Pinduoduo's idol - Costco is the "ideal type" of retail?

Looking at the overall retail industry in China, Pinduoduo in e-commerce and Pangdaon in physical retail are generally regarded as benchmarks in their respective segmented markets, even considered the "optimal solution" for their business models. The most commonly shared and highly praised feature between these two is their focus on consumer interests first, and extreme operations (the former focusing on efficiency, while the latter emphasizes quality), which more or less "inherits" from another overseas retail benchmark - Costco.

This time, Dolphin Research will review, explore, and learn together with everyone about this long-standing retail benchmark, examining where its core strengths and scarcity lie, and what specific business models and operational differences with competitors have created this differentiated advantage:

1. Reviewing the past stock price performance, since the early 2000s, Costco's market value has increased by about 19 times, with an annualized growth rate of about 12.8%, significantly higher than the S&P 500's annualized growth of 5.4% over the same period. However, compared to stocks that easily increase by hundreds of times, Costco's growth rate is not the strongest.

But in terms of annual growth rate, Costco has only experienced 4 annual declines during extreme events such as the dot-com bubble, the 2008 financial crisis, and the "historic" COVID-19 pandemic in 2020, with all other years showing an increase. Its extremely low retracement and nearly 100% increase except for stock market crashes, are the true rarity.

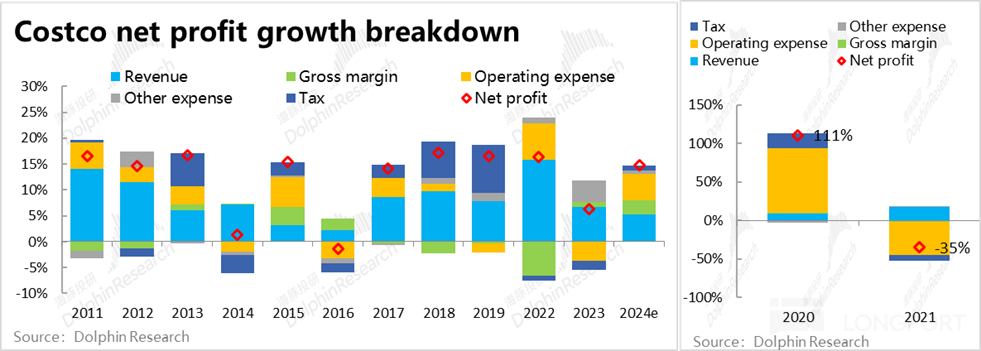

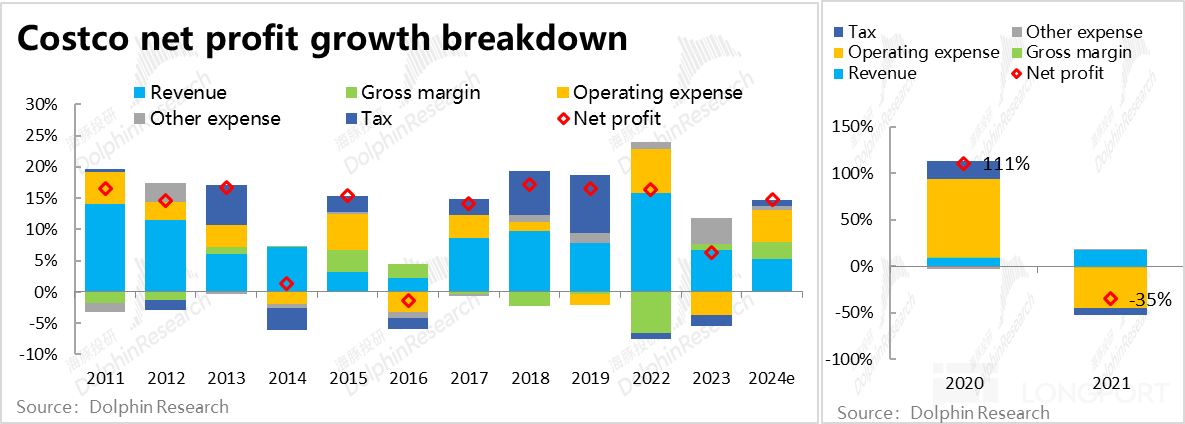

2. Analyzing the factors driving stable market value growth after splitting, most of the time Costco's PE ratio fluctuates in the range of 20x to 30x, indicating that valuation is not the main contributor. The increase in market value is mainly attributed to the "accumulation of net profit growth never below 10% annually." Among them, revenue growth (blue), decrease in expense ratio (yellow), and the reduction in taxes and fees over several years (dark blue) are the main factors in decreasing order of importance for profit growth.

Therefore, the secret behind Costco can be summarized in two points:

① What reasons have allowed Costco to achieve steady revenue growth for over 20 years, almost ignoring the fluctuations in the macroeconomy, consumer sentiment, and changes in consumer habits and channels?

② What reasons have enabled Costco to continuously improve operational efficiency and reduce cost ratios over more than 20 years? With the gross profit margin basically unchanged, how has the company's profit margin continued to increase in small steps?

As the first article on Costco research, we will focus on the first point mentioned above, attempting to answer how Costco has achieved continuous stable income growth over decades, which is the key reason that has allowed Costco to stand out

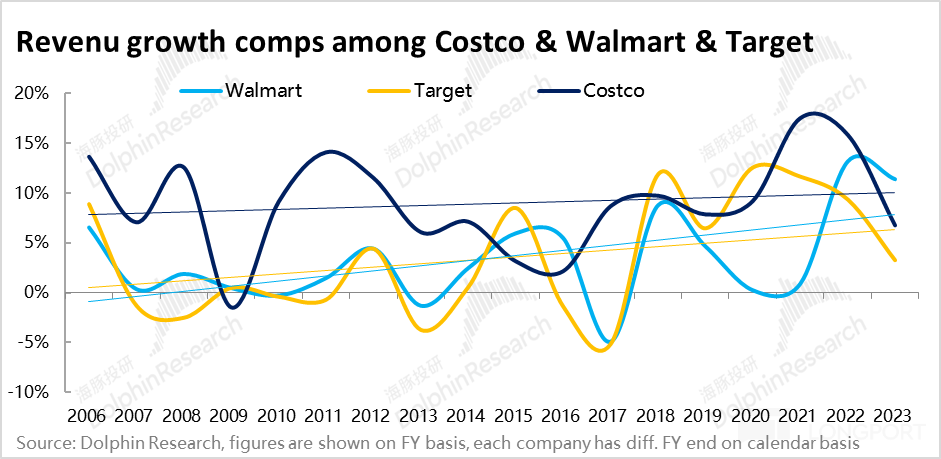

1 Over the past nearly 20 years from 2005 to 2023, Costco's compound revenue growth rate was 8.8%, far exceeding Walmart and Target's mere 3.3% growth rate during the same period. In the fully mature offline retail industry, Costco has relatively higher growth potential.

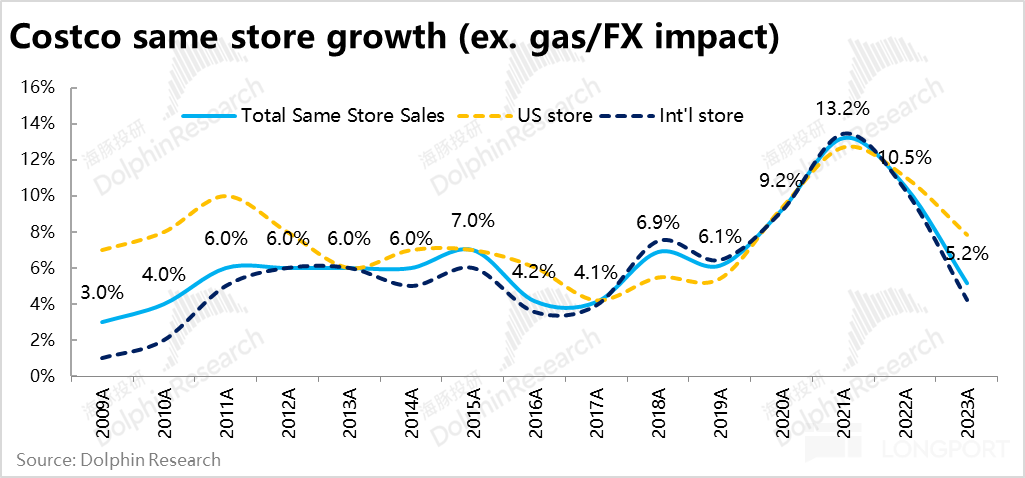

2. Except for a few cases, the number of new stores opened by Costco each year has remained between 15 to 30 for over 20 years, indicating that Costco's growth is not simply driven by opening new stores. Excluding uncontrollable factors such as new store openings, exchange rates, and fluctuations in gasoline prices, Costco's same-store comparable compound growth rate from 2009 to 2023 was 6%, higher than its peers. Even in 2009 (during the financial crisis), comparable store sales still grew by 3%, demonstrating strong resilience against macroeconomic cycles.

3. What exactly enables Costco to have such loyal customers, stable foot traffic, and sales? Under the framework of "saving, variety, quality, and speed", the most important aspect of "saving" is that Costco adopts a "hard discount" model that offers consumers the greatest benefits. In simple terms, it does not rely on low-quality (low-cost white label) or flawed (brand discount) products for low prices. Instead, while ensuring product quality, the retailer compresses its own profit margin space, directly benefiting consumers.

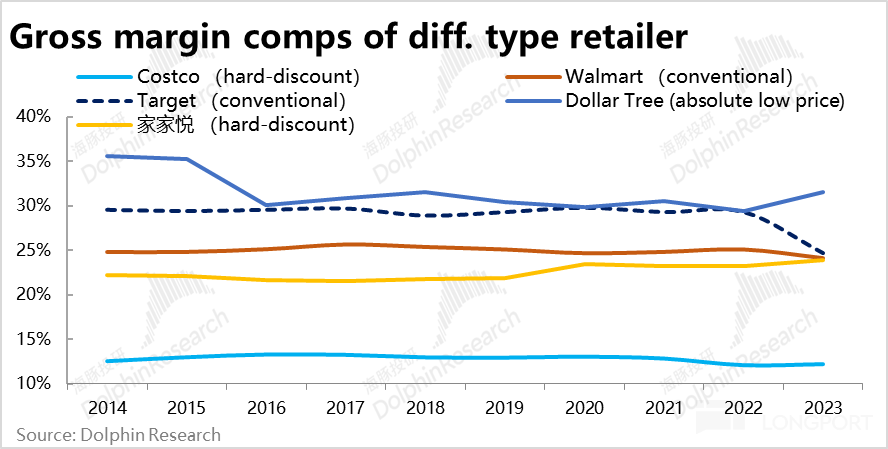

As a validation, Costco's gross margin has consistently remained low at 12% to 13% for over a decade, with no signs of increase. This is significantly lower than the 25% to 35% gross margin of both conventional supermarkets like Walmart and Target, and absolute low-price retailers like Dollar Tree. This clearly reflects Costco's deliberate choice to maintain a low gross margin.

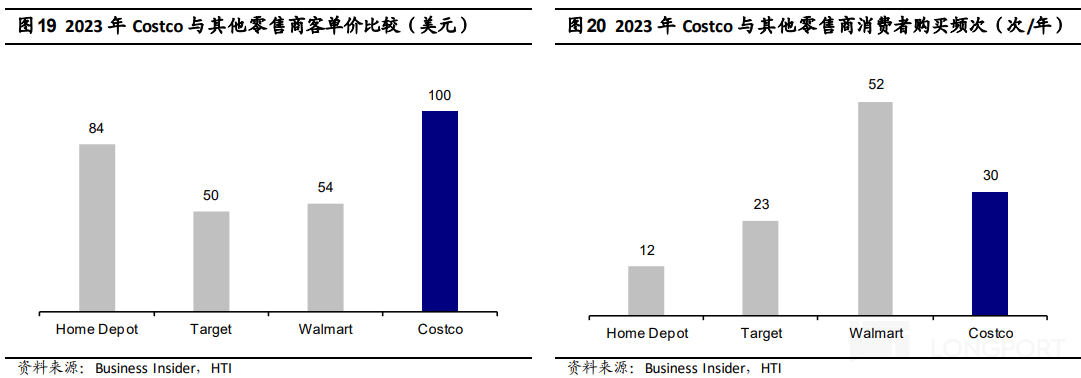

4. While Costco prices relatively lower than its competitors, its products are generally synonymous with "quality". Balancing "saving" and "quality" is one of the winning reasons why the company can attract and retain loyal and stable foot traffic. Despite being known for discounts, Costco's actual positioning is towards the middle-class consumers. As evidence, the average single shopping amount for Costco consumers is over $100, double the average order value of around $50 for competitors like Walmart and Target.

Costco actively selects and targets the relatively small and clearly defined user group of the middle class, allowing the company to benefit from the middle class's stronger purchasing power (affording quality products) and theoretically lower volatility in daily consumption expenditure, which is also one of the reasons why Costco is more resistant to economic cycles.

5. From the perspective of "variety" - the richness of products/services, Costco's approach involves a combination of "addition and subtraction".

In terms of the total number of product SKUs, Costco's approach is "less" (but refined). Costco generally has around 4000 SKUs, much lower than the around 20,000 SKUs in conventional large supermarkets Moreover, in terms of the structure of product categories, only 3/4 of Costco's SKUs are allocated to high-frequency and essential items such as food and daily necessities. Only 1/4 is allocated to low-frequency and optional items such as clothing, home furnishings, and electronics.

By offering a carefully selected and limited range of products, Costco reduces consumers' decision-making costs (preventing decision fatigue), while also lowering the difficulty in managing product selection and supply chain operations (we will discuss this further in the next part from a cost and efficiency perspective).

In terms of product categories, 3/4 of the products are concentrated on daily items with high demand elasticity and high-frequency purchases, bringing stable and high-frequency foot traffic, which is also an important reason for relatively stable revenue. Additionally, categories such as food (fresh and frozen) are naturally not well-suited for online sales, which is one of the reasons why Costco is not heavily impacted by online retail.

6. "Addition" for Costco involves expanding higher-priced and higher-profit-margin optional products and services, which not only provide more comprehensive services to better engage consumers but also contribute to higher sales and profits. For example, ① high-frequency services like gas stations and affordable dining options help increase consumer stickiness; ② relatively low-frequency, optional, but higher-profit-margin services such as pharmacies, optical and hearing tests, car maintenance, as well as broader services like travel bookings, insurance, and credit cards. Leveraging the large foot traffic brought by Costco's core business with almost zero incremental customer acquisition costs, even though these businesses are not Costco's core strengths, they can still help increase the company's profits due to low incremental costs and higher profit margins.

7. In summary, unlike typical companies, Costco has made many sacrifices. They do not pursue rapid growth but instead conservatively expand stores to ensure the success of new stores and stable same-store sales growth; they do not pursue high profit margins but actively maintain low gross margins to benefit consumers; they do not pursue unlimited user expansion but instead actively limit and target user groups, facilitating the matching of supply and demand between users and the company; they do not pursue a wide range of products but instead actively streamline and focus on high-quality essential products, almost ignoring economic and technological cycles to ensure demand stability. Undeniably, these factors indeed limit the company's growth, with profits rarely exceeding 20% growth rate, and the scale can never become the industry leader. This trade-off results in moderate growth but extreme stability. These decisions are worth contemplating.

In the next part, we will focus more on the company's operations, management, and efficiency, to see how Costco, with so many "self-imposed limitations" and the industry's lowest gross margin, can still achieve decent profits that continue to slightly increase.

The following is the main content analysis:

I. What makes Costco remarkable? Slow and steady wins the race

1. Not aiming for high growth, but for stability

As mentioned in the introduction, one question we want to answer is, from an investor's perspective, what makes Costco a good company? From the ultimate judgment criterion - market value growth, reviewing Costco's past performance, we can generally find that:

① Impressive but not astonishing growth: Since the year 2000, Costco's market value has increased nearly 19 times (with an annualized growth rate of about 12.8%), significantly outperforming the S&P 500 index, which has grown by about 2.7 times during the same period. However, compared to Nvidia, which has surged over 1000 times during the same period (even excluding the recent AI-driven surge, Nvidia's cumulative growth from 2000 to 2022 is still over 100 times), it is evident that while Costco's growth is considerable, it has not reached the extraordinary level. (In terms of stock price growth rankings from high to low since 2000, Costco ranks around 250th)

② Strength lies in certainty: Since the new millennium, Costco has only experienced four annual declines in its stock price, which occurred during the bursting of the dot-com bubble from 2000 to 2002, the global financial crisis in 2008, and the outbreak of the COVID-19 pandemic in early 2020. In other words, Costco has only had 4 years of annual declines, with a significant portion of the reasons being the impact of "historic-level" market crashes. Excluding extreme "stock disaster" cases, from an annual candlestick perspective, Costco can be said to have a 100% success rate, never incurring losses.

Combining the above two points, from the perspective of market value growth, Costco's annualized growth rate is impressive but not astonishing. The true rarity lies more in its ability to consistently outperform the market, experience very few pullbacks, and provide a high-quality holding experience with extremely high certainty.

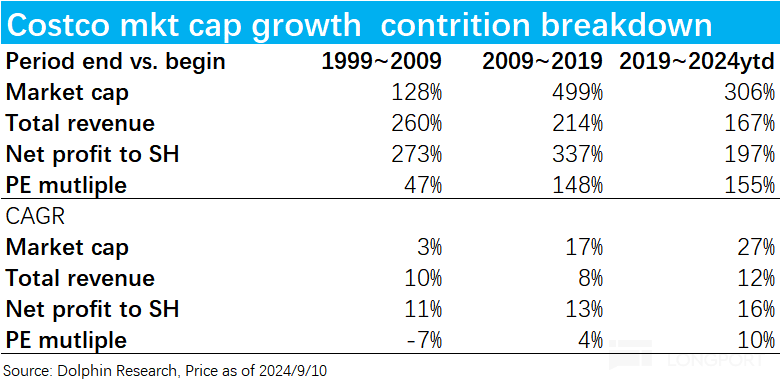

Breaking down the factors that have driven Costco's market value growth of nearly 17 times in the past 25 years, we can see the following trends in each 10-year interval:

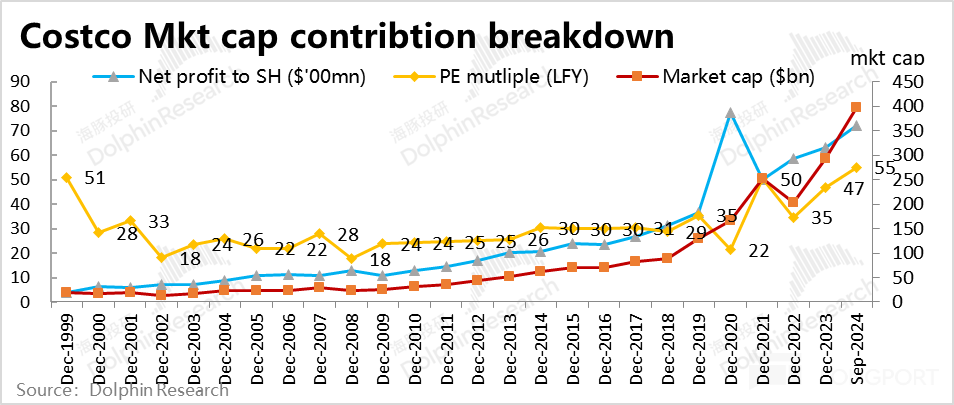

① From the end of 1999 to the end of 2009, Costco's market value remained almost flat, with a cumulative growth of nearly 28% over the decade and an annualized growth of only 3%. This was mainly due to the drag of valuation bubbles bursting and significant pullbacks. In 1999, Costco's PE valuation reached as high as 50 times, while by the end of 2009, it was 24 times, a 52% contraction in valuation (annualized -7%). However, the annualized growth rates of revenue and net profit were 10% and 11% respectively, indicating decent performance growth.

② From 2009 to 2019, over the decade, the market value increased nearly 4 times, primarily being driven by performance (revenue and profit grew at annualized rates of 8% and 13% respectively), with valuation increasing moderately (from 24 times to 35 times, a 4% annualized increase).

③ From 2019 to the present, driven by the largest quantitative easing in U.S. history, Costco's market value has rapidly surged under the resonance of both valuation and performance growth. Of the 27% annualized market value growth in the past five years, around 10% annualized growth came from the rise in valuation (Costco's PE valuation has now exceeded 50 times again), but the more significant driver is the increase in profit growth to 16% annually. The improvement in profit growth has to some extent provided support for the noticeable increase in valuation

From the above text, it can be seen that for most of the past 25 years, Costco's market value growth has been driven almost entirely by profit growth, except for the significant impact of valuation multiples expansion at the beginning and end stages. Most of the time, Costco's PE multiples have fluctuated in the range of 20+x to 30x.

Interestingly, both at the end of 1999 and currently, Costco's PE valuation has been above 50x, which inevitably raises questions about whether Costco's valuation (or bubble level) in the current U.S. stock market has reached the level of the dot-com era, and whether history will repeat itself in the future.

2. Revenue growth as the cornerstone, efficiency improvement, cost reduction, and value-added services

As seen from the above text, Costco's market value growth, except during special stages such as stock market bubbles accumulation and burst, has mostly accumulated from "steady and continuous" profit growth. So, what are the main factors driving Costco's annualized 13.4% net profit growth from 2010 to the present?

By deconstructing, it can be clearly seen that Costco's profit growth over the past decade is mainly driven by revenue growth (blue), decrease in expense ratio (yellow), and reduction in taxes and fees in certain years (dark blue), with the importance decreasing in that order. Gross profit margin (green) has not made a sustained positive contribution. (The performance fluctuation in 2020 and 2021 due to the pandemic has been too significant, not reflecting the long-term trend).

Through the above breakdown, we can clearly see that the secret behind Costco's nearly uninterrupted performance growth and stock price returns over the past few decades can be summarized in two simple points:

① What reasons have enabled Costco to almost ignore the fluctuations in macroeconomics, consumer sentiment, and changes in consumer habits and channels for over 20 years, continuously achieving steady revenue growth?

② What reasons have allowed Costco to continuously improve operational efficiency, reduce cost ratios, and incrementally increase profit margins over such a long span of over 20 years, while the gross profit margin remains relatively stable?

II. Where does the consumer preference across cycles come from

Based on the identified analysis direction, let's first look at the reasons why revenue can continue to grow. From 2005 to 2023, Costco's compound annual revenue growth rate was 8.8% over nearly 20 years, which, although not a high growth rate when viewed from an absolute angle, does not indicate very high growth However, comparing Walmart and Target (Costco's two biggest competitors) with a compound growth rate of only 3.3% during the same period, it is clear that Costco actually has a relatively high growth rate in the mature retail industry, where overall growth is very limited.

Moreover, compared to the downturns in growth experienced by Walmart and Target at various times, Costco only had a revenue decline during the 08-09 financial crisis, the only time in nearly 20 years, indicating its lower growth volatility and stronger ability to withstand macroeconomic cycles.

1. "Conservative" store opening pace & single-store growth across cycles

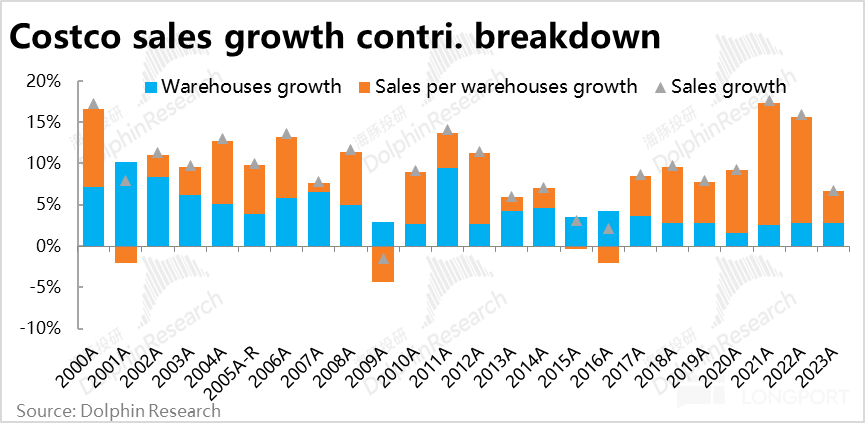

Breaking down Costco's revenue growth drivers, from 2000 to the present, the contribution of average single-store sales growth and store count growth to driving factors is almost equal, with both having a compound annual growth rate of 4.5% between 2000 and 23. Moreover, since 2017, the contribution of single-store sales to growth has become significantly higher than that of new stores. Therefore, Costco's stable growth is not solely achieved by opening new stores, but rather by sustained growth in single-store sales.

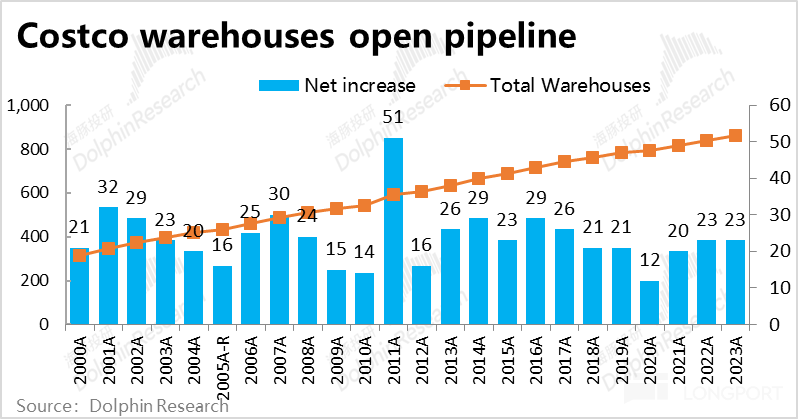

Furthermore, Costco's total number of stores (referred to as warehouses by Costco) has grown from 313 in the early millennium to over 860 stores currently, with Costco opening roughly 15-30 new stores each year for over 20 years, excluding a few outliers.

In contrast to the development path of internet or "internet-famous retail" - "rapidly opening stores to seize the market (even at an early loss), and then focusing on reducing costs and increasing efficiency to release profits after achieving a leading position or economies of scale", Costco has adhered to a very steady expansion strategy. Even though its revenue and store count are now several times higher than in the early millennium, its pace of opening new stores has not accelerated at all, and can even be described as "overly conservative".

From a subjective experience perspective, the strategy of rapid expansion to seize the market first has the probability of quickly becoming a leader in a certain industry within a few years, followed by fine-tuning operations, releasing profits, and maintaining market share. However, as the saying goes, "easy come, easy go", companies or brands that grow rapidly may quickly return to obscurity as consumer preferences or other external factors change In contrast, Costco, which has been adhering to slow expansion, has maintained its industry-leading position and above-average growth for decades. Although the former may not necessarily be the cause of the latter, it is obviously worth investors' consideration that "slow and steady wins the race." In the following text, we will further explore the management choices and objective constraints behind Costco's steady store openings.

Moreover, Costco's continuous and stable growth in same-store sales is even more rare and precious. Costco's average compound growth rate in same-store sales over the past nearly 25 years is 4.5%. Excluding the drag of new store openings on same-store sales, as well as uncontrollable factors such as exchange rates and fluctuations in gasoline prices, Costco's actual comparable same-store compound growth rate reached 6% from 2009 to 2023, and even during the financial crisis in 2009, comparable same-store sales still increased by 3% year-on-year. In other words, Costco's continuous and stable growth in same-store sales, almost never "dropping the ball," is a key reason why its performance can transcend economic and consumption cycles.

2. What is true affordability? Soft discounts vs. Hard discounts

So, what has Costco done right to have the ability to achieve stable growth across cycles? Following the classic framework of "save, more, fast, good" in the retail industry, starting from the most important aspect of "save," in fact, "cost-effective retail" can also be divided into three categories: soft discounts, hard discounts, and absolute low prices:

① Low-price stores: This format mainly emphasizes the absolute low prices of goods, with product prices mostly limited to a certain range, such as ten yuan, hundred yuan stores, etc. However, one of the main reasons for the low prices in this format is that the products sold are mostly inherently low-cost, such as white-label or OEM products. In many cases, due to the low cost, the markup rate (or gross margin) of low-price stores is not actually low.

② Soft discounts: By selling defective goods, expired goods, off-season goods, etc., a business model is established to achieve ultra-low prices. The low prices in the soft discount model mainly come from the fact that the products themselves have some defects, but most of the products in this format have brands.

Therefore, the main value of retailers in this model lies in establishing good relationships with brands, ensuring a stable source of goods; still having outstanding abilities in product selection, or consumer snowball grasp, to ensure that the defective products they purchase have a high sell-through rate (rather than becoming inventory pressure).

③ Hard discounts: The goods sold under the hard discount model, their low prices come from retailers optimizing the supply chain, improving operational efficiency, self-produced goods, etc., to lower their own gross profit margin and benefit consumers And the products sold under hard discounts are all goods without quality defects, and even high-quality products, with prices that are not necessarily low.

Compared to the first two models where the low price depends on the product itself (external factors), hard discounts rely more on the retailer's internal efficiency to achieve low prices. Therefore, among the three "cost-effective retail" business models, hard discounts generally have the lowest profit margin, closest to the model of low profit and high sales volume.

In reality, Costco's gross profit margin has been consistently maintained at a low level of 12% to 13% for over a decade, significantly below the industry average, and the company has never had the intention to increase its gross profit margin. In comparison, whether it is Walmart and Target in the conventional supermarket model or Dollar Tree with absolute low prices (the American version of a dollar store), their gross profit margins range from 25% to 35%. Looking across markets, Jiajiale, which follows the hard discount model in China, also has a gross profit margin between 20% and 25%.

In terms of pricing, comparing the prices of the same products, Costco is generally 10% to 40% lower than Walmart (the largest in scale and should have the strongest scale effect), while the prices of other small to medium-sized regional chain supermarkets are 60% to 70% higher than Costco.

Therefore, whether across formats or markets, Costco is resolute in implementing low gross profit margins. Costco's low prices do not stem from low-quality/defective products or "squeezing" suppliers, but more from squeezing its own gross profit and operational efficiency internally, transferring the most benefits to consumers with the lowest markup rate.

3. "Low Price and High Quality" is the Winning Strategy

Although named "discount," Costco is actually positioned for middle-class consumers. According to research, Costco's customers spend over $100 per shopping trip, which is twice the average spending of about $50 at competitors Walmart and Target. (This is a different concept from the earlier comparison where Costco's prices were lower than Walmart's)

From a qualitative perspective, most of Costco's products on various social media platforms are also seen as a "synonym for high quality". For example, the use of "high-quality animal cream" and "imported high-quality durian" as raw materials are some evidence of the high quality of its products.

In other words, Costco excels in both "saving" and "quality". While its products are relatively low-priced, the quality is also relatively excellent. This is one of the main reasons why Costco can ignore cycles, maintain stability, and retain loyal customer flow.

Furthermore, Costco's positioning towards the middle class has two other noteworthy advantages:

Firstly, by setting a membership entry threshold and selling relatively expensive quality products, Costco actively selects and defines a relatively small and clearly defined user group, thereby being able to provide targeted products and services, increasing conversion rates. Moreover, theoretically, people with incomes above the middle class have stronger risk resistance and lower volatility in their daily consumption expenditures, which should also be one of the reasons why Costco's single-store sales fluctuate less than its peers.

Secondly, the significantly higher average customer spending also allows Costco to have a client's average profit margin that is not significantly lower than its peers, despite having a lower markup rate (i.e., gross profit margin). This gives Costco enough room to cover other operating expenses, so even without considering membership income, the theoretical profit margin left for Costco in pure retail business may not be significantly less than its peers.

As shown in the illustrative calculation table below, both Costco and Walmart earn an average gross profit of about $13 per single user shopping trip. This is just a preliminary introduction to this point, and a detailed discussion on the cost side will be discussed in another document.

4. Coexistence of Addition and Subtraction

In terms of "saving" and "quality", Costco can be said to have the best standards in the industry. However, from the perspective of "variety" - the richness of products/services, we believe that Costco's choice is a combination of "addition and subtraction".

In terms of the total number of product SKUs, Costco's choice is "less" (but refined). Representing warehouse club supermarkets like Costco, although mostly located in suburban areas with large store areas, the number of SKUs generally ranges around 4000, far lower than the around 20,000 SKUs of conventional large supermarkets.

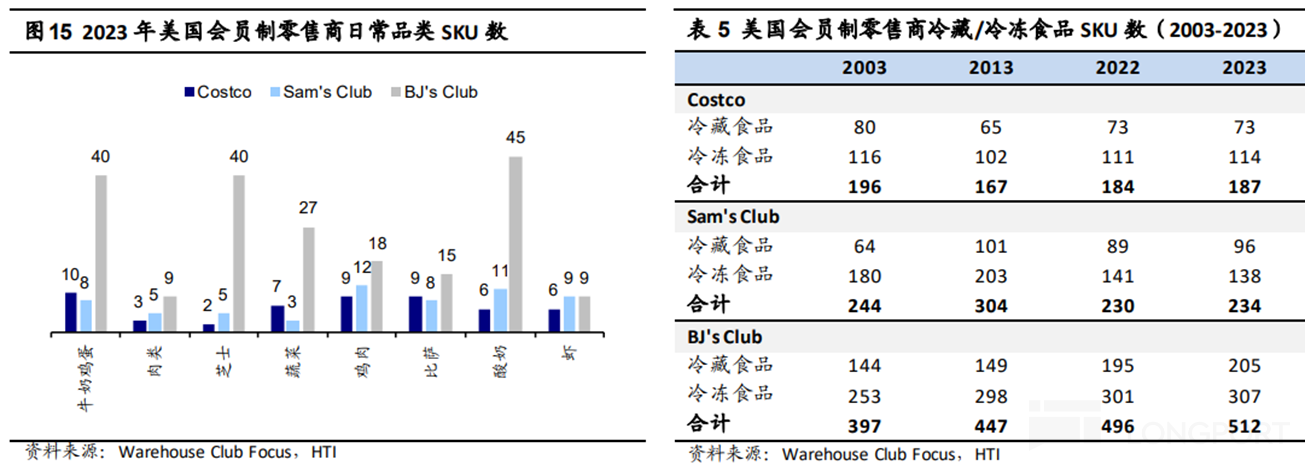

Even compared to Sam's and BJ's, which are also warehouse membership stores, Costco has the fewest product SKUs. For example, in fresh and frozen foods, Costco's product SKUs are roughly similar to Sam's but still about 30% to 40% less, and compared to BJ's, the product SKUs are more than half streamlined

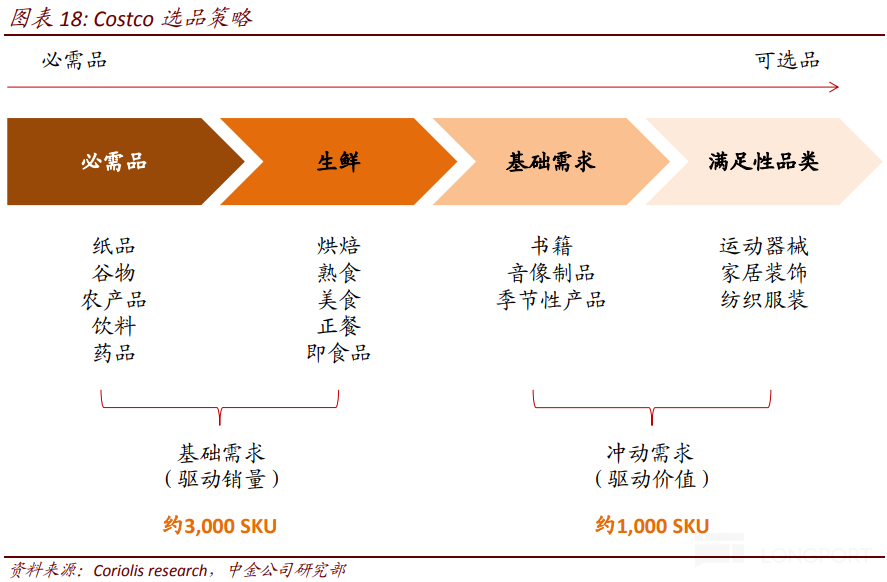

In terms of the structure of product categories, Costco allocates three-quarters of its only 4,000 SKUs to high-frequency and essential items such as food and daily necessities. Only one-quarter is allocated to lower-frequency and optional items such as clothing, home furnishings, and appliances.

Combining the above two points, the limited selection of products actually reduces consumers' decision-making costs (they won't be overwhelmed by choices), to a certain extent, benefiting sales. On the other hand, focusing products on fewer categories of best-selling or high-quality products also reduces the difficulty of product selection and supply chain management, which helps reduce costs (will be discussed in detail later).

In terms of category structure, concentrating three-quarters of the products on food and daily necessities, which are high-frequency purchases with relatively rigid demand regardless of the economic cycle, creates a stable and high-frequency customer flow for Costco. Then by selling optional products with higher unit prices and profit margins, they achieve high sales and profits.

From another perspective, food including fresh, refrigerated/frozen, and prepared foods are naturally not suitable for online sales + delivery, which is one of the reasons why Costco has not been heavily impacted by the penetration of online economy.

However, compared to the "subtraction" or "less but better" approach on the product side, Costco adopts an "addition" approach in additional services. Abstractly expanding business can have two directions: one is to expand the same business to different scenarios, such as expanding offline retail to online; the other is to incorporate various different formats into the same scenario.

Costco adopts the second expansion method by incorporating various types of services into the store, providing consumers with more convenient one-stop services, including:

① Similarly, high-frequency services such as refueling and dining, mainly to increase consumer stickiness. Due to the remote locations of Costco stores and the habit of American residents driving cars, refueling after driving to the store is a natural extension of the scenario. Dining is a higher-frequency consumption scenario than daily shopping. The extremely low-priced rotisserie chicken, hot dogs, and soda, among other popular items, are indeed one of Costco's traffic-driving measures.

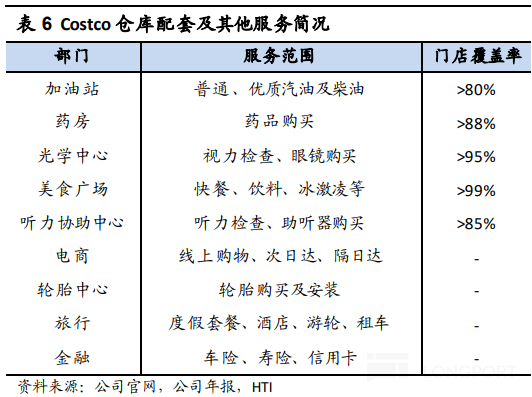

② Relatively low-frequency, optional, but higher profit margin services such as pharmacies, optometry, audiometry, and car maintenance. These extend from core daily shopping to low-frequency, optional, and from goods to services. They enrich the consumer shopping experience and to some extent increase profitability.

③ Spanning a wider range such as travel booking, insurance, credit cards, etc., these are typical light-asset, high-profit channel businesses, bringing a "secondary monetization" of the large customer flow to Costco's main business. Due to Costco's near-zero incremental customer acquisition cost in these channel businesses, even though these businesses are not Costco's core areas of strength, they can still increase the company's profits to some extent due to low incremental costs and high profit margins.

Risk Disclosure and Disclaimer for this article: Dolphin Research Disclaimer and General Disclosure