Broadcom: "Buy, Buy, Buy" paving the way to a "trillion-dollar" road? Tencent and Alibaba should learn!

In the leading technology companies in the United States, Broadcom has always been a "special" presence. Companies like Apple, NVIDIA, AMD, etc., have all developed and grown through self-developed technologies and internal growth. However, Broadcom is a "freak", always "buying, buying, buying", even to the extent of small fish eating big shrimp, gradually transforming itself from a small transparent company to the current $80 billion company.

All of the company's core business capabilities are acquired, including network business, wireless business, ASIC, and software business, among others. Many companies, after acquiring new businesses, end up mismanaging them and becoming a burden. In contrast, Broadcom has shown significant improvement in operations and continues to grow. In this regard, Alibaba may be a very typical negative case, and Tencent's investments are not as efficient as Broadcom's.

$Broadcom(AVGO.US) has repeatedly brought in top private equity firms for its acquisitions, analyzing the feasibility of acquisitions from operational and financial perspectives, making Broadcom a platform for excellent companies to go public.

Broadcom's acquisitions often have distinct characteristics:

1) Business aspect of the acquisition target: Leading technology or market share in a certain field;

2) Operational aspect of the acquisition target: Inefficient operations, especially high costs directly affecting the company's final profits;

3) Source of acquisition funds: Self-owned funds and stock cooperation with financial consortium loans, through leveraged acquisitions;

4) Post-acquisition operations: Retain core business, divest and sell the remaining parts of the business. Through operational integration, reducing the company's overall operating expense ratio to increase profits and EBITDA. Selling off some businesses can reduce losses and also repay some loans.

The current acquisition of VMware by the company will also be a microcosm of each acquisition case. After the acquisition and consolidation, the company's overall operating expense ratio has already started to decline, and the company's gross profit margin is expected to return to 70%.

