Apple's dominance in the App Store! Will WeChat's "hard resistance" be different?

I. Content vs. Channel, Epic Giants Clash

1. "Either-Or" is Pure Fiction, Controversy Lies in Revenue Sharing Ratio

Last week, the long-standing controversy between Apple and WeChat over the "either-or" issue finally came to a conclusion - the upcoming iPhone 16 has approved WeChat's update, and the iteration version submitted by WeChat in the past week has also been successfully launched. For a moment, in this clash of titans, WeChat was almost unanimously hailed as the "clear winner" across the internet.

The so-called "either-or" mentioned above did not originate from official sources, indicating that with the rapid growth of the mini-game market and many developers bypassing Apple's 30% commission through external links, Apple intends to strengthen control and require Tencent to clean up in-app and external links. Otherwise, Apple will reject WeChat's update, leading to the viral rumor of "iPhone 16 will not support WeChat".

In Dolphin's view, the "either-or" between the two can be considered groundless, especially since the rumored "either-or" was initiated by Apple as a form of "threat".

Upon reviewing the information, Dolphin found that neither Apple nor Tencent, in their official statements, mentioned the seemingly dominant but ultimately mutually damaging notion of "you can't have both" - the key point of contention between the two parties has always been the revenue sharing ratio, including the current situation where the approved iteration update is being launched. In other words, the crux of the tug-of-war between the two lies in the revenue sharing ratio.

Although Apple was the first to bring up the issue of "mini-program commissions" to the negotiating table, Tencent, having just won the battle against Android channels in the DNF mobile game war, is also actively involved in this negotiation during a crucial period where the U.S. and EU are forcing Apple to adjust its commission rates through tough legal actions.

2. WeChat is no stranger to Apple's commission controversy

Currently, within the WeChat ecosystem, the major sources of payment are e-commerce transactions of physical goods (for which Apple does not charge a commission), as well as payments for virtual goods and services, mainly from mini-game payments and public account rewards.

In the aforementioned user consumption scenarios, under the normal payment process, iOS users would have 30% deducted by Apple during payment. However, because mini-programs and public accounts operate within the WeChat ecosystem and do not involve the download process from the App Store, game developers can more easily circumvent Apple's commission through third-party links.

Regarding whether public account rewards should be "taxed", as early as 2017, Apple and Tencent had already clashed, although WeChat's reasons were evidently more justified - all reward amounts go directly to the individual public account, with WeChat not benefiting from it, as it does not constitute a platform's commercial activity.

From "WeChat cancels iOS reward function" to "Apple waives commission", the fluctuation of interests back and forth indicates that there is no overwhelmingly victorious party between the two sides

II. Why is Apple so persistent in pursuing the "fly leg meat"?

If we refer to the final result of "Apple giving up taxation" in 2017, then this time the payment for mini-games should also be exempt from the 30% commission. But why did Apple choose to stir up controversy again and cling tightly to this piece of interest?

It is well known that Apple is a global giant with annual revenue of nearly $400 billion and operating profit of nearly $120 billion.

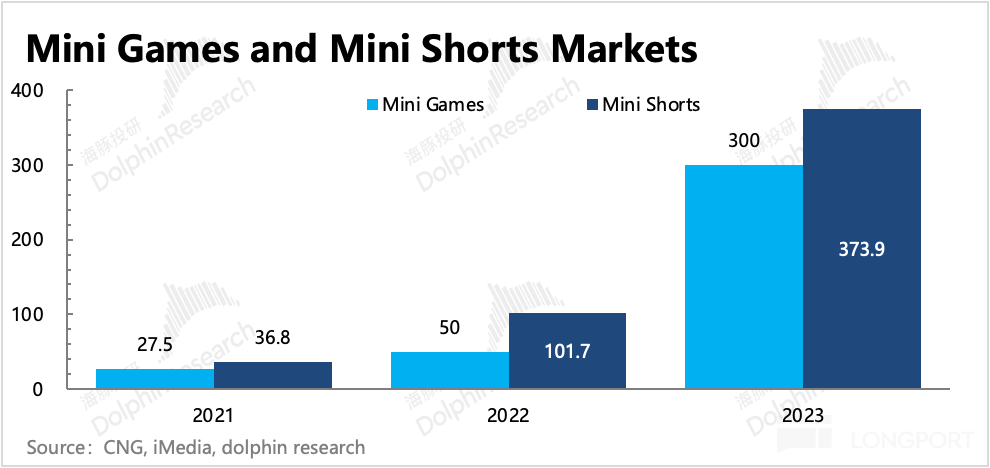

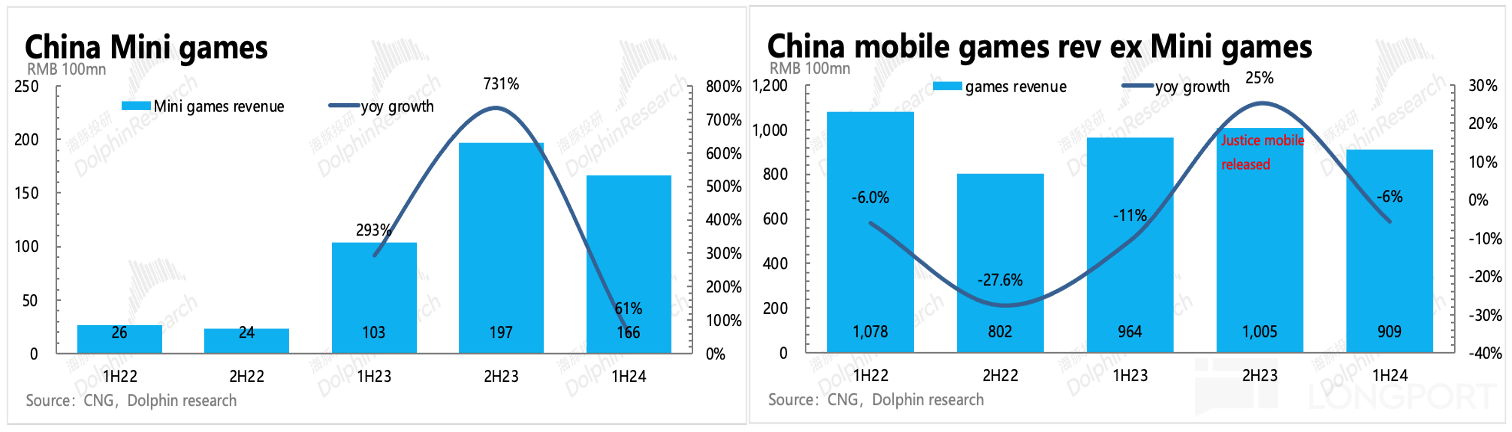

The scale of WeChat mini-games is expected to reach 30 billion in 2023 (source: Gamma Games), with in-app purchase revenue of about 15 billion. In addition, there is another short drama market worth 37.4 billion that Apple is eyeing (source: iMedia Consulting, mostly paid). Assuming Android:iOS=3:7, then the overall iOS in-app revenue for mini-games + short dramas is 480 billion.

