), Shanghai and Shenzhen 300 Index (-2.7%), and S&P 500 (-4.2%). This was mainly because the returns from holding US bonds in the Alpha Dolphin portfolio offset the impact of the stock market decline, with the weekly decline in equity assets at 3.5%

Since the start of the test until last weekend, the absolute return of the portfolio is 38%, with an excess return compared to MSCI China of 62%. From the perspective of asset net value, Dolphin Jun initially had virtual assets of USD 100 million, which has now fallen to USD 140 million.

IV. Individual Stock Profit and Loss Contribution

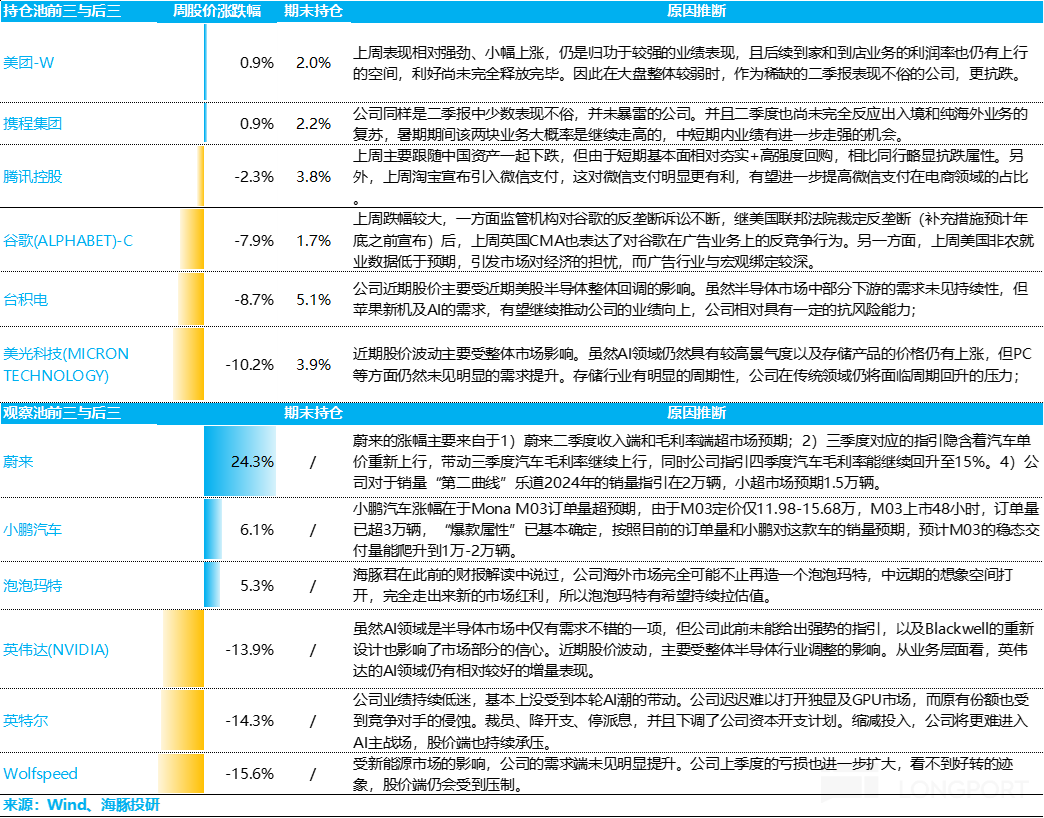

Last week, the main drop was concentrated in US stocks, especially in AI stocks such as TSMC and Micron. Currently, it seems difficult for the leading company NVIDIA to further deliver better-than-expected performance. With major tech giants actively investing in AI, there are concerns that the current linear extrapolation of valuations may face a pullback risk. Moreover, as the market begins to trade, the risk of growth stocks like AI is increasing as the US economy may be on the edge of recession.

Compared to the overall valuation slaughter of US assets, Chinese concept stocks can only be said to have a smaller decline when valuations are cheap enough. Companies like Nio occasionally have performance results that are not as pessimistic as the current stock price suggests, giving hope for a strong rebound.