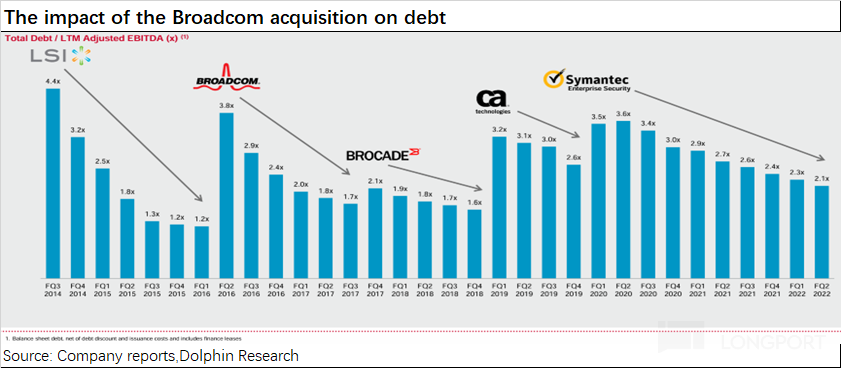

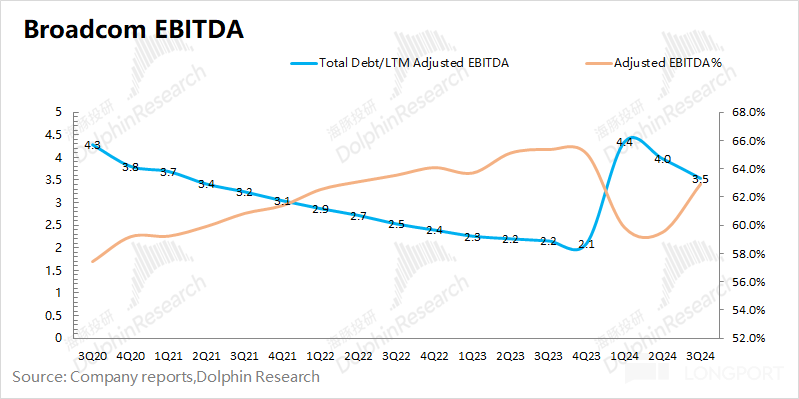

Therefore, Broadcom's development is a story of extreme "acquisitions and mergers". From an investment perspective, the company also considers EBITDA as one of the core goals of company operations. The total debt/adjusted EBITDA ratio is also an indicator that investment companies use to measure a company's debt repayment ability. Historically, each time the company acquires and consolidates, it happens when this ratio drops to around 2 times. With the VMware consolidation, the relevant ratio has once again risen to over 4 times, and Broadcom is currently focusing on business integration. As the relevant ratio drops to around 2 times again, the company may embark on a new round of acquisitions.

As Broadcom differs from traditional tech companies, the core logic of the company's development lies in external mergers and acquisitions. Therefore, in this article, the focus is mainly on the company's acquisition strategy. In the next article, the focus will be on the company's business situation and investment value Dolphin's specific analysis of Broadcom (AVGO.O) is as follows:

I. Broadcom: The King of Mergers and Acquisitions

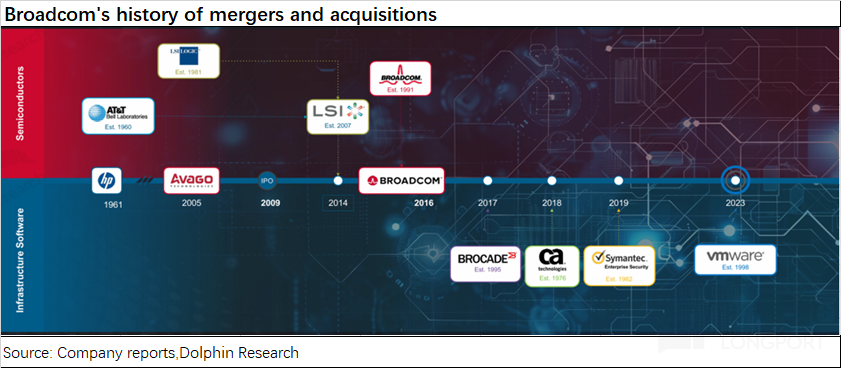

Unlike other companies that focus on internal development, Broadcom's growth mainly comes from external mergers and acquisitions. Through M&A integration, Broadcom started from HP's semiconductor division and has now become a tech giant spanning hardware and software.

After spinning off from Agilent (a division of HP), KKR and Silver Lake renamed the company to Avago, and 3 years later, they made their first acquisition of Infineon's BAW business. From then on, the company continued to acquire Cyoptics, LSI, and Broadcom. In about 10 years, Avago transformed from a semiconductor division into one of the top five semiconductor companies globally. The company's pace has been to acquire a company every 2 years. Originally, the company planned to acquire Qualcomm in 2017, but the deal was eventually blocked by the U.S. government.

As Broadcom had already become a leading company in the global semiconductor industry, after the Qualcomm acquisition was blocked, the company shifted its focus to software business. Subsequently, the company acquired CA Technologies, Symantec, with software business accounting for 20% of its revenue. With the inclusion of VMware, the revenue from the software business quickly caught up with the hardware side.

After a series of acquisitions, the company has transformed from a single semiconductor hardware company into a tech giant with both software and hardware capabilities.

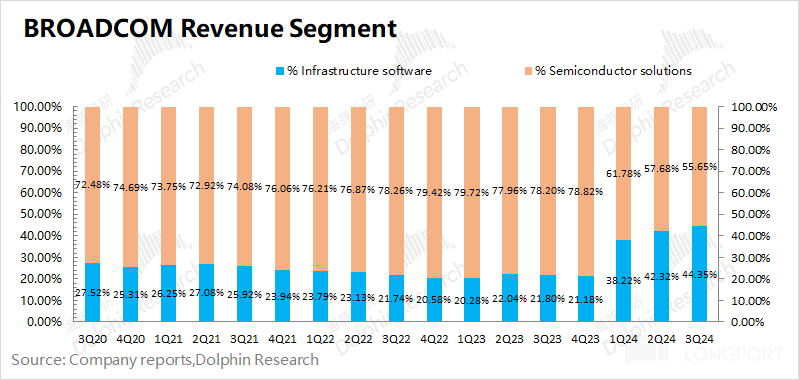

Currently, Broadcom's business is mainly divided into semiconductor solutions and infrastructure software. With the inclusion of VMware, the proportion of the company's software business has significantly increased, almost reaching a 1:1 ratio.

With the company's expansion through mergers, the capabilities of its various businesses mainly come from acquisitions. Looking specifically at the two main business categories:

1) Semiconductor Solutions: Hardware remains the company's largest source of revenue, accounting for over 50%;

① Network Business (30%): Main products include Ethernet switching chips, router chips, ASIC customized chips, etc., with business capabilities mainly acquired from Broadcom and LSI;

② Broadband Business (6%): Main products include set-top box SoCs, gateways, etc., with business capabilities mainly acquired from Broadcom; ③Wireless Business (13%): The main products include RF RF modules and filters, WiFi and Bluetooth SoC, and the business capabilities mainly come from the previous acquisitions and integrations of Infineon related businesses and Javelin Semiconductor;

④Storage/Server Business (7%): The main products include SAS and RAID controllers, PCIe switches, and the business capabilities mainly come from the acquisition and integration of LSI's business;

⑤Industrial and Others (2%): The main products include optocouplers, industrial-grade optical fibers, etc., and the business capabilities mainly come from Nemicon, CyOptics, etc.

2) Infrastructure Software (42%): Since 2017, the company has entered the software business. Through acquisitions of CA, Symantec, and VMware, the company's software business proportion continues to increase. The main products of the company's software business currently include host software, distributed software, network security solutions, etc.

II. Avago's Past Acquisitions and Integrations

Regarding Avago's past development, it can mainly be divided into three stages: independent operation of Avago, acquisition of LSI, and acquisition of Broadcom. These three stages have played important roles in Broadcom's future development.

Overall, Broadcom's acquisitions and integrations have distinct characteristics: ① Target companies have leading technological advantages or market shares; ② Acquisitions through leveraged funds; ③ Retain and develop core businesses; ④ Operational integration, reduce costs, improve profit margins; ⑤ Divest and monetize some assets to repay loans.

2.1 Establishment of Avago

Initially, Avago originated from Agilent (spun off from HP independently and listed). Since Agilent's main businesses at the time were T&M (providing testing and solutions for communication networks, etc.) and LS&CA (life science-related businesses), the semiconductor business accounted for a relatively small proportion and was greatly affected by industry cycles. The company was more inclined towards the development of the former, leading to the idea of disposing of the semiconductor business.

At that time, KKR and Silver Lake decided to acquire Agilent's semiconductor business for $2.66 billion and subsequently renamed it Avago.

From an operational and financial perspective:

1) Operational Perspective: Avago focused on high-margin and high-growth products such as filters, RF, etc., and sold off some other businesses. The company relocated its headquarters to Singapore to enjoy a tax rate of around 5%. In addition, the company outsourced some of its IT back-office operations to India.

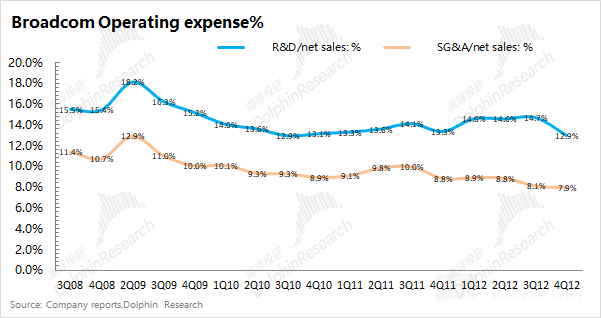

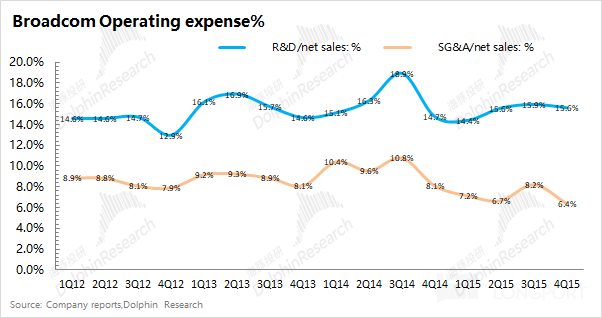

Through these series of operations, the company not only retained core business advantages and achieved growth, but also reduced the company's R&D expense ratio from around 16% to around 14%; the sales and management expense ratio also decreased from 11% to around 8% During this period, the company's annual revenue increased by $800 million, but the total of two expenses showed no significant growth.

2) Fundamentals: The total funds required for the entire transaction amount to $2.775 billion, including $2.66 billion for the target consideration and operational, transaction-related expenses. Half of the funds provided by KKR and Silver Lake Capital came from high-interest borrowings, totaling approximately $1.4 billion.

Subsequently, within Arvgo's six major businesses at the time, PMC-Sierra, Imaging Solutions, and other non-core businesses were directly divested and sold within a year, generating $700 million, which was used to directly repay half of the debt.

The remaining liabilities, Avago went public in 2009 with a valuation reaching $4 billion, nearly 50% higher compared to the acquisition four years ago. Through operational improvements, the stock price began to rise, allowing shareholders to repay debts and earn profits.

2.2 Acquisition of LSI

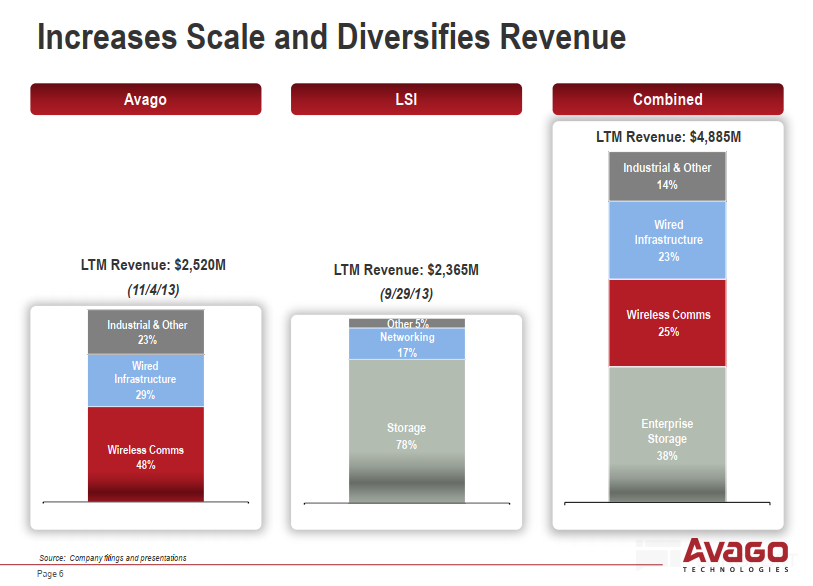

Since becoming independent, Avago gradually became a "small leader" in the semiconductor industry, especially in the RF filter and wireless business. Particularly in the filter market, the company's market share was significantly ahead. Riding the wave of 4G smartphones, the company's market value grew from $4 billion to over $10 billion. While the company's business steadily developed, Avago set its sights on LSI's HDD and SSD storage sector.

At that time, LSI was not a small company, with overall revenue scale similar to Avago. For example, in 2013, Avago's annual revenue was around $2.5 billion, while LSI's revenue exceeded $2 billion.

Although there were doubts in the market about the company's acquisition, Avago believed it could "help LSI reduce cost rates and enhance profitability". At that time, Avago's combined R&D and marketing expense ratio had already decreased to 21%, while LSI's was surprisingly high at 39%.

1) Operational Aspect: 78% of LSI's revenue came from the storage business, which did not overlap with Avago's existing business and had little synergy. The acquisition was mainly based on high-quality assets and financial integration. LSI's storage business was mainly divided into HDD and SSD. After completing the acquisition, Avago similarly retained the core HDD business and divested some of the remaining businesses. The company sold the SSD business and Axxia business, reducing operational losses while also enabling early repayment of some debts.

Furthermore, the company integrated LSI's R&D and sales aspects with the original Avago, significantly reducing the company's operating expenses After the acquisition, the combined R&D expense ratio and sales and management expense ratio once reached around 30%, but through the reduction and integration of expenses on the company's end, the two expense ratios returned to below 25%. By the end of 2015, the company's revenue and profit both soared, achieving a doubling growth.

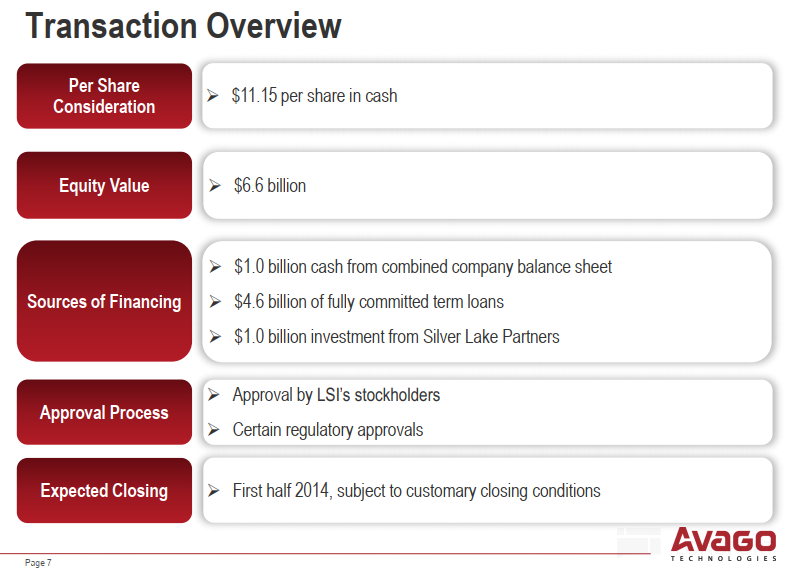

2) Fundamentals: Similar to before, the company's funds mainly come from borrowings. For the consideration of $6.6 billion for the acquisition of LSI, $4.6 billion came from bank borrowings, $1 billion from the merged company, and another $1 billion from Silver Lake Capital. Also, within a year of the acquisition, the company successively sold non-core SSD and Axxia businesses, bringing in $450 million and $650 million respectively, to repay some of the bank borrowings and reduce the company's interest expenses. Through a year of split and integration, Avago's stock price doubled again, exceeding $40 billion.

2.3 Acquisition of Broadcom

After completing the acquisition of LSI, Avago had already become one of the top ten semiconductor companies globally. However, not content with this, in less than two years, the company shifted its focus to Broadcom. At that time, Broadcom was already in the top 5 of global semiconductor companies, making Avago's acquisition undoubtedly a "big fish eats small fish" scenario.

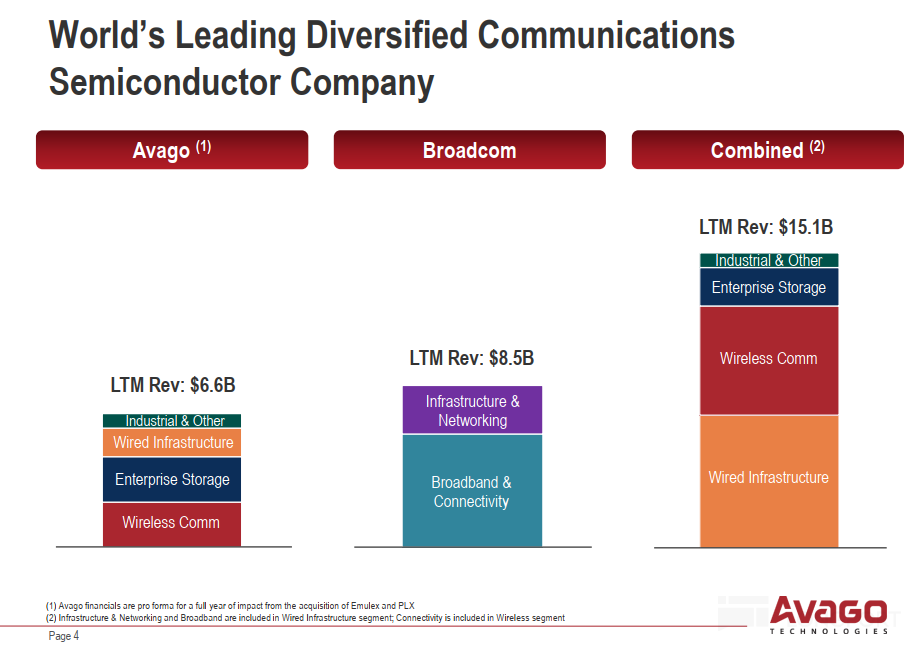

Similar to the situation with LSI, the relevance of Broadcom's business to Avago was also low at that time. The only related wireless business accounted for only 1/5 of Broadcom's revenue. Before the acquisition, Avago's annual revenue was about $6.6 billion, while Broadcom's annual revenue had already reached $8.5 billion. However, due to differences in operational efficiency, Avago's operating profit was higher than Broadcom's. In the first quarter of 2025, Avago's operating profit margin reached 38%, while Broadcom's was only 24%.

1) Operational Aspect: After acquiring Broadcom, the company further expanded its wired infrastructure and wireless communication businesses, which became the new company's core performance drivers. While retaining core businesses, the company divested "unprofitable" IoT businesses, reducing the company's interest costs.

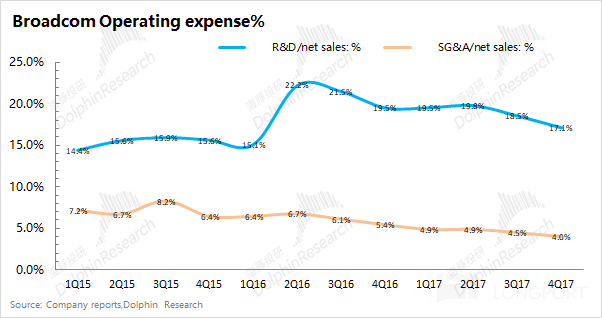

Furthermore, the company continued to integrate resources related to R&D and sales, reducing the expense ratio from nearly 30% at the time of acquisition to around 20% within 1-2 years, resulting in significant improvements in revenue and profit.

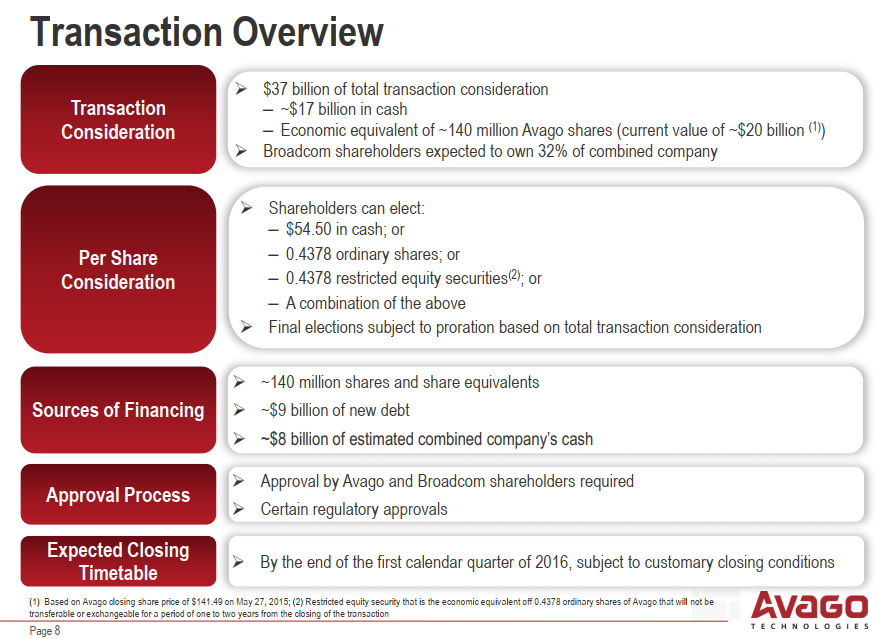

2) Fundamentals: With the increasing size of Avago's acquisitions, the consideration for the acquisition of Broadcom this time reached $37 billion. In terms of fund arrangement, the company conducted it in a "cash + stock" manner, including $17 billion in cash and $14 billion in stock consideration. Of the $17 billion in cash, it mainly consists of $9 billion in new debt and $8 billion in cash on hand.

The IoT business that the company subsequently divested fetched $550 million, which also helped repay some of the debt. With the company's business integration, in less than 2 years, the quarterly net profit of the company increased from $400 million to $600 million. The company's stock price also doubled again, reaching over $80 billion.

III. Current Acquisition of VMware and Broadcom's Goals

Following the completion of the acquisition of Broadcom, the company began to look for new directions. At this point, Broadcom had already firmly established itself in the top five of the global semiconductor industry, but the company wanted to make another major acquisition. In 2017, the company proposed to acquire Qualcomm, a company that was still larger than itself. However, this heavyweight acquisition was eventually called off by the U.S. government.

After the acquisition hit a roadblock, Broadcom rethought its strategy, stopped expanding in the semiconductor field, and turned to the software sector. Subsequently, the company acquired companies such as CA and Symantec, increasing the company's software business revenue to 20%.

In the past two years, the company has also acquired another publicly traded company in the software sector—VMware. The company acquired VMware for $61 billion and assumed $8 billion in debt. The large-scale acquisition brought revenue growth to the company but also once again brought pressure to the company.

3.1 Regarding the Acquisition of VMware this time

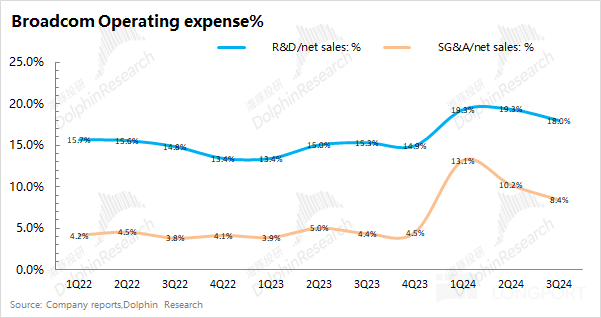

1) Operational Aspect: With the acquisition and consolidation, the company's related expense ratio has once again significantly increased. The combined R&D% and SG&A% of the company have increased from around 20% to 32%. Based on past shared processing, it is expected that these two expense ratios of the company will also see a decrease, and the total expense ratio is expected to drop to below 25%. With the integration underway, the company's profit margin is also expected to significantly improve.

2) Fundamentals: The $61 billion transaction this time was mainly in a "cash + stock" manner. Originally, VMware shareholders could choose to trade at a price of $142.5 per share or an equivalent amount of Broadcom stock. At the same time, Broadcom and a consortium of banks prepared $32 billion in new loans For acquisition situations, Broadcom measures the company's debt repayment ability through the multiple of total liabilities/LTM adjusted EBITDA. Based on the company's historical acquisition situations, the relevant ratio will significantly increase after each major acquisition. With divestitures, asset sales, and business integration, the company repays some loans, increases profits, and thereby enhances its repayment ability. When the ratio of total liabilities/LTM adjusted EBITDA drops to around 2 times, the company will start a new round of acquisitions and consolidation.

3.2 Broadcom's Vision and Goals

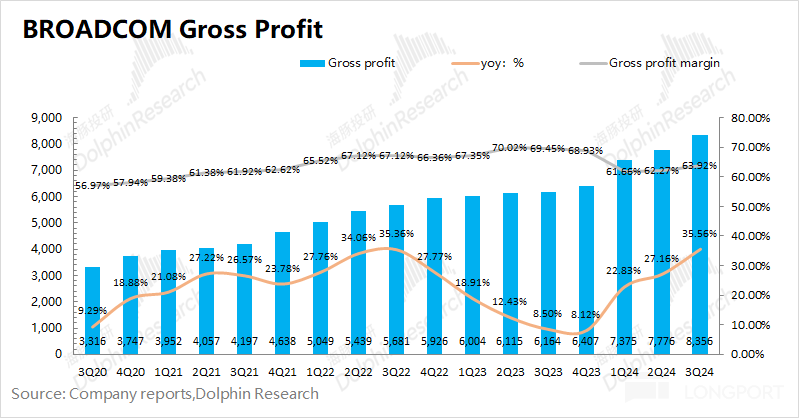

With the successive acquisitions of software companies such as CA, Symantec, and VMware in recent years, the company's gross profit margin has steadily increased. This is mainly due to the higher gross profit margin of the software business compared to the original semiconductor business, raising the company's gross profit margin from around 50% to over 60%.

Currently, due to the impact of VMware's acquisition and integration, the gross profit margin has temporarily declined. As VMware's own gross profit margin exceeds 80%, with the ongoing integration, Broadcom's overall gross profit margin is expected to return to above 70%. Combined with the reduction in operating expenses, the company's operating profit margin is expected to return to above 40%.

In addition to revenue, the company has set a target for EBITDA% on the operating side, which aligns with the company's strategy of "leveraged acquisition development." Adjusting the profit EBITDA for non-cash expenses is more like a rough measure of the company's cash profit, reflecting the company's operational efficiency and management capabilities while also measuring its debt repayment ability. The company has always set its EBITDA% target at above 60%, ensuring that after each acquisition, it remains a high-margin business while also having debt repayment capability.

With the consolidation of VMware, the ratio of total liabilities/LTM adjusted EBITDA has risen to 4.4. As operational improvements lead to an increase in adjusted EBITDA and a decrease in total liabilities, the relevant ratio gradually declines to 3.5. Historically, 3.5 is still relatively high for the company.

Therefore, Dolphin believes that the company will temporarily not proceed with the next acquisition and will focus on integrating VMware. When the relevant ratio drops to around 2 times again, the company may start looking for new acquisition opportunities

Dolphin Research on Semiconductor Articles Review:

September 6, 2024 Conference Call "Broadcom: ASIC demand will increase in 2025 (FY24Q3 Conference Call)"

September 6, 2024 Financial Report Review "Broadcom "soaring"? AI can't support the collapse of traditional semiconductors"

August 29, 2024 Conference Call "NVIDIA: Blackwell shipments start in the fourth quarter (FY25Q2 Conference Call)"

August 29, 2024 Financial Report Review "NVIDIA: AI faith collapses, honey turns into poison?"

August 2, 2024 Financial Report Review "Intel: Complete defeat, Intel's "dream" shattered"

July 31, 2024 Conference Call "AMD: MI350 to compete with Blackwell (24Q2 Conference Call Summary)"

July 31, 2024 Financial Report Review "AMD: Major factories hoarding, AI guidance on the rise again"

July 18, 2024 Conference Call "TSMC: Annual revenue growth of over 20% (24Q2 Conference Call Summary)"

July 18, 2024 Financial Report Review "ASML and Trump keep "bluffing"? TSMC "dominance" fears nothing!"

Risk Disclosure and Statement of this article: Dolphin Research Disclaimer and General Disclosure