If calculated at a 30% commission rate, even at the highest estimate, it would only bring Apple nearly 15 billion RMB, or about 2 billion USD in incremental revenue/operating profit, equivalent to 1.7% of Apple's annual profit. Yet, it is precisely this small piece of "fly leg meat" that Apple has changed its compromise attitude towards "public account rewards" from the past and seriously pursued.

Dolphin believes that the point Apple cares about this time also determines the room for Apple's possible concessions in the ongoing "commission negotiations" with Tencent.

1. Realistic experience, Apple also needs to plan ahead

Apple tax is the abbreviation for the commission that Apple charges on apps downloaded from the App Store, paid at the time of download and for subsequent in-app digital goods/services sales. The reasons for charging are:

1) For developers, the App Store provides a platform to reach high-quality users;

2) For users, the apps in the App Store are also high-quality and safe apps reviewed by Apple.

However, since iOS is a closed system and the App Store is the only app store in the iOS system, this commission that pays for the advantages of the App Store has actually become a mandatory "Apple tax".

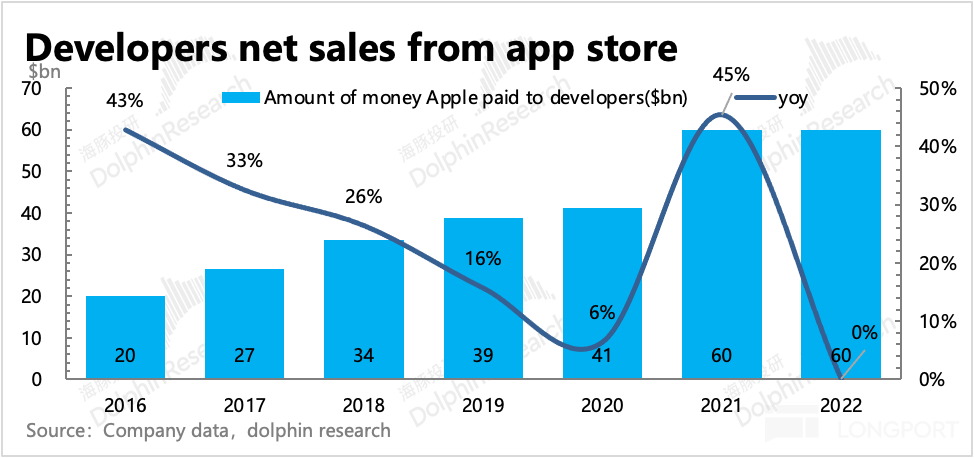

The App Store, launched in 2008, has gradually become an important driver of overall revenue growth as Apple's hardware shipments increase and global user penetration deepens.

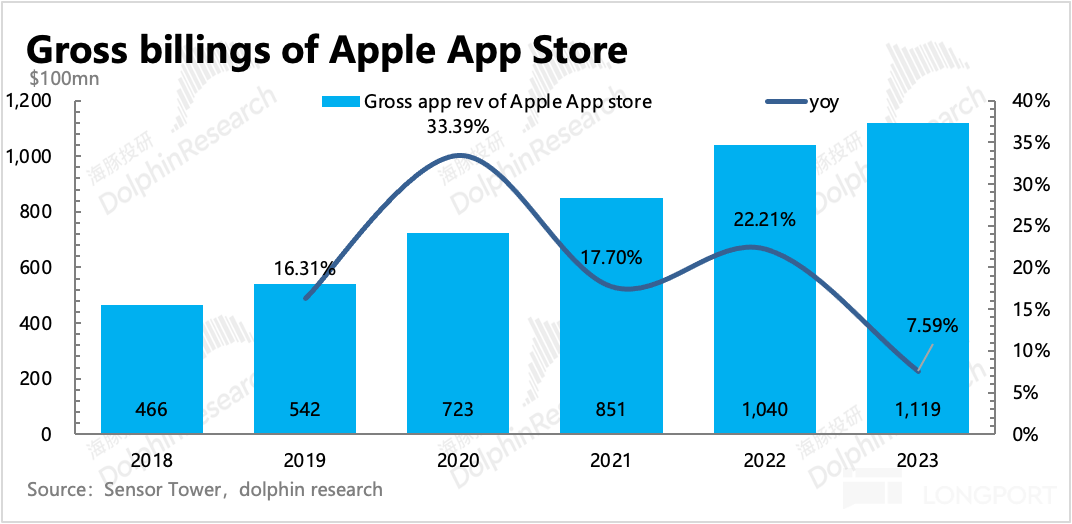

The revenue of the App Store is classified under the Apple Services category, and the official data does not provide further breakdown. The market generally uses the revenue provided by the third-party platform Sensor Tower, calculated simply based on a 30% commission rate. In addition, Apple also discloses ecosystem data (net sales paid to app developers since 2008), as well as data disclosed by courts in recent years regarding Apple tax litigation cases The above-mentioned income from different sources may vary. To maintain data consistency, the discussion below by Dolphin will mainly combine Apple's net sales data to developers, Sensor Tower data, and investment bank estimates as the basis for analysis.

In the 2023 fiscal year, overall Apple Services revenue was $85.2 billion, accounting for 22% of total revenue. Among them, App Store revenue is estimated at $25.8 billion, accounting for approximately 30% of Services revenue. The remaining subscription revenue (Music, iCloud, TV, etc.) and licensing revenue (revenue from default options, such as defaulting Google as the search engine) each account for around 30% as well.

However, looking back over the past decade, whether it is the official revenue share paid to developers by Apple or the transaction data tracked by Sensor Tower, it is evident that in recent years, the growth of App Store revenue has become increasingly challenging.

This clearly contradicts the market's valuation logic for Apple: In the past 3 years when hardware sales have become more difficult, Services revenue led by the Apple Store has been crucial in driving profit growth and supporting valuation (the commission revenue from the Apple Store has almost no cost). Therefore, from this perspective, exploring new growth for the App Store is becoming increasingly urgent for Apple. Compared to the "generous" treatment of public account tipping in the past, Apple's emphasis is no longer the same.

2. Mini-games represent a dual "increment"

However, while seeking growth is understandable, why did Apple specifically target mini-games, which are currently not yet large in scale?

Dolphin believes that Apple's focus on mini-games is not only due to the growth prospects of mini-games (penetrating light game users), but also the disruptive impact of mini-games on existing App games.

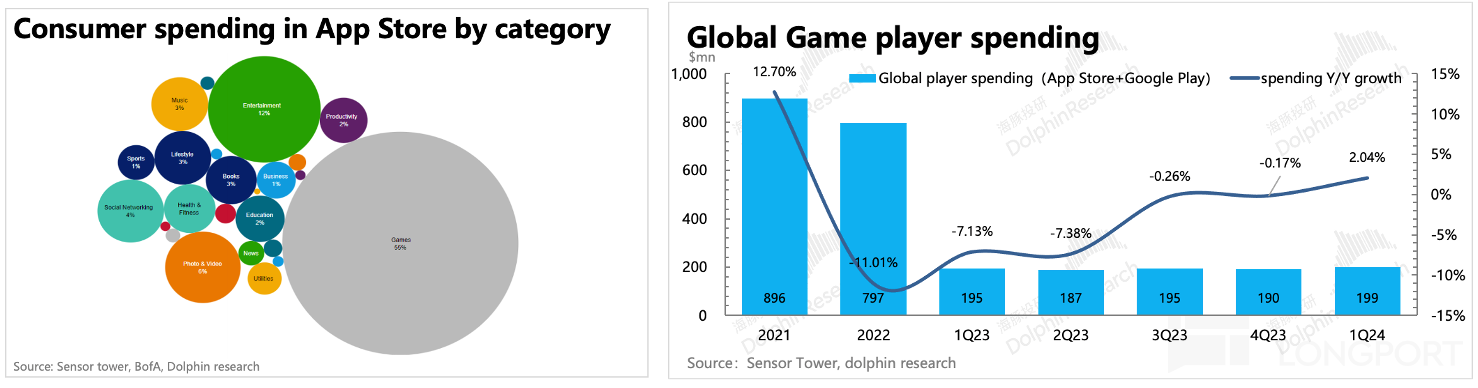

As we all know, in the in-app payment revenue on the App Store, game apps contribute the most, reaching 55% of total revenue in 2023. However, after the pandemic lockdown, the online stay-at-home economy boom has faded, coupled with the impact of the pandemic on new product supply (extending the product production cycle), the global mobile gaming market itself has been sluggish.

According to Sensor Tower's disclosed total revenue from user payments on the App Store + Google Play, mobile game payments decreased by 11% in 2022 and continued to decline by 4% in 2023.

In the Chinese market, in the year 2023 when casual games completely exploded, apart from the significant contribution of "Justice" to the industry's revenue, the revenue of App games has been in a negative growth state for the past two years.

With the expected growth of casual games exceeding 50 billion in the coming years, the revenue from Apple's App Store, if the market share does not further increase along with the penetration of iOS users, will naturally have a greater impact.

III. Reviewing the results of the global five-year struggle: How much has Apple really compromised?

Although the growth rate of Apple Store revenue has slowed down, app developers' resentment towards Apple's commission has not diminished at all. Google Play also faces the same issue. Although Google's Android system is not closed and allows the existence of third-party app stores, relying on an open model has accumulated a larger user base and more application software over the years, resulting in a considerable amount of Google's commission.

1. First round of adjustments: Proactive, globally unified, benefiting small apps

In 2020, with relentless protests from various parties such as Epic and Spotify, and subsequent regulatory scrutiny, Apple and Google successively raised the flag of friendship:

(1) At the end of 2020, Apple announced that starting from January 1, 2021, for apps joining the App Store Small Business Program (annual net income below $1 million, i.e., revenue below $1.3 million), the commission rate would be reduced from 30% to 15%. However, for those with revenue exceeding $1 million, they would continue to follow the 30% "Apple tax rate."

(2) In 2021, Google reduced the rate for businesses with revenue below $1 million per year from 30% to 15%, but for the portion exceeding $1 million, a 30% commission would be charged.

Both Apple and Google mentioned the $1 million threshold for different rates. Although both companies claimed that over 90% of the apps on their platforms met the condition of annual revenue below $1 million and would enjoy the reduced rate, for the pyramid distribution of platform revenue structure, developers with revenue exceeding $1 million per year, although accounting for only 10%, contribute 70% to 90% of the revenue.

Therefore, even if the rate for developers below $1 million is reduced to 15%, the actual impact on the overall App Store commission income is less than 2%. Apple and Google can still enjoy a 30% commission on the vast majority of revenue.

Therefore, such adjustments have not actually addressed the core demands of non-small and micro app developers like Epic and Spotify: allowing the existence of other app stores within the system to compete with the App Store; allowing third-party payment redirection. **

2. The second round of adjustments: passive, differentiated treatment, opening up payments, and significant fee reductions

If the first round of adjustments was initiated by the head and major developers, with regulatory agencies serving as auxiliary forces, then the second round of adjustments is more of a round of rectification led by regulatory agencies from various regions themselves.

Apple and Google also have their own strategies to deal with this. In contrast to the first round, where Apple and Google took proactive small measures to appease public anger, in the second round, their main strategy in response to regulatory lawsuits can be summed up in one word - "delay".

While app developers can directly influence public opinion, lawsuits and rulings by regulatory agencies require detailed evidence and strict adherence to relevant laws. However, global laws in different regions are not uniform and legal provisions are not perfect, leading to significant differences in enforcement decisions.

Among them, the EU, South Korea, and other regions that are actively promoting reforms need to amend laws while filing lawsuits, not to mention that many other regions' regulatory agencies have not actively initiated reviews and charges against Apple.

Therefore, Apple and Google's strategy is to "delay" and wait for the opponent to make a move. On one hand, they repeatedly entangle with the regulatory agency's rulings to delay time; on the other hand, they treat different regions differently. If the platform loses the lawsuit, adjustments will only be made in the corresponding region, while other regions remain unchanged. This is different from the first round of adjustments, where they proactively made adjustments uniformly.

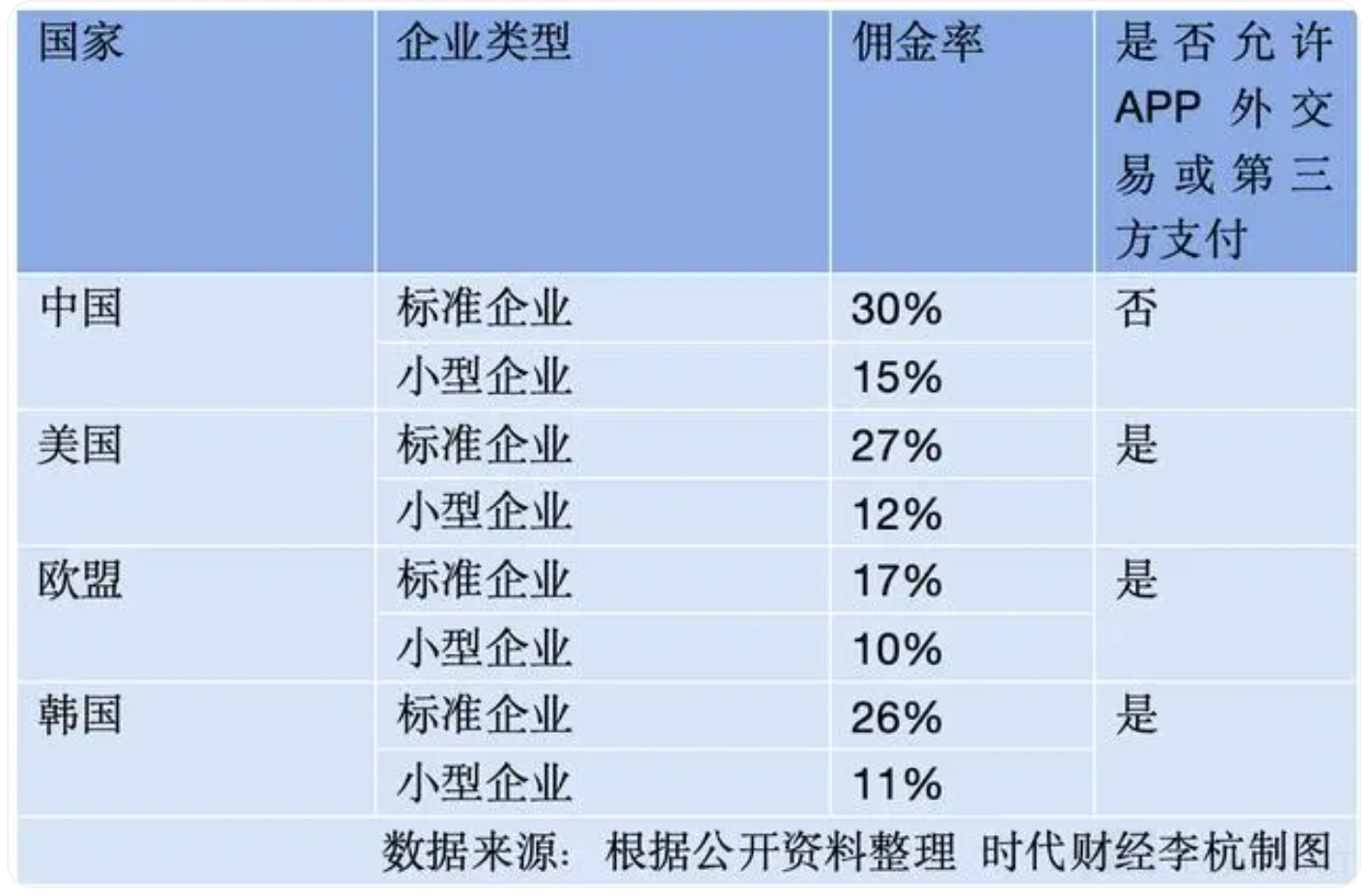

As a result, as of now, both Apple and Google have encountered issues with different fee rates in different regions. In the recent WeChat battle with Apple, Chinese media also highlighted that "fees in China are higher than in other regions" as a point of attack in public opinion. The following image is a widely circulated fee comparison chart in media articles.

But are fees in other regions as discounted as they appear on paper? The Dolphin believes not entirely. Through careful study of the new fee rules, the Dolphin found that in the actual implementation process, it may not be easy to obtain the displayed discounts. While Apple adjusted the commission rates, they also sneakily added a bunch of supplementary clauses.

Taking the South Korea region, which was adjusted in 2021, and the recent uproar in the European region as examples, let's see how much Apple has truly compromised:

(1) Breaking new ground in South Korea: Allowing third-party payments, but are developers really saving money?

The legal battle between South Korea's regulatory agency and Apple lasted from 2021 to 2022, and finally, after the revision of the "Telecommunications Business Act" (prohibiting app store operators from forcing developers to use specific payment methods), they successfully made a ruling allowing the use of third-party payment channels for Apple and Google.

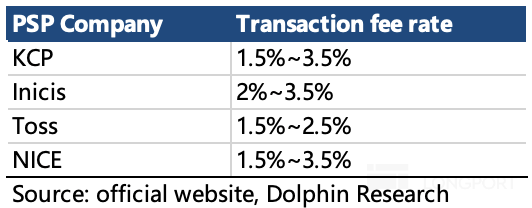

However, while allowing the use of other payment methods, developers still have to pay the commission, just with a reduction of a 4% payment processing fee, meaning the standard rate has been reduced from 30% to 26%. For developers under the "Small Business Program," the rate has been reduced from 15% to 11% However, when developers choose a third-party payment channel, they can only select from the list of PSP payment service providers pre-approved by Apple, and they need to embed special technical modules to ensure transaction security, prompt users when using payment methods other than Apple Pay, and regularly submit sales bills to Apple.

Currently, there are only four options available, and the rates vary depending on the source of funds behind the users, such as credit card payments having a higher comprehensive rate and electronic wallet payments having a lower rate:

Although the rates of the above service providers (local transactions in South Korea) are slightly lower than Apple's tax preferential rate of 4%, considering some additional upfront technical costs and additional processing fees (1%~2%) for cross-border payments, for some merchants, the cost-effectiveness of using a third-party PSP may not be as good as using Apple Pay.

After more than a year of hard work, the South Korean government finally made a lonely breakthrough in the Apple App Store fortress.

(2) The EU is closely following: a significant reduction in commission rates, but is it really easy to implement?

Compared to the South Korean government's tentative approach, the actions of the EU regulatory authorities are more significant, especially after the passage of the Digital Markets Act (DMA) in March last year, the EU accelerated its antitrust scrutiny of global tech giants.

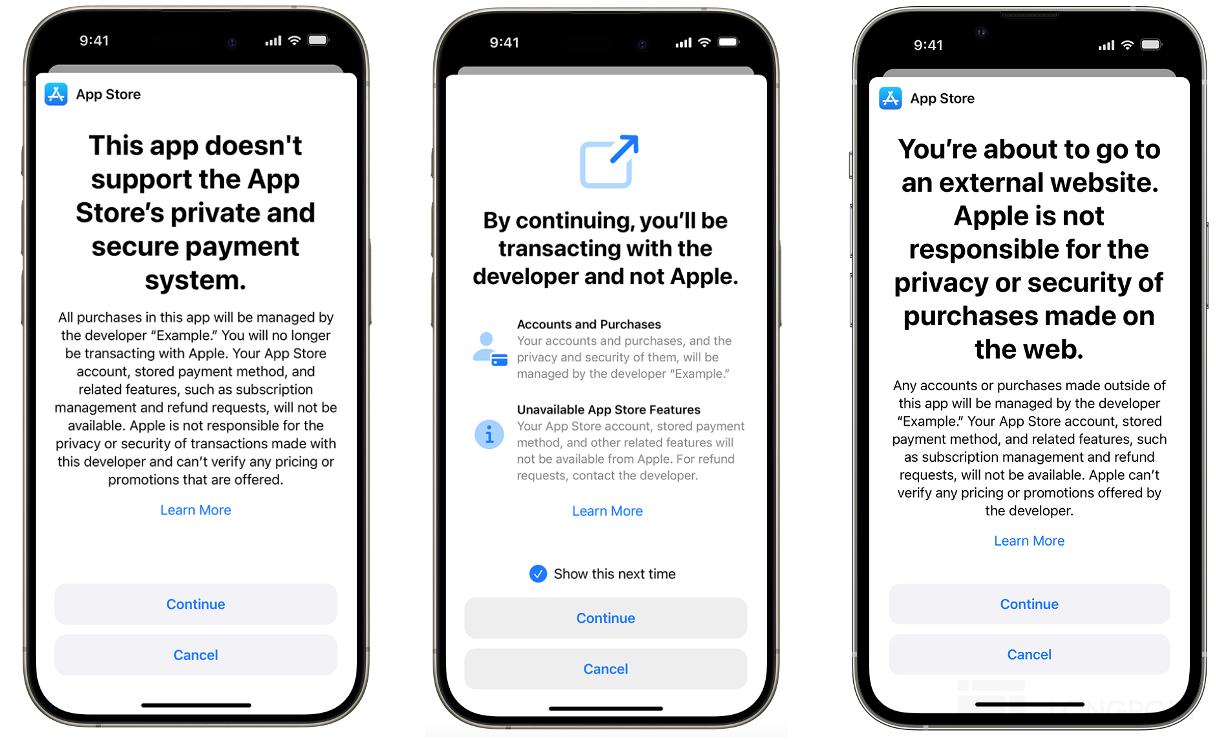

For Apple, the main violations of the DMA are the monopolistic position and forced exclusivity of the Apple Store. Earlier this year, after the EU announced a ruling that Apple violated the DMA, with a maximum penalty of 10% of global revenue, Apple made a major modification to the fee policy of the Apple Store in the EU region for the first time, with the main points being:

While retaining the existing rules, new rules are introduced as alternative options for developers. Under the new rules:

a. Developers can choose third-party app stores outside of the Apple Store, but each app can only be downloaded from one app store.

b. Developers can choose payment service providers other than Apple Pay for in-app purchases, or redirect users to external web pages for payment, but they need to apply to Apple for authorization for external purchases through Storekit or external link purchases. In addition, developers need to configure additional technical modules and provide users with "non-Apple Pay transaction security alerts."

c. For revenue generated by developers through the Apple Store, the Apple tax rate has been reduced from 30% to 17% + 3% (credit card payment processing fee) = 20%. For app developers who join the Small Business Program, the original 15% rate has been reduced to 10% + 3% (credit card payment processing fee) = 13%.

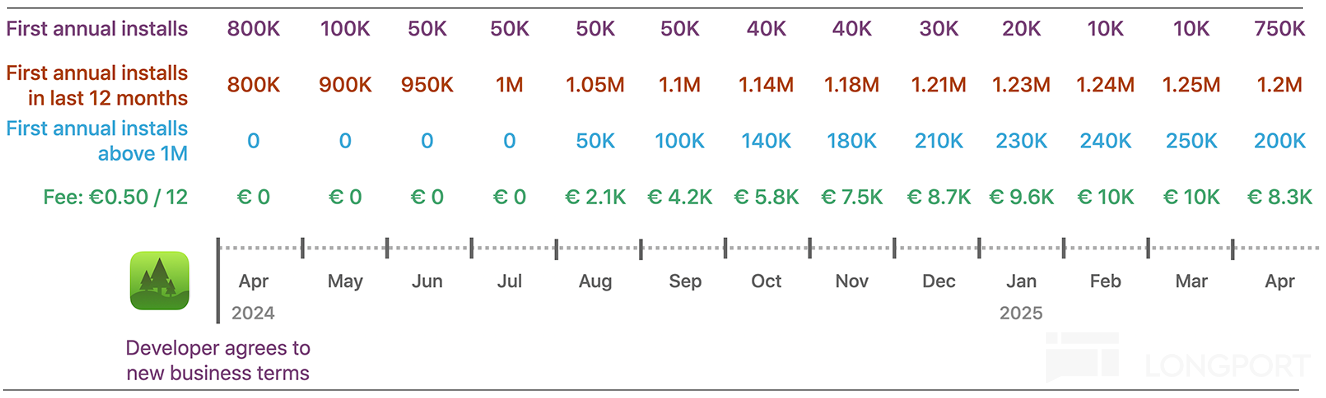

d. However, choosing to adopt the new rules will require a core technology fee to be charged for some apps that exceed 1 million first-time installations within a 12-month period, at a rate of 0.5 euros per installation Definition of "Annual First Installation": The total number of first downloads for each Apple account within a 12-month period. This includes downloads from other app stores; repeated downloads by the same Apple account on multiple iPhone devices count as one; downloading after an app update counts as one; downloads on devices other than iOS such as iPadOS, MacOS count as multiple downloads, and reinstalling after uninstalling also counts as multiple downloads.

The above is the version from the beginning of the year and was implemented in March. Some investment banks have estimated the potential impact of this adjustment on Apple's profits. Due to its implementation only in the European Union (where the App Store revenue is expected to account for 7%) and with some additional payment terms (such as new CTF fees), the final impact is minimal. Our rough estimate suggests a revenue impact of only around 0.2% and a profit impact of 0.5%.

While Apple Store did experience some pressure due to regulations (as discussed earlier, the adjustments in the Korean region cannot be considered as concessions), soon after, European software companies led by Spotify jointly sent a protest letter to the European Commission, pointing out that Apple's adjustments to the App Store rules still do not comply with the relevant provisions of the DMA:

a. Since the original App Store charging rules did not comply with the DMA, why were they allowed to coexist with the new rules?

b. Questions regarding the newly added core technology fee CTF and payment processing fees. Although Apple claims that only 1% of developers in the European Union need to pay the CTF fee, Dolphin Jun found through a simple calculation that for apps with a large DAU (which contribute the majority of the App Store revenue), the download fee may potentially increase additional costs, resulting in Apple's final tax exceeding 30%, leading developers to abandon the new rules.

c. For external link download methods, complex "security" steps are set up (requiring users to manually confirm the "accept installation from this website" option) and pop-up warnings about risks. For users using payment channels other than Apple Pay, similarly, "intimidating warnings" are set up.

In June, the European Union still ruled that Apple did not comply with the DMA and continued to demand Apple to make changes. In early August, Apple once again adjusted the App Store rules. This adjustment mainly focuses on point c mentioned above, which is to reduce friction in the use of external link downloads and payment methods.

1) Developers are allowed to promote and advertise downloading and payment methods other than Apple's within their own apps.

2) The "security steps" required for users to adjust settings before clicking on external links will be eliminated.

3) External links within the app can have multiple URLs and are no longer restricted in format. However, developers are not allowed to track and locate user behavior through URLs for commercial advertising purposes.

4) The "security prompt" will continue to appear, but if users choose not to be reminded again, the prompt will stop appearing in the future.

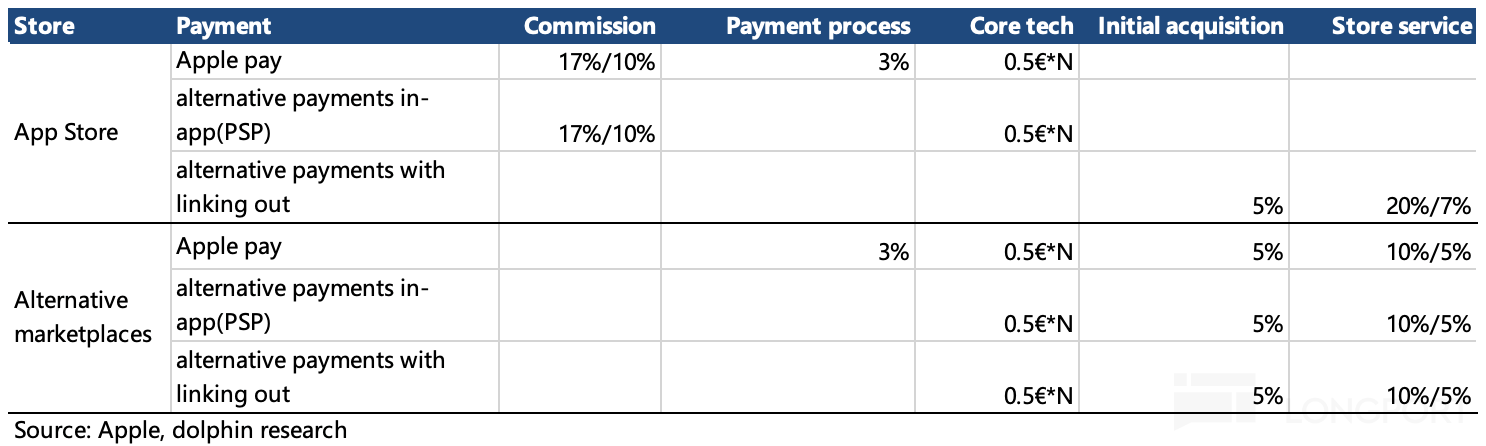

However, Apple has not canceled or adjusted the controversial CTF fees. Even more outrageous is that in the developers' apps, Apple also wants a share of the sales revenue from other app stores and alternative payment channels. This seems more like a punitive fee for developers using third-party services outside of Apple:

The cost for developers to flexibly introduce external links in the app and guide users to make purchases through external links involves paying two fees based on a certain percentage of this revenue (initial acquisition fee of 5%, store service fee of 10%). This is to reflect the value of Apple providing the functionality to reach iOS users, as well as app distribution, management, and review functions.

a. Initial Acquisition Fee: Within 12 months after the first installation (each software update or re-download will reset the period), users purchase virtual goods or services through external links promoted within the app distributed from the App Store. Apple needs to charge a 5% fee on any platform to demonstrate the distribution role of the App Store.

b. Store Service Fee: In addition, developers also need to pay a 10% fee on any platform to Apple, reflecting the value of Apple providing services such as app review, app store security, anti-fraud checks, etc. For those joining the Small Business Program and having automatic subscriptions for over a year, the fee is discounted to 5%.

If the alternative clauses for the EU are not chosen, the store service fee for running apps in the App Store and generating revenue through external links will be 20% (7% for small businesses), but the Core Technology Fee (CTF) will not be required.

Dolphin summarized the new fee rules adjusted in January and August, finding that Apple has been introducing new fees to achieve a "surface commission reduction" without actually affecting its core revenue goals.

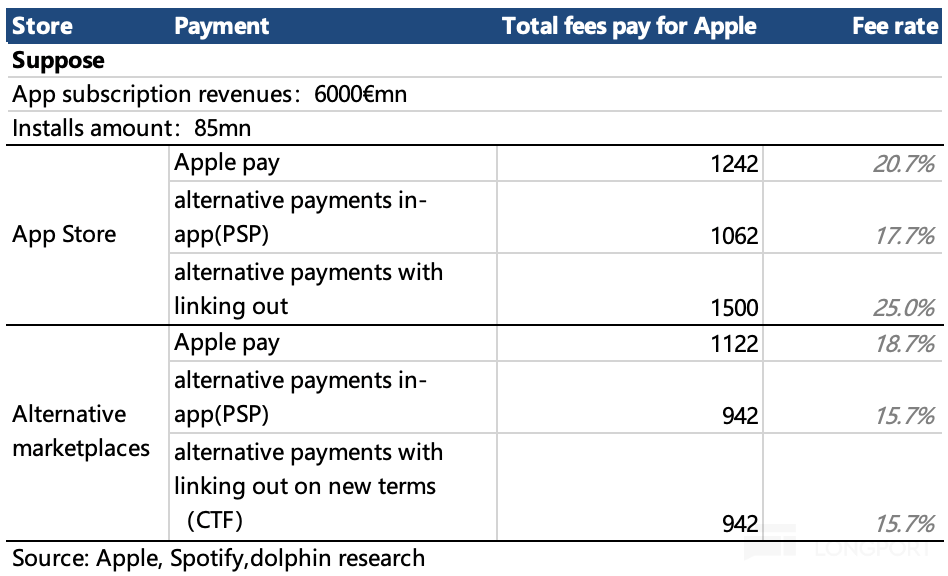

For example, taking Spotify as an example:

As a company in the EU region, we estimate that Spotify's subscription revenue in the EU region in 2023 will exceed 6 billion euros, with an average of 160 million active users in the EU. In 2022, Spotify's global downloads were 238 million times, and in 2023, the MAU user base grew by 20%. Based on this growth rate, it is estimated that the global downloads in 2023 will exceed 300 million times. Based on the EU user proportion, it is estimated that the annual download volume in the EU region is about 85 million times According to different scenarios, the commission rate for Apple ranges from 15% to 25%. However, it should be noted that when Spotify guides users to download from other app stores or use other payment channels, in addition to the commission to Apple, they also need to pay a share to other platforms.

Since the fee rates of payment service providers are relatively low, around 2-3%, but considering the upfront investment required for using external payments to develop certain technical modules and the subsequent regular reporting of sales, the cost-effectiveness analysis seems to favor the combination of the App Store and Apple Pay (20.7% in the figure below). In other words, through a series of complex operations, Apple continues to strengthen the monopoly of the App Store within the iOS system.

The complexity of these charging rules also increases the difficulty for the EU regulatory authorities to conduct follow-up reviews and tracking. This seemingly unsolvable problem continues to be delayed.

IV. Mini-programs are inevitably exploited, but WeChat's breakthrough is not impossible

Based on the above analysis, it is believed that although WeChat is not at risk of being excluded from iOS, a certain commission fee still needs to be paid.

1. There is a lack of regulatory impetus to counter Apple's tax domestically

Looking back at the experiences of various regions in their struggles with Apple:

(1) Developers have mostly "lost" in their battles with Apple. They may win lawsuits, but it is difficult to implement real changes, and the more common outcome is to guide users to pay on their official websites. However, from the perspective of user habits and convenience, this is unreasonable.

(2) However, when regulatory agencies take the lead and use administrative measures such as high fines, they force Apple to adjust proactively. Although the adjustments may not happen all at once and may require some negotiation, there is at least some flexibility.

For example, the power of the EU DMA legislation, although the optimal solution may still be the App Store and Apple Pay, the overall comprehensive fee rate has indeed decreased from 30%.

However, in China, regulatory agencies rarely give severe judgments to foreign companies. In May this year, the Shanghai Intellectual Property Court ruled on a lawsuit filed by individual consumer Jin against Apple's Apple Store in 2021 for abusing its market dominance and unfair high pricing. It was determined that Apple has a dominant market position, but due to the inability to accurately calculate the relationship between commissions and operating costs, the 30% charged by Apple does not fall into the existing highest tier in the market (50%). Additionally, the lawsuit was dismissed based on reasons such as Apple Pay being exclusive but ensuring data security and transaction security.

Moreover, Apple's production capacity in mainland China provides a large number of jobs. From the perspective of social stability, domestic regulatory agencies mostly turn a blind eye to Apple in the short term. It is relatively difficult to regulate the behavior of giants like in South Korea and the EU by amending laws

2. Full commission exemption is hopeless, but there is hope for negotiating lower commissions between giants

Therefore, completely avoiding Apple, eliminating commissions, is not feasible. In the past, the market size was small, and Apple's App Store was not in a hurry to grow. Now that it has been targeted, trying to bypass it is like actively seeking trouble.

However, theoretically, mini-program games do not rely on Apple's App Store for promotion and distribution, but parasitize on the WeChat ecosystem. At the same time, transactions in mini-programs are peer-to-peer between users and developers, not between users and WeChat. WeChat only provides basic technology and platform ecology, covering platform operating costs and sharing some revenue through a portion of the commission.

Therefore, Tencent treats the revenue from mini-games as Net revenue, unlike App-end exclusive/self-operated games which are recognized based on Gross revenue. Based on this logic, there is actually no reason for the App Store to take a commission, at most an additional 3% payment processing fee for transactions using Apple Pay.

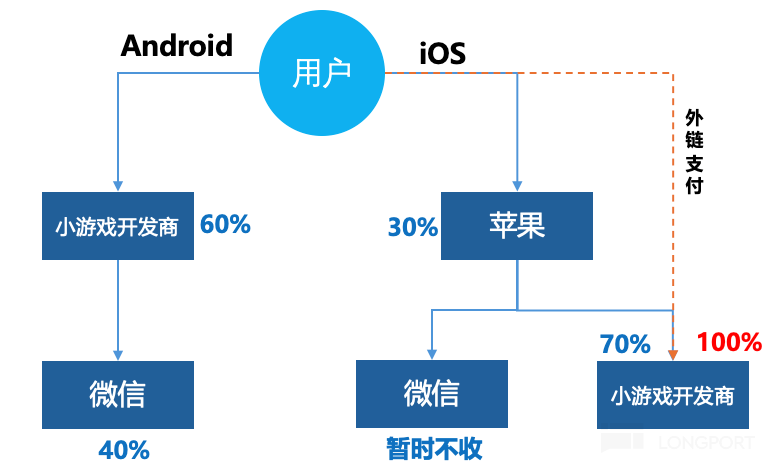

Before bypassing the Apple Store, because in-app payments in mini-games still need to go through Apple Pay, after Apple deducts a 30% commission, WeChat does not initiate additional commissions for these mini-game developers. On the Android platform, app stores operated by Huawei, Xiaomi, OPPO, VIVO, etc., do not charge commissions, while WeChat charges 40%.

In other words, in WeChat mini-games on the iOS platform, the portion of the "hard work fee" that WeChat should receive as a provider of basic technology, promotion, and distribution ecosystem, is actually taken by Apple.

Of course, Apple's "domineering" behavior is not only targeted at WeChat. It can be said that there is widespread anger over the Apple tax issue. Let's take two platforms similar to WeChat as examples:

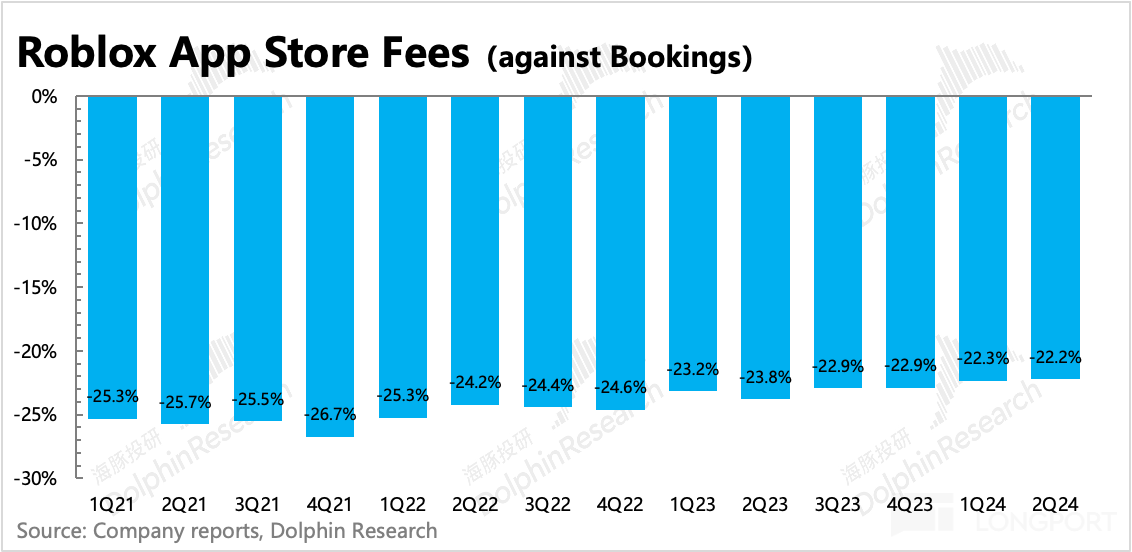

(1) Roblox: Similar to WeChat's in-app ecosystem.

In Dolphin's view, Roblox also functions as an in-app ecosystem platform (promoting and distributing in-app mini-games). Although users make purchases within the app by buying Robux coins from Roblox, to some extent, when users spend in a specific mini-game on Roblox, it is also a "peer-to-peer" sales activity.

Nevertheless, Roblox still cannot escape Apple and Google's commissions, with these App Store fees and other expenses accounting for as much as 22% of Billings.

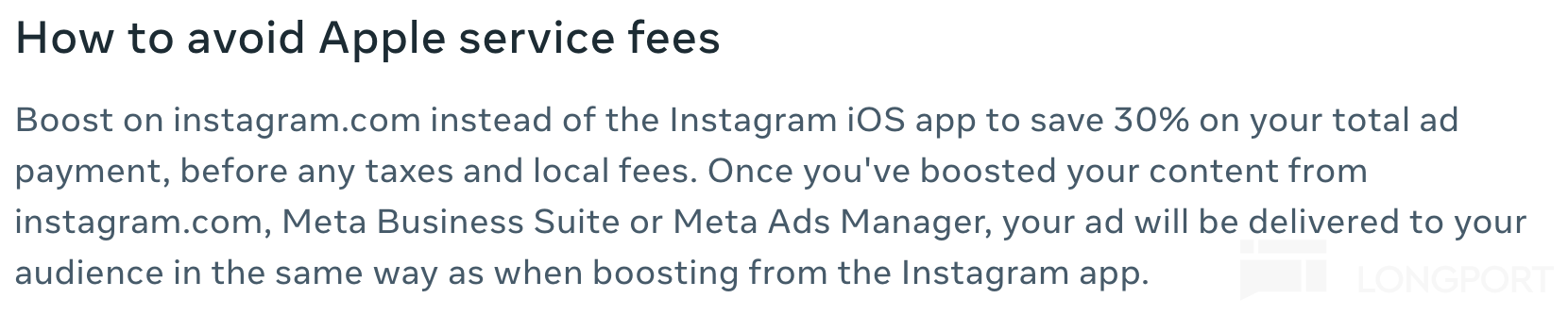

(2)Meta: Apple Tax Even Advertising Fees Are Not Spared

Meta's social platforms Facebook and Instagram mainly monetize through advertising, with almost no other paid content projects. Within FB and Ins, advertisers can promote their posts by paying for exposure to traffic. However, if advertisers choose to directly recharge and pay within iOS mobile apps, they cannot escape Apple's 30% cut.

Although compared to Roblox, which is essentially a third-party "peer-to-peer transaction," advertisers pay Meta directly,

Therefore, at the beginning of this year, Meta introduced ways for advertisers to bypass the Apple tax: Recharge through FB/Ins's web official website, and then consume within iOS; achieve advertising effectiveness through Meta Business Suite or Meta Ads Manager.

Apple's response is to openly condemn Meta for teaching people how to bypass the Apple Store ecosystem.

In summary, under the supervision of regulators in the United States and South Korea, only 3% of the payment rate has been adjusted, Apple's adjustments under the tough stance of the European Union are still being tested repeatedly, the ambiguous judgment of Apple tax in China due to incomplete related laws, and the cases of Meta and Roblox in the corresponding industry all indicate that touching Apple's cake is not that easy. Therefore, it is basically impossible for WeChat mini-games to completely avoid Apple's commission.

Although it is possible to bypass by guiding payment to the web end, compared to app games that attract players with "convenience," the demand for convenience from users of mini-games relying on "lightweight" will also be higher, and "in-app payment completion" is the main requirement of users.

Currently, due to the issue of revenue sharing ratio with Apple, Tencent has not commercialized WeChat mini-games on the iOS side, but doing it for free public welfare is definitely not Tencent's ultimate goal, after all, the number of mini-games within WeChat has rapidly expanded, and whether it is basic operations or optimization of the WeChat ecosystem, costs will continue to be incurred.

Therefore, this time Tencent also has sufficient motivation to actively negotiate with Apple. At the same time, as mentioned earlier, at a critical period of global channel waving, Tencent, the largest traffic source in China, also has hopes of becoming the dominant party in the revenue sharing ratio negotiations.

At the recent Apple new product launch event, when showcasing the chip performance of iPhone16, the game demonstration segment chose Tencent's next blockbuster game "Honor of Kings World," indirectly indicating that the relationship between the two is not cold, and negotiations are likely progressing smoothly.

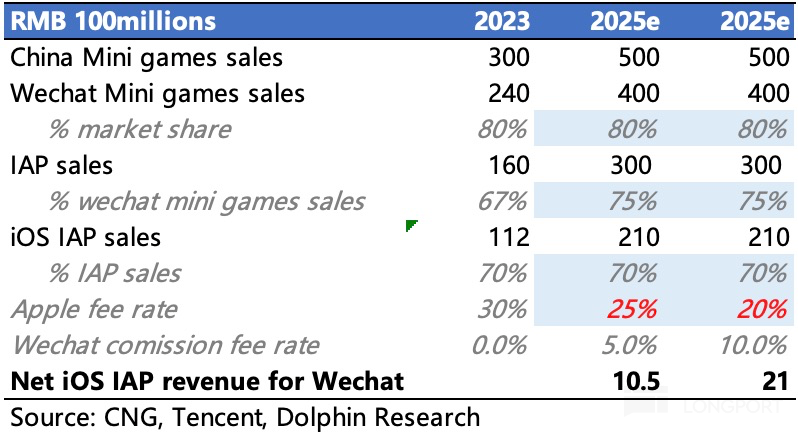

Referring to the adjustments in the European Union region (17%~25%), Dolphin expects to have a chance to offer a preliminary discount of 5%~10% on top of the 30% base for Apple, that is, the commission rate will be in the range of 20%~25%.

Although the Apple tax is difficult to chew, after all, mini-games are actually not related to Apple. With WeChat, the first-class traffic in front, the App Store has not had much impact on mini-games.

In this way, WeChat will correspondingly charge 5%~10% of the revenue from mini-games on the iOS side, for mini-game developers, the overall channel distribution cost of 30% remains unchanged.

Assuming that the final adjustment as mentioned above, Tencent's mini-game revenue in 2025 is expected to increase by 10-20 billion yuan from the original base, note that this incremental revenue is almost pure profit.

The revolution has not yet succeeded, and comrades still need to work hard. Although from the assumption in 2025, the reduction of the commission rate for mini-games on iOS by 5~10 percentage points has limited impact on Tencent's profit increment. However, Dolphin believes that this negotiation leveraging mini-game commissions is expected to open up a bigger market for iOS App games in the future.

When the toughest nut Apple starts to loosen, other channel platforms with weaker barriers will naturally compromise towards lower commission rates, a global content channel revolution is finally beginning, and the feast for content creators is truly approaching.

Dolphin Research on "Content Channel Revolution" Related Articles:

June 21, 2024, " With the New "King" in Hand, Tencent is Fighting with Channels Again》

Risk disclosure and statement of this article: Dolphin Research Disclaimer and General Disclosure