V. Portfolio Asset Allocation

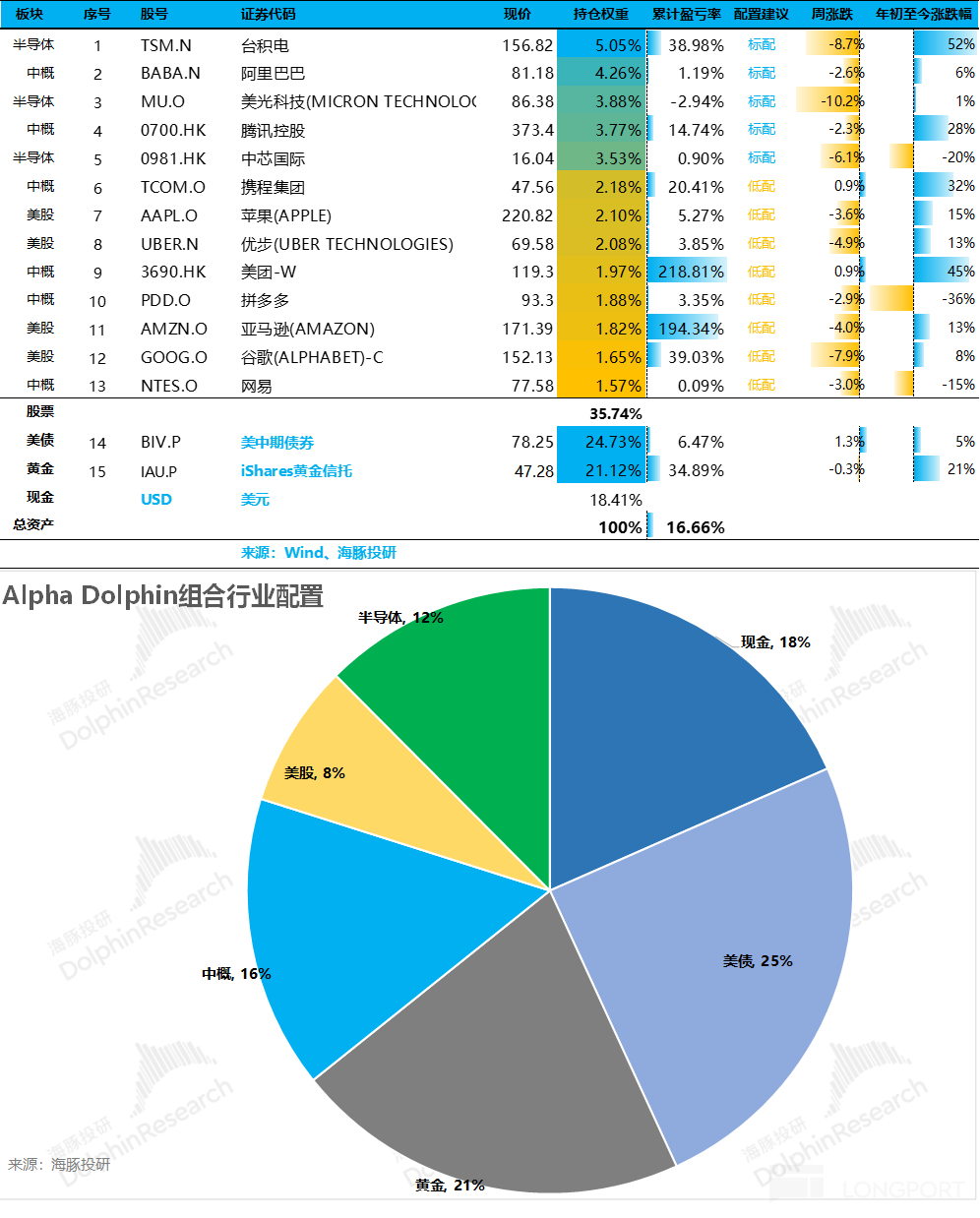

The Alpha Dolphin virtual portfolio holds a total of 13 individual stocks and equity ETFs, with 5 core holdings and 8 equity assets being underweighted. The rest is distributed in gold, US bonds, and US dollar cash. Currently, there is still a significant amount of cash and cash-like assets, which will gradually increase based on performance after the end of the financial reporting season. As of last weekend, the asset allocation and equity asset weighting of Alpha Dolphin are as follows:

Risk Disclosure and Statement of this Article: Dolphin Research Disclaimer and General Disclosure

For recent weekly reports from Dolphin Research, please refer to:

《"After the Slaughter, Is There Still Hope for Chinese Concept Stocks?》

《US Stocks: Scared, then playing music?》

《US Stocks keep exploding with "ghost stories", is there no bottom line for the decline?》

《Are the "brilliant" small-cap stocks in the US nourished by economic fundamentals?》

《US Stock Soft Landing = Giant Hard Control + Small Retail Investors Scattered?》

《The American consumption locomotive is leaking, can it still achieve a soft landing in trading?》

《Deflated social zero, soft landing economy, will it drag down Chinese assets?》

《The U.S. fiscal spending is "not guarding the door", be cautious about trading interest rate cuts》

《U.S. stock market interest rate cut expectations kill "backstabbing", is it reliable this time?》

《Hong Kong stocks suddenly change face, to escape or to accept?》

《Simultaneous correction of US concept stocks, who is the opportunity?》

《America in 2024, not a soft landing or no landing》

《Can earn more and spend more, why do American residents consume so fiercely》

《Hoping for a major correction in US stocks to get on board? Not very hopeful》

《Low inflation in the United States is not receding, can Chinese concepts still rise?》《Not daring to chase after the rise of the seven tech sisters? Chinese concept stocks unexpectedly benefited》

《Enterprises relay to support the economy, the United States will not cut interest rates quickly》

《In 2024, will the U.S. economy avoid a hard landing?》

《At another critical moment! Will Powell bail out the spendthrift Yellen?》

《Seeing mud and sand again, how much faith can withstand the test?》

《Unstoppable Deficits, Supporting the Dignity of the US Stock Market》

《2024 United States: Good Economy, Quick Rate Cuts? Too Beautiful, Will Suffer Losses》

《2023 United States: Suicide-style Rebirth》

《High Interest Does Not Extinguish Consumption, Is America Really Strong or Just Hype?》

《Second Half of Tightening by the Federal Reserve, Neither Stocks nor Bonds Can Escape